Business Insurance

Business Owners Policy (BOP) For Electricians

★★★★★ 150+ Five-Star Reviews · Google & Facebook

A single spark from a faulty connection can burn through a client's kitchen, your reputation, and your bank account in the same afternoon. Electrical contractors face a unique combination of risks that most small business insurance policies weren't designed to handle: fire liability, expensive tool theft, project delays, and property damage that can escalate fast. That's why a Business Owners Policy, or BOP, built specifically for electricians bundles the coverage you actually need into one policy at a price that makes sense. The average cost for an electrical contractor's BOP in 2026 runs approximately $937 per year, though higher-risk operations can pay significantly more. This guide breaks down coverage limits, exclusions, real claims scenarios, and the endorsements that separate a policy that works from one that leaves you exposed. Whether you're a solo electrician running residential service calls or managing a crew on commercial buildouts, understanding how a BOP works for your trade is one of the smartest business decisions you'll make this year.

Understanding the Business Owners Policy (BOP) for Electrical Contractors

A BOP is a bundled insurance product that combines several essential coverages into a single policy. For electrical contractors, it's designed to protect against the most common financial threats: someone getting hurt on a job site, your tools getting stolen from a van, or a fire shutting down your operations for weeks. Instead of purchasing general liability, commercial property, and business interruption insurance as three separate policies, a BOP packages them together, usually at a lower premium than buying each individually.

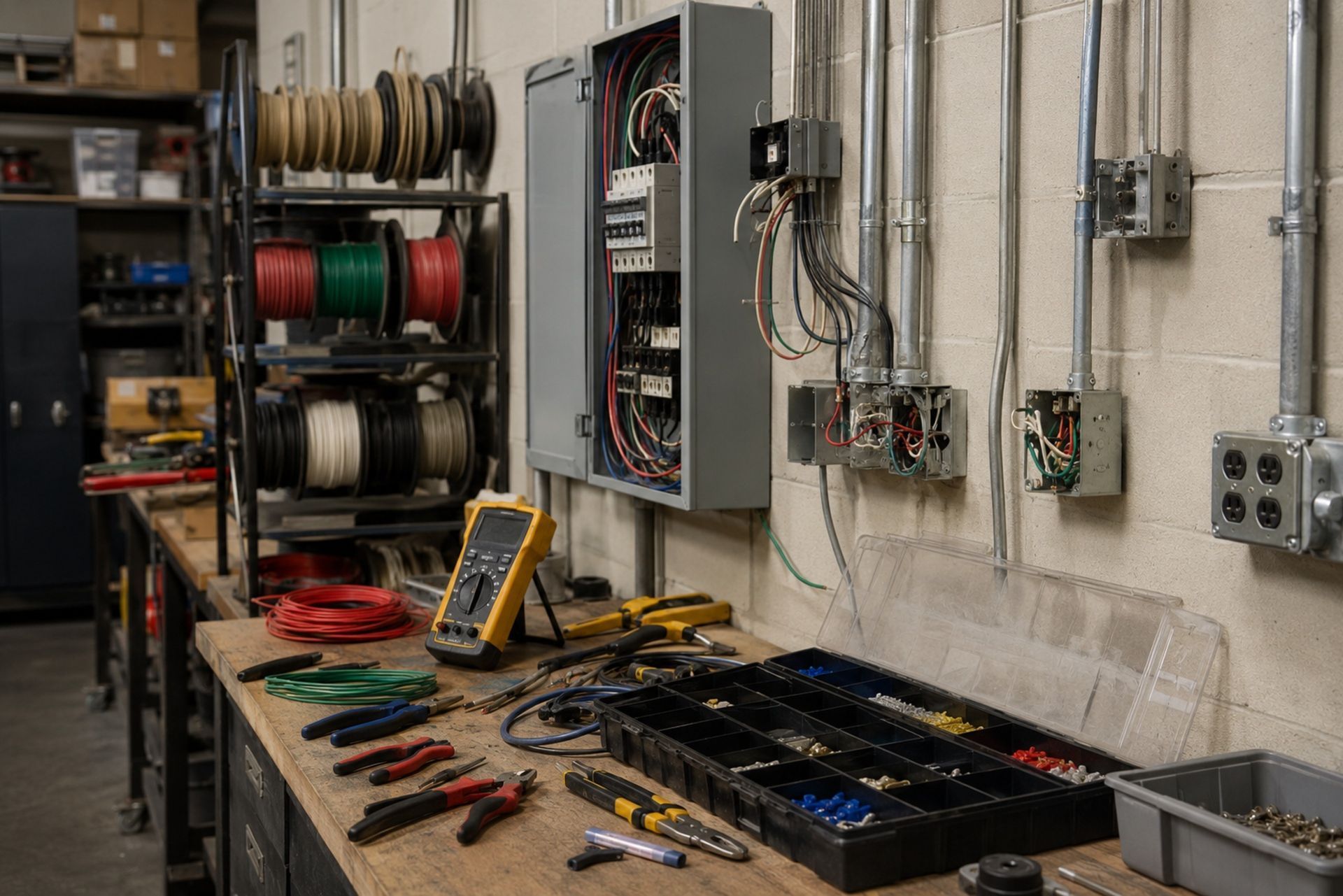

The electrical trade carries risks that generic business policies don't always account for. You're working with live circuits, running wire through walls, and installing panels in buildings worth millions. A BOP tailored to electricians reflects those realities in its coverage structure, limits, and available endorsements.

Why a BOP is Essential for the Electrical Trade

Most states require some form of liability insurance before you can pull permits or bid on contracts. But legal minimums rarely cover the full scope of what can go wrong. A client's house fire traced back to your wiring job, a tripped breaker that damages a server room, copper wire stolen from your warehouse: these are Tuesday problems in the electrical industry.

A BOP gives you a foundation. It won't cover everything (we'll get to exclusions), but it handles the bread-and-butter risks that would otherwise come straight out of your pocket. General contractors and property managers increasingly require proof of a BOP before they'll let you on site, so carrying one also keeps your pipeline full.

The Three Pillars: General Liability, Property, and Business Interruption

Think of a BOP as a three-legged stool. General liability covers third-party bodily injury and property damage claims. Commercial property protects your physical assets: tools, equipment, office furniture, inventory. Business interruption replaces lost income if a covered event forces you to stop working.

Each pillar addresses a different financial threat. Lose one, and the whole thing tips over. A fire at your shop might be covered under property insurance, but without business interruption coverage, you're still losing revenue every day you can't operate. That combination is what makes a BOP more valuable than any single policy on its own.

By: Michael Fusco

President of Joule Pro

INDEX

Understanding the Business Owners Policy (BOP) for Electrical Contractors

Core Coverage Components and Policy Limits

Common Exclusions Every Electrician Should Know

Real-World Claims Examples in the Electrical Industry

Customizing Your BOP with Industry-Specific Endorsements

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Core Coverage Components and Policy Limits

Understanding what each component actually covers, and where the limits sit, is the difference between filing a successful claim and getting a denial letter.

General Liability: Protecting Against Job Site Accidents

General liability is the workhorse of your BOP. It responds when a customer trips over your extension cord, when your work causes water damage to a neighbor's property, or when a completed installation leads to a claim months later. Most BOPs for electricians carry general liability limits between $300,000 and $1 million per occurrence, with aggregate limits of $1 million to $2 million.

Here's what catches people off guard: general liability covers completed operations. That means if you finish a panel upgrade in March and the client's house has an electrical fire in September, your policy can still respond. This is critical for electricians because defective workmanship claims often surface long after the job is done.

Commercial Property: Covering Tools, Inventory, and Office Space

Your commercial property coverage protects physical assets at your listed business location. This includes office equipment, computers, furniture, and any tools or inventory stored on-site. Standard BOP property limits for small electrical contractors typically range from $50,000 to $500,000, depending on the value of your assets.

One thing to keep in mind: property coverage under a BOP usually applies only at the location listed on your policy. Tools in your work van or materials stored at a job site may not be covered unless you add specific endorsements (more on that below). This is a common gap that electricians don't discover until after a loss.

Determining Appropriate Coverage Limits for Electrical Risks

Choosing limits isn't guesswork. Start by calculating the replacement cost of your tools, equipment, and office contents. Then consider your largest active contract: if a liability claim on that job exceeded your per-occurrence limit, could you cover the difference?

| Coverage Type | Typical Minimum | Recommended for Most Electricians | High-Risk Operations |

|---|---|---|---|

| General Liability (per occurrence) | $300,000 | $1,000,000 | $2,000,000 |

| General Liability (aggregate) | $600,000 | $2,000,000 | $4,000,000 |

| Commercial Property | $50,000 | $150,000–$300,000 | $500,000+ |

| Business Interruption | 30 days | 60–90 days | 12 months |

Many general contractors require $1 million per occurrence and $2 million aggregate as minimums before they'll add you to a project. Programs like Joule Pro, which focuses exclusively on licensed electrical contractors, can help you find the right limits without overpaying for coverage you don't need.

Common Exclusions Every Electrician Should Know

Every insurance policy has exclusions, and a BOP is no different. Knowing what's not covered is just as important as knowing what is.

Professional Errors and Omissions vs. General Liability

General liability covers physical damage and bodily injury. It does not cover claims arising from professional advice, design errors, or failure to meet a specification. If you design an electrical system that doesn't meet code and the client sues for the cost of redesign, that's a professional liability (errors and omissions) claim, not a general liability claim.

This distinction matters most for electricians who do design-build work or provide engineering consultation. A standard BOP won't include professional liability coverage. You'll need a separate E&O policy or an endorsement to fill that gap. Electrical contractors who bid on commercial or industrial projects should pay close attention here because design-related claims are among the most common disputes in the construction industry.

Standard Exclusions: Vehicles, Workers' Comp, and Flood Damage

Your BOP will not cover vehicles, employee injuries, or flood damage. These require separate policies:

- Commercial auto insurance covers your vans, trucks, and any vehicle used for business

- Workers' compensation covers employee injuries on the job and is required in nearly every state

- Flood insurance is a separate policy, typically through FEMA's National Flood Insurance Program or a private carrier

Other common BOP exclusions include pollution liability, cyber liability, and employment practices liability. If you store chemicals, handle client data, or have employees, these gaps deserve attention. A specialty program like Joule Pro can bundle these alongside your BOP so nothing falls through the cracks.

Real-World Claims Examples in the Electrical Industry

Abstract coverage descriptions only go so far. Here's how BOP claims actually play out for electricians.

Faulty Wiring Leading to Fire Damage

An electrician completes a residential panel upgrade. Six months later, a loose connection in the panel causes an arc fault, igniting insulation inside the wall. The homeowner's insurance pays for the home repairs and then subrogate against the electrician's policy. The completed operations portion of the electrician's general liability responds, covering the homeowner's damages up to the policy limit.

Electrical fires account for a significant share of residential fire damage each year, and home electrical fires cause an estimated $1.5 billion in property damage annually. This is the single most common high-dollar claim type for electrical contractors, which is why adequate per-occurrence limits matter so much.

Theft of Specialized Electrical Equipment and Copper

A contractor arrives at the shop Monday morning to find the lock cut and $40,000 worth of copper wire, conduit benders, and diagnostic equipment gone. The commercial property portion of the BOP covers the stolen inventory and tools, minus the deductible, up to the property coverage limit.

Copper theft remains a persistent problem in the electrical trade. If your property limits are set too low, you'll eat the difference. Review your tool and material inventory annually and adjust your limits accordingly.

Customizing Your BOP with Industry-Specific Endorsements

A base BOP is a starting point. The endorsements you add are what make it work for the way you actually run your business.

Inland Marine: Protecting Tools in Transit

Standard commercial property coverage protects assets at your listed location. Inland marine coverage extends that protection to tools and equipment while they're in your van, at a job site, or in transit between locations. For electricians who carry $10,000 to $50,000 worth of tools in their vehicles every day, this endorsement is essential.

Inland marine policies typically cover theft, accidental damage, and loss. The premiums are relatively low compared to the replacement cost of a fully stocked service van. If you've ever had a $3,000 Fluke meter walk off a job site, you understand the value here.

Installation Floaters for High-Value Project Materials

An installation floater covers materials and equipment you've purchased for a specific project but haven't yet installed. Think about a commercial job where you've ordered $80,000 in switchgear that's sitting in a staging area. If it's damaged by water, stolen, or destroyed in a fire before installation, your base BOP property coverage probably won't respond because the materials aren't at your listed business location.

Installation floaters fill that gap. They cover project materials from the time you take possession until the work is complete and accepted by the client. For electricians working on larger commercial or industrial projects, this endorsement can prevent catastrophic out-of-pocket losses.

How to Evaluate and Purchase the Right Policy

Shopping for a BOP isn't like comparing car insurance quotes online. The cheapest policy almost never provides the best protection for electrical contractors, and the differences between policies often hide in endorsement availability and exclusion language.

Start by listing your actual exposures: the value of your tools, your largest active contract, the number of employees, and the types of work you perform. Then look for an insurer or program that specializes in contractor risks. Generalist agencies often lack the underwriter relationships needed to place electrical contractors at competitive rates, especially if you do high-voltage or industrial work.

Ask about claims handling. A policy is only as good as its response when something goes wrong. Find out whether you'll work with a dedicated claims team or get routed through a generic call center. Joule Pro, backed by Fusco Orsini & Associates Insurance Services, provides direct access to licensed professionals who understand electrical trade risks, which means faster quotes, cleaner proposals, and fewer surprises at renewal.

Frequently Asked Questions

Does a BOP cover my work van? No. Vehicles require a separate commercial auto policy. Your BOP's property coverage applies to assets at your business location, not vehicles.

Is workers' comp included in a BOP? It's not. Workers' compensation is a standalone policy required in nearly every state if you have employees. You'll need to purchase it separately.

Can I get a BOP if I'm a sole proprietor? Yes. BOPs are available to sole proprietors, and they're often the most cost-effective way to bundle liability and property coverage for one-person electrical operations.

How much does a BOP cost for an electrician? The average runs around $937 per year in 2026, but your premium depends on revenue, number of employees, claims history, and the type of electrical work you perform.

Does a BOP cover work I completed months ago? Yes, through the completed operations portion of your general liability coverage. This is critical for electricians because defective workmanship claims often appear well after a job wraps up.

Making the Right Choice for Your Electrical Business

A BOP gives electrical contractors a solid insurance foundation, but the details matter more than the label on the policy. Get your coverage limits right, understand the exclusions, and add endorsements that match how you actually work. Review your policy annually as your business grows, your tool inventory changes, and you take on different types of projects.

If you're unsure where to start or whether your current policy has gaps, reach out to a program built for your trade. The right coverage protects more than your balance sheet: it protects the business you've spent years building.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.