Business Insurance

Tools and Equipment Insurance For Electricians in Washington

★★★★★ 150+ Five-Star Reviews · Google & Facebook

A stolen work van with $15,000 worth of Fluke meters, Megger insulation testers, and conduit benders inside. A jobsite fire that melts your wire-pulling equipment overnight. A crew member who accidentally drops a thermal imaging camera off a ladder on a high-rise in Seattle. These are the scenarios that separate electricians who bounce back quickly from those who eat the loss out of pocket. If you're a licensed electrical contractor in Washington State, understanding how tools and equipment insurance works - including coverage limits, state-specific requirements, and which carriers actually want to write your policy - isn't optional knowledge. It's the difference between a minor inconvenience and a five-figure hit to your bottom line. Most electricians carry general liability and workers comp because they have to. But the coverage that protects the physical tools you use every single day? That's where the gaps show up. And in a state like Washington, where licensing, bonding, and permitting requirements create a web of compliance obligations, getting this piece wrong can stall your business faster than a rainy January in Olympia.

Understanding Inland Marine Insurance for Washington Electricians

Inland marine insurance is the policy type that covers tools, equipment, and materials while they're in transit or stored at jobsites - basically anywhere that isn't a fixed location like your shop. The name sounds odd (what does "marine" have to do with electrical work?), but it traces back to ocean cargo policies and has evolved to cover movable property of all kinds.

For Washington electricians, this is the policy that matters most for protecting your physical assets. Your tools travel with you constantly: from the warehouse to a residential panel upgrade in Bellevue, then to a commercial tenant improvement in Tacoma. Inland marine follows those tools wherever they go, which is exactly what you need.

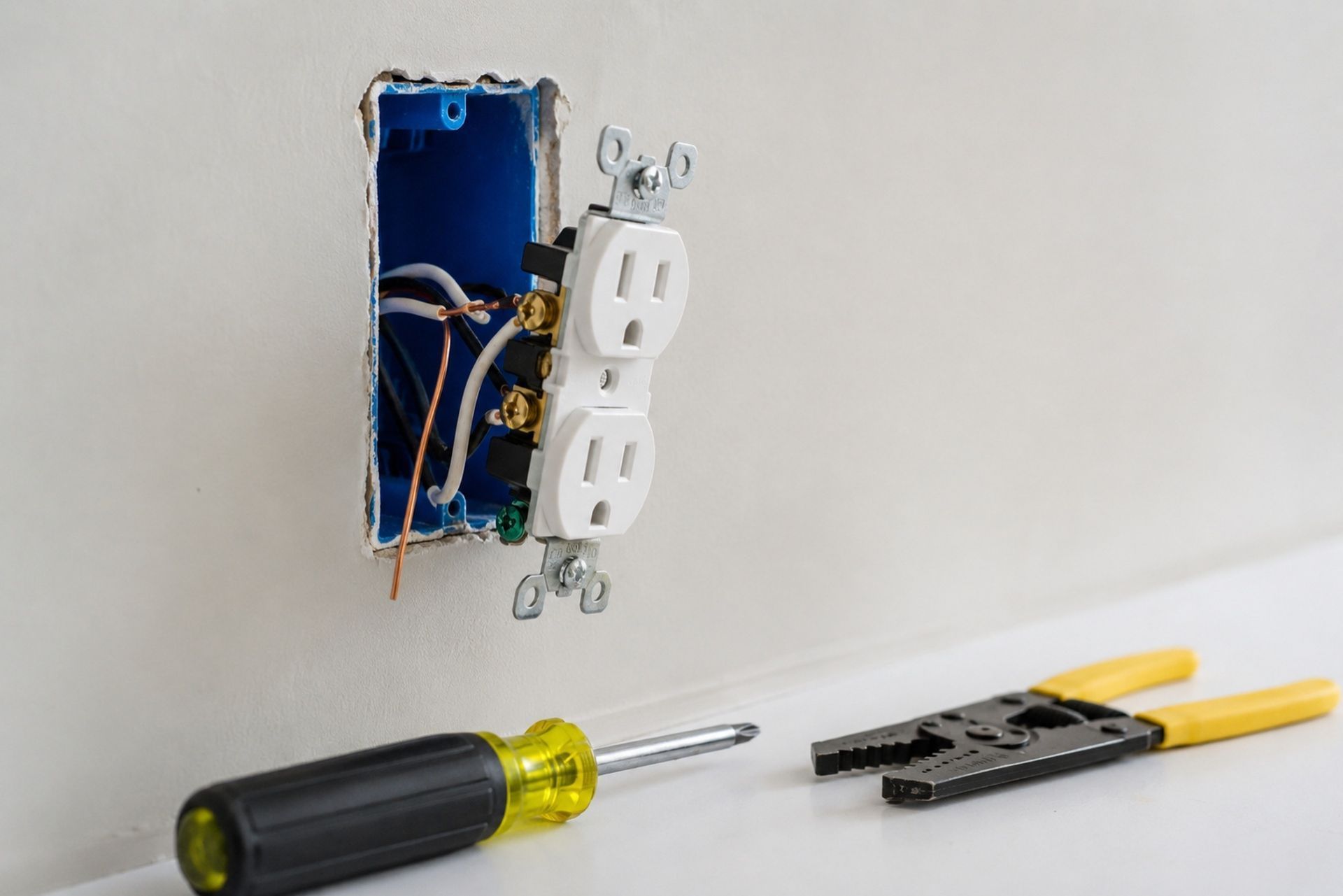

Why Standard General Liability Isn't Enough for Tools

General liability covers bodily injury and property damage you cause to others. It does not cover your own tools and equipment. This is one of the most common misunderstandings we see at Joule Pro when onboarding new electrical contractors.

Your commercial property policy might cover tools stored at your shop, but the moment those tools leave the premises, coverage typically ends. Think about how much time your equipment actually spends at your permanent location versus out on jobs. For most electricians, the answer is obvious: the tools are almost always on the road or on a site.

A general liability claim pays when your apprentice accidentally damages a homeowner's hardwood floor. An inland marine claim pays when someone breaks into your van overnight and takes your oscilloscope, your power tools, and your fish tape reels. Two completely different risks, two completely different policies.

Coverage for Specialty Electrical Testing Equipment

Residential electricians might get by with $10,000 to $25,000 in tool coverage. But if you're doing industrial or commercial work, your testing equipment alone can exceed that range. A single Fluke 1587 FC insulation multimeter runs over $700. A quality power quality analyzer can cost $5,000 or more. Megger testing equipment for medium-voltage work? You're looking at $10,000 to $20,000 per unit.

The point is that electrical testing equipment has gotten expensive, and standard blanket limits on a cheap inland marine policy may not cut it. You need to know exactly what you own and what it would cost to replace, then build your coverage around those numbers.

By: Michael Fusco

President of Joule Pro

INDEX

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Washington State Requirements and Licensing Mandates

Washington has some of the more structured electrical licensing requirements in the country. The state's Department of Labor & Industries (L&I) oversees electrical contractor licensing, and the rules are specific.

L&I Compliance for Electrical Contractors

Washington electrical contractors must maintain a $4,000 surety bond or assignment of savings under RCW 19.28. This bond protects consumers but does nothing for your tools or equipment. It's a common point of confusion: contractors assume the bond provides broad protection, but it's narrowly focused.

L&I requires proof of workers compensation coverage for any contractor with employees. Washington is a monopolistic state for workers comp, meaning you purchase it directly through L&I rather than through private carriers. This is unusual compared to most states and catches out-of-state contractors off guard.

While Washington doesn't mandate inland marine or tools coverage by statute, many general contractors and project owners require it contractually before you set foot on their jobsite. The practical requirement is real even if the legal mandate isn't.

Proof of Insurance for Local Municipal Permits

Cities like Seattle, Tacoma, Spokane, and Vancouver each have their own permitting offices, and most require proof of general liability insurance before issuing electrical permits. Some municipalities have minimum coverage thresholds of $1 million per occurrence.

If you're pulling permits across multiple jurisdictions (common for electricians working the I-5 corridor), keeping your certificates of insurance current and accessible saves real time. A program like Joule Pro, which handles the full contractor coverage stack, can issue updated certificates quickly because all your policies are managed in one place by a licensed producer who understands electrical trade requirements.

Determining Appropriate Coverage Limits and Deductibles

Getting the right coverage limit is more art than science. Too low, and you're underinsured when it matters. Too high, and you're paying for coverage you don't need.

Replacement Cost vs. Actual Cash Value

This distinction matters more than most electricians realize. Here's the quick comparison:

| Feature | Replacement Cost | Actual Cash Value (ACV) |

|---|---|---|

| Payout basis | Cost to buy new equivalent | Depreciated value |

| Premium | Higher | Lower |

| Best for | Newer, expensive equipment | Older tools nearing end of life |

| Claim example | $3,000 meter replaced at $3,000 | $3,000 meter paid out at $1,200 after depreciation |

If you bought a $4,500 Megger tester three years ago and it gets stolen, an ACV policy might pay you $2,000 after depreciation. A replacement cost policy pays what it actually costs to buy a new one in 2026. For most working electricians, replacement cost is worth the premium difference.

Scheduling High-Value Items vs. Blanket Limits

Blanket coverage sets one total limit for all your tools and equipment combined. Scheduling means listing specific high-value items individually on the policy with their own stated values.

The general rule: schedule anything worth more than $2,500 individually. This protects you from sublimit surprises and ensures the adjuster knows exactly what was covered. Keep your blanket limit for hand tools, drill bits, PPE, and other items that would be tedious to list one by one.

A common mistake is setting a blanket limit based on what you owned when you bought the policy, then adding $8,000 worth of new equipment over two years without updating coverage. Review your limits annually at minimum.

Carrier Appetite and Underwriting in the Pacific Northwest

Not every insurance carrier wants to write tools and equipment coverage for electricians. Carrier appetite - the willingness of an insurer to take on a specific type of risk - varies significantly based on your specialty, claims history, and location.

Preferred Carriers for Residential vs. Industrial Electricians

Residential electricians generally find broader carrier appetite. The risk profile is straightforward: smaller tool inventories, lower-voltage work, and fewer catastrophic exposure scenarios. Most standard commercial carriers will write inland marine for residential electrical contractors without much friction.

Industrial and commercial electricians face a tighter market. If you're working in refineries, data centers, or doing medium-voltage installations, fewer carriers are interested. The tool values are higher, the jobsite risks are greater, and theft exposure on large commercial sites can be significant. This is where working with a specialty program like Joule Pro pays off: we maintain underwriter relationships specifically built around electrical trade risks, which means access to markets that generalist agencies may not even know exist.

Common Exclusions and Theft Prevention Requirements

Most inland marine policies exclude wear and tear, mechanical breakdown, and tools left in an unlocked vehicle. That last one trips up electricians constantly. If your van doesn't have proper locks or a secure tool vault and you file a theft claim, expect pushback from the adjuster.

Other common exclusions include damage from flooding (separate flood coverage is needed), tools lent to subcontractors, and equipment rented to others. Some carriers also require specific anti-theft measures: GPS tracking on vehicles, locked tool cribs on jobsites, or inventory documentation. Meeting these requirements upfront can mean the difference between a paid claim and a denied one.

Strategies for Reducing Premiums and Managing Claims

Premium costs for inland marine coverage typically run between 1% and 3% of the total insured value annually. A $50,000 tool inventory might cost $500 to $1,500 per year to insure. That's reasonable, but there are ways to bring it down further.

The Role of Tool Inventories and Digital Tracking

Carriers love documentation. A detailed tool inventory with serial numbers, purchase dates, photos, and receipts does two things: it gets you better rates at underwriting, and it makes claims processing dramatically faster.

Several electricians we work with use simple spreadsheet systems or apps like Sortly or Tool Hawk to track their inventory. GPS tracking devices on high-value items (thermal cameras, power analyzers) and on vehicles carrying tools can qualify you for premium discounts of 5% to 15% with certain carriers.

The five minutes it takes to photograph a new tool and log its serial number can save you hours of headache during a claim. Build this habit into your purchasing process.

Bundling Inland Marine with Commercial Auto and Workers Comp

Bundling your inland marine policy with your commercial auto and general liability coverage through a single program often produces savings of 10% to 20% compared to buying each policy separately from different carriers. The insurer rewards the combined premium volume, and your administration gets simpler.

Since Washington requires workers comp through L&I, that piece stays separate. But your GL, commercial auto, and inland marine can all sit under one program. Joule Pro structures packages exactly this way for electrical contractors, which simplifies renewals and ensures your coverage limits coordinate properly across policies.

Before You Renew Your Policy

Washington electricians carry some of the most expensive portable equipment in the trades. Protecting that investment with the right inland marine policy isn't complicated, but it does require attention to the details: replacement cost versus ACV, scheduled items versus blanket limits, carrier exclusions around theft, and making sure your coverage keeps pace as you add equipment.

The contractors who handle this well share a few habits: they maintain current tool inventories, they review coverage limits every year, they bundle policies for savings, and they work with producers who actually understand electrical trade risks. If you're unsure whether your current coverage has gaps, reach out to a Joule Pro licensed producer for a policy review. A 20-minute conversation now beats a denied claim later.

Frequently Asked Questions

Does Washington State require electricians to carry tools and equipment insurance? No state statute mandates inland marine coverage, but many general contractors and municipalities require it before you can work on their projects. It's effectively required for most commercial work.

How much tools coverage do most Washington electricians carry? Residential contractors typically carry $10,000 to $30,000. Commercial and industrial electricians often need $50,000 to $150,000 or more, depending on their testing equipment inventory.

Will my commercial auto policy cover tools stolen from my van? Usually only up to a small sublimit, often $1,000 to $2,500. A standalone inland marine policy provides much broader protection for tools in vehicles.

What happens if I don't update my coverage after buying new equipment? You risk being underinsured. If your policy covers $25,000 but your actual inventory is worth $40,000, you'll absorb the difference out of pocket after a total loss.

Can I get inland marine coverage if I've had a prior theft claim? Yes, though your options may narrow and premiums may increase. Carriers want to see what theft prevention steps you've taken since the incident.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.