Business Insurance

Generator Installer Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

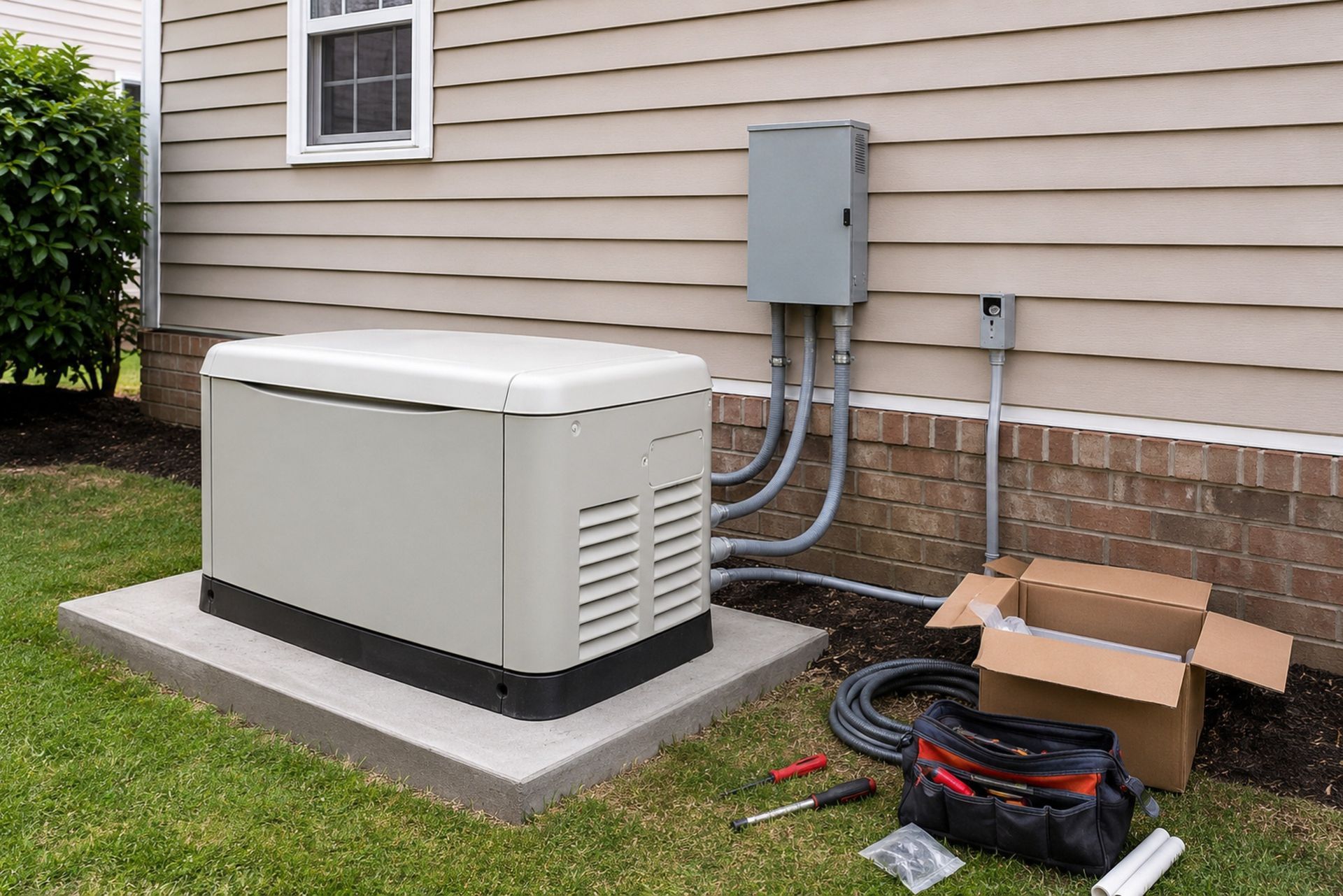

A single generator installation gone wrong can wipe out a small contracting business. Picture this: a 22kW standby unit tips off a forklift during placement, crushes a homeowner's gas meter, and triggers a leak that evacuates the block. The installer's out-of-pocket exposure for property damage, bodily injury claims, and regulatory fines could easily reach six figures before an attorney even gets involved.

Generator installation sits at the intersection of electrical work, fuel systems, concrete pads, and heavy lifting, which means the risk profile is broader than most electrical specialties. A complete insurance program for generator installers needs to cover general liability, workers comp, tools and equipment, commercial auto, and the trade-specific hazards that generic policies routinely exclude. Getting this wrong doesn't just cost money: it can cost your contractor's license.

This guide breaks down every coverage layer a generator installation business actually needs, with real numbers, common claim scenarios, and the policy details that matter most.

Core Liability Protection for Generator Installation Businesses

General liability and completed operations coverage form the foundation of any generator installer's insurance program. Without these two pieces in place, you're exposed to the most common and most expensive claims in the trade.

General Liability for Third-Party Property Damage and Bodily Injury

General liability (GL) covers damage you cause to other people's property and injuries to non-employees while you're on a job site. For generator installers, that includes scenarios like cracking a customer's driveway during equipment placement, damaging siding while running conduit, or a passerby tripping over your staging area.

Most installation businesses pay an average of $73 to $95 per month for general liability insurance, typically with a $1 million per occurrence limit and a $2 million aggregate. That range shifts depending on your annual revenue, number of employees, and claims history. A solo installer doing $200K in residential work will pay less than a five-person crew handling commercial standby systems.

One thing to keep in mind: GL policies for electrical contractors often include exclusions for pollution-related events, which matters a lot when you're connecting natural gas or diesel fuel lines. Make sure your policy doesn't carve out the exact risks your work creates.

Completed Operations Coverage for Post-Installation Faults

Your GL policy covers you while you're on site. Completed operations coverage picks up where that stops: it protects you after you've finished the job and left. This is where generator installers face some of their biggest exposure.

A transfer switch wired incorrectly might not fail for months, until the next power outage when it back-feeds into the utility grid and damages a neighbor's electronics. Or a vibration-dampening mount loosens over time and the unit shifts, cracking a gas line. These claims can surface a year or more after installation.

Completed operations is typically included within your GL policy, but the limits are shared. If you're doing 50+ installs a year, talk to your producer about whether your aggregate is high enough to absorb a late-surfacing claim on top of your normal exposure. Programs like Joule Pro, which are built specifically for licensed electrical contractors, structure these limits with the realities of electrical trade work in mind.

By: Michael Fusco

President of Joule Pro

INDEX

Core Liability Protection for Generator Installation Businesses

Protecting Your Workforce and Physical Assets

Commercial Auto and Fleet Insurance Requirements

Mitigating Trade-Specific Risks and Environmental Hazards

Surety Bonds and Regulatory Compliance

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Protecting Your Workforce and Physical Assets

People and tools are your two most valuable assets. Protecting both requires separate, purpose-built policies.

Workers Compensation for Electrical and Lifting Injuries

Generator installation is physically demanding and electrically hazardous. Your crew is lifting 250-pound units, trenching for conduit, working near live panels, and sometimes operating in confined spaces. Workers comp covers medical bills, lost wages, and rehabilitation when an employee gets hurt on the job.

Every state except Texas requires workers comp for businesses with employees, and many states mandate it as soon as you hire your first W-2 worker. Classification codes matter here: generator installers typically fall under NCCI code 5190 (electrical wiring), but if your crew also does concrete pad work or plumbing connections, you may need additional class codes. Misclassification can lead to audits, back-premiums, and penalties.

Common claims in this trade include back injuries from lifting generators, electrical burns from panel work, and hand injuries from conduit bending. Your experience modification rate (EMR) directly affects your premium, so investing in safety training pays off in real dollars.

Inland Marine Insurance for Specialized Tools and Testing Equipment

Standard commercial property policies cover your office and warehouse. They don't cover the $15,000 worth of tools, meters, load banks, and testing equipment sitting in your service van right now. That's where inland marine insurance comes in.

Inland marine covers tools and equipment in transit and at job sites, essentially anywhere away from your fixed business location. For generator installers, this includes wire pullers, torque wrenches, multimeters, megohm testers, transfer switch analyzers, and the generator units themselves before they're installed.

A typical inland marine policy for an electrical contractor runs between $500 and $2,000 annually, depending on the total value of covered equipment. Make sure your policy covers theft from locked vehicles, since tool theft from work trucks remains one of the most common property crimes affecting contractors. Some policies require specific security measures like locked toolboxes or GPS tracking to honor theft claims.

Commercial Auto and Fleet Insurance Requirements

If your business owns vehicles or your employees drive for work, you need commercial auto coverage. Personal auto policies exclude business use, period.

Coverage for Heavy-Duty Transport Trucks and Trailers

Generator installers don't drive sedans to job sites. You're running F-350s, box trucks, and flatbed trailers loaded with 500-pound generators. Commercial auto insurance covers these vehicles for liability, collision, and comprehensive losses.

Here's what most contractors miss: the trailer and its cargo need separate coverage. Your commercial auto policy covers the truck pulling the trailer, but the trailer itself and the generator strapped to it may need an inland marine endorsement or a separate cargo policy. If a trailer detaches on the highway and a $12,000 Generac ends up in a ditch, you want to know exactly which policy responds.

| Coverage Type | What It Covers | Typical Limit |

|---|---|---|

| Liability | Damage/injury you cause to others | $1M combined single limit |

| Collision | Damage to your vehicle from an accident | Actual cash value |

| Comprehensive | Theft, vandalism, weather damage | Actual cash value |

| Cargo/Inland Marine | Equipment and generators in transit | $25K-$100K per occurrence |

| Uninsured Motorist | Accidents caused by uninsured drivers | Varies by state |

Hired and Non-Owned Auto Liability

Sometimes your technician drives their personal truck to a job site, or you rent a flatbed for a large commercial install. Hired and non-owned auto (HNOA) coverage fills the gap when employees use personal vehicles for work or when you rent vehicles your business doesn't own.

Without HNOA, your business has zero liability protection if an employee causes an accident in their own car while driving between job sites. This endorsement is inexpensive, usually $200 to $500 per year, and it's one of the most overlooked coverages in the trades. Any contractor sending employees to job sites in personal vehicles needs this.

Mitigating Trade-Specific Risks and Environmental Hazards

Generator installation creates risks that most general contractor policies weren't designed to cover. Fuel systems and engineering liability require specialized endorsements.

Pollution Liability for Fuel Leaks and Hazardous Materials

Every generator runs on fuel: natural gas, propane, or diesel. During installation, your crew connects fuel lines, fills day tanks, and tests fuel delivery systems. A cracked fitting, an over-tightened connection, or a bumped fuel tank can release hazardous materials on a customer's property.

Standard GL policies almost universally exclude pollution events. A contractor's pollution liability (CPL) policy fills this gap, covering cleanup costs, third-party bodily injury from fumes or contamination, and regulatory defense costs. For generator installers working with diesel day tanks or underground propane lines, CPL isn't optional: it's essential.

Premiums for CPL policies typically range from $1,500 to $5,000 annually for small to mid-size contractors, depending on the volume of fuel-related work and your claims history.

Professional Liability for System Design and Load Calculations

If your business performs load calculations, specifies generator sizing, or designs transfer switch configurations, you're providing professional services. Professional liability (also called errors and omissions) covers claims arising from mistakes in those recommendations.

Here's a real scenario: you size a generator at 22kW for a home, but the customer's HVAC system, well pump, and electric range actually require 30kW. During an outage, the generator overloads and shuts down, leaving the customer without power and potentially damaging connected equipment. That's a professional liability claim, not a general liability claim, and your GL policy won't cover it.

Surety Bonds and Regulatory Compliance

Most states require electrical contractors to carry surety bonds before issuing or renewing a license. These bonds aren't insurance: they're a financial guarantee to the state and your customers that you'll perform work according to code and contract terms.

Bond amounts vary significantly by state. California requires a $25,000 contractor's license bond, while Florida's requirements differ based on the type of electrical license held. Some municipalities require additional permit bonds for specific projects. Failing to maintain your bond means losing your license, which means losing your ability to pull permits and work legally.

Beyond bonds, many states and municipalities require proof of specific insurance coverages before issuing contractor licenses. General liability and workers comp are nearly universal requirements. Some jurisdictions also mandate pollution liability for contractors working with fuel systems. Joule Pro's team stays current on state-specific requirements for electrical contractors, which saves you from discovering a compliance gap when you're trying to close a permit.

Factors Influencing Generator Installer Insurance Premiums

Your premiums aren't arbitrary. Insurers price generator installer coverage based on several measurable factors:

- Annual revenue and payroll: higher numbers mean higher premiums

- Number of employees and their experience levels

- Claims history over the past 3-5 years

- Types of generators installed (residential vs. commercial vs. industrial)

- Whether you work with diesel, natural gas, or propane systems

- Geographic location and state regulatory requirements

- Your EMR (experience modification rate) for workers comp

- Subcontractor usage and certificate tracking practices

Contractors who maintain clean claims histories, invest in safety programs, and carry proper certifications typically see premiums 15-30% lower than their peers. Bundling multiple coverages through a single program designed for electrical contractors, rather than piecing together policies from different carriers, often produces better pricing and fewer coverage gaps.

FAQ

How much does insurance cost for a generator installation business? Most small generator installation businesses spend between $3,000 and $10,000 annually for a full coverage package including GL, workers comp, commercial auto, and inland marine. Your exact cost depends on revenue, payroll, claims history, and the types of systems you install.

Do I need pollution liability insurance for generator installation? Yes, if you connect fuel lines or handle diesel, propane, or natural gas during installations. Standard GL policies exclude pollution events, so a separate contractor's pollution liability policy is necessary to cover fuel spills and related cleanup costs.

What's the difference between general liability and professional liability for generator installers? General liability covers physical damage and injuries. Professional liability covers mistakes in your professional recommendations, like incorrect load calculations or improper generator sizing. You likely need both if you specify equipment or design systems.

Does my personal auto insurance cover my work truck? No. Personal auto policies exclude vehicles used for business purposes. You need a commercial auto policy for any vehicle used in your generator installation business.

Can I get all my coverages from one provider? Yes. Specialty programs like Joule Pro bundle GL, workers comp, commercial auto, inland marine, and trade-specific endorsements into a single program designed for electrical contractors, which simplifies management and often reduces total cost.

Making the Right Coverage Choice

Getting insurance right for a generator installation business isn't about buying the cheapest policy: it's about eliminating the gaps that turn a routine claim into a business-ending event. Every coverage layer discussed here addresses a specific, documented risk that generator installers face regularly.

Start by auditing your current policies against the coverages outlined above. If you find gaps, especially around pollution liability, completed operations limits, or inland marine for tools in transit, address them before your next install. A single uncovered claim can cost more than a decade of premiums.

For a coverage review built around the actual risks of electrical trade work, reach out to the Joule Pro team. Every quote is handled by a licensed insurance professional who understands generator installation, not a chatbot or a generic call center.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.