Business Insurance

Stage and Theater Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

A stage electrician who accidentally trips a breaker during a sold-out Broadway preview doesn't just kill the lights: they can kill a production's entire insurance standing. Theater and stage electricians face a risk profile that most general insurance agents barely understand, from high-voltage temporary power setups to rigging motorized lighting trusses 60 feet above a stage. Getting the right coverage means understanding specialty risks, knowing which carriers actually want your business, and building a policy with trade-specific components that won't leave you exposed when a claim hits. This guide breaks down what stage and theater electrician insurance actually looks like in practice, covering the specific endorsements, exclusions, and underwriting factors that matter most for this niche within the electrical trades. If you've been lumped in with residential wiremen or commercial electricians by a generalist agent, you're probably either overpaying or underinsured. Likely both. General liability premiums for electricians are forecasted to rise between 4.2% and 9% in the current market cycle, and stage electricians often sit at the higher end of that range due to the unique hazards involved. The difference between a well-structured policy and a generic one can mean tens of thousands of dollars in a single claim.

Core Insurance Requirements for Stage and Theater Electricians

Stage electricians need the same foundational coverages as other electrical contractors, but the details inside those policies look very different. The venues, the equipment, and the work environment all create exposures that standard electrical contractor policies weren't designed to handle.

General Liability and Third-Party Property Damage

Your general liability policy is the backbone. For stage electricians, the critical piece is third-party property damage coverage that accounts for working inside venues you don't own. A single electrical fault that damages a theater's vintage lighting grid or triggers a fire suppression system can generate six-figure claims fast.

Most GL policies for electricians carry $1 million per occurrence and $2 million aggregate limits, but venues and production companies frequently require higher limits. You'll often need to carry a $5 million umbrella just to get on the approved vendor list for major theaters and touring productions. Pay close attention to your policy's completed operations coverage, which protects you after you've finished a job and left the venue. A wiring connection that fails three weeks after you installed it is still your problem.

Professional Liability for Lighting Design and Consulting

Here's where stage electricians diverge sharply from typical electrical contractors. Many theater electricians don't just install: they design lighting plots, consult on electrical load calculations, and spec equipment for productions. That's professional services work, and your GL policy won't cover errors in design or consulting advice.

Professional liability (errors and omissions) insurance covers claims arising from your professional recommendations. If you design a lighting layout that overloads a venue's electrical system, or if your load calculations are wrong and a dimmer rack fails during a performance, this is the policy that responds. Premiums typically run $1,200 to $3,500 annually for stage electricians, depending on your revenue and the scope of your consulting work.

Workers' Compensation for High-Altitude Technical Work

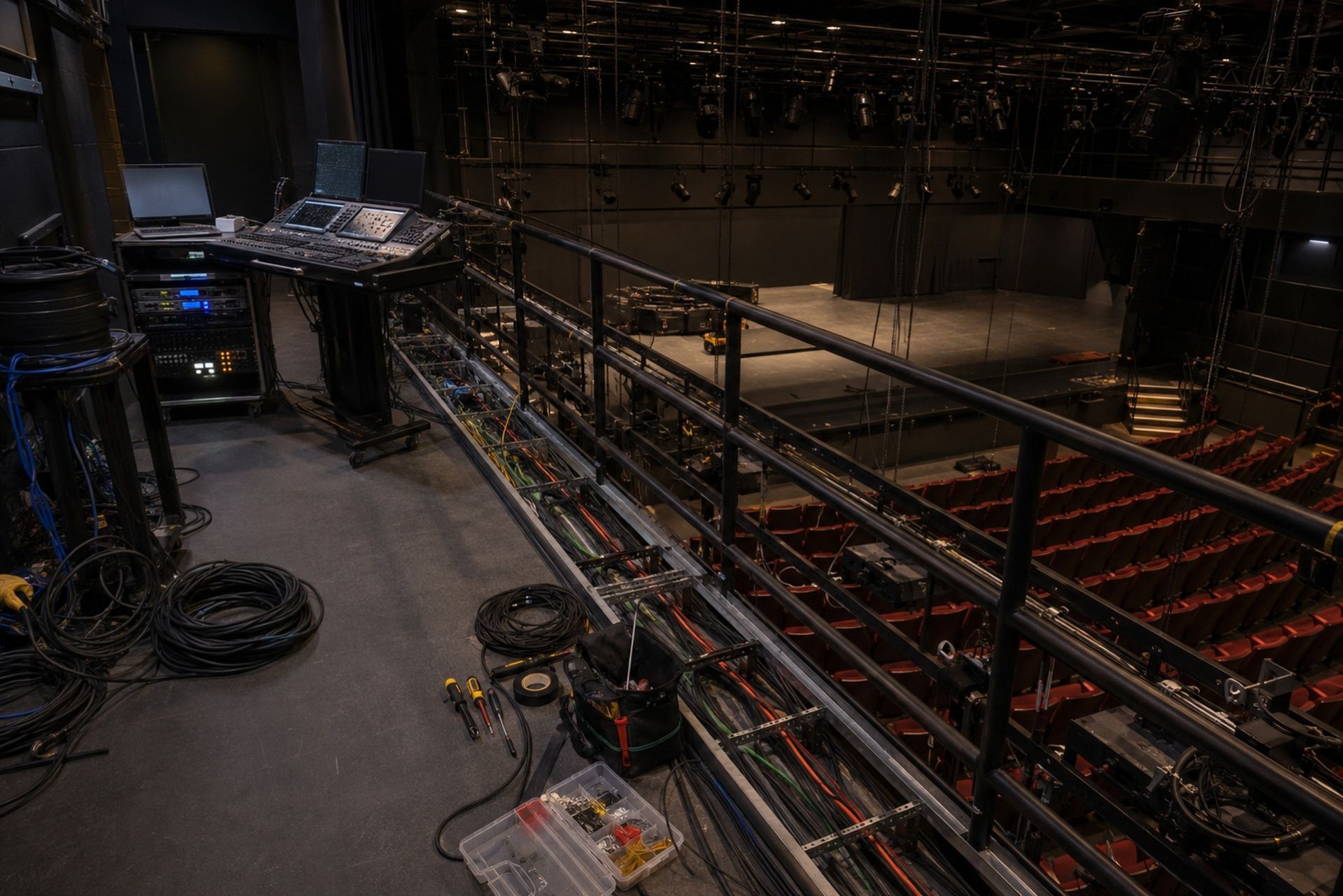

Stage electricians routinely work at heights that would make most commercial electricians uncomfortable. Hanging and focusing instruments from catwalks, loading galleries, and fly systems means your workers' comp classification reflects that elevated risk. The NCCI class code for theater electrical work carries higher experience modification factors than standard commercial electrical work.

If you have employees working on scaffolding, in cherry pickers, or on catwalks above 20 feet, your workers' comp premiums will reflect that exposure. One thing to keep in mind: misclassifying your workers as standard commercial electricians to save on premiums is a fast path to an audit surcharge and potential fraud investigation.

By: Michael Fusco

President of Joule Pro

INDEX

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Specialty Risks and Niche Coverage Extensions

The standard contractor policy leaves major gaps for stage electricians. These extensions fill them.

Inland Marine for Portable Lighting and Sound Gear

Stage electricians often own or are responsible for tens of thousands of dollars in portable equipment: lighting instruments, dimmers, cables, control consoles, and rigging hardware. Your standard property policy covers equipment at your shop. Inland marine covers it everywhere else: in transit, at venues, in storage trailers.

A program like the one offered through Joule Pro can structure inland marine coverage specifically for electrical contractors who move expensive gear between job sites. For stage electricians, that means coverage for equipment sitting in a loading dock at 2 AM between shows, not just equipment bolted to your shop wall.

Pyrotechnic and Special Effects Liability Endorsements

If your work involves any pyrotechnic effects, flash pots, or fog machines with electrical ignition systems, you need a specific endorsement. Standard GL policies exclude pyrotechnic-related claims entirely. The endorsement typically adds 15% to 25% to your GL premium, but without it, you have zero coverage for one of the highest-risk activities in theater production.

Even if you're just wiring the ignition circuits and someone else handles the pyrotechnics, your involvement in the electrical triggering system can pull you into a claim. Get the endorsement.

Rigger's Liability for Overhead Electrical Installations

Overhead electrical work in theaters involves rigging motorized lighting bars, installing chain hoists, and running power to instruments suspended above performers and audiences. Rigger's liability coverage addresses claims arising from the failure of overhead installations.

This is separate from your GL because rigging failures carry catastrophic injury potential. A lighting truss that falls into an audience creates the kind of claim that can exceed standard policy limits within hours. Rigger's liability endorsements typically provide $1 million to $5 million in additional coverage specifically for overhead installation failures.

Understanding Carrier Appetite in the Entertainment Sector

Not every insurance carrier wants to write stage electrician business. Knowing which ones do, and what they're looking for, saves you months of shopping.

Preferred Risks: Resident Technicians vs. Touring Crews

Carriers strongly prefer resident technicians who work at a single venue or a small rotation of known theaters. The risk profile is predictable: same building, same electrical systems, same safety protocols. These accounts get the best rates.

Touring crews are harder to place. You're working in a different venue every week, dealing with unfamiliar electrical systems, and often under intense time pressure for load-in. Carriers that write touring crew policies want to see detailed safety protocols, OSHA 10 or 30 certifications for all crew members, and a clean loss history going back at least three years. Specialty programs, like those built by Joule Pro through their underwriter relationships in the electrical trades, are often the most efficient path to coverage for touring operations.

Hazardous Classifications: Temporary Power and Outdoor Events

Outdoor events and temporary power installations push you into hazardous classification territory. Festival work, outdoor theater, and concert touring all involve temporary power distribution: generators, spider boxes, and cam-lock connections exposed to weather. Carriers view this work as significantly riskier than permanent venue installations.

Expect premium surcharges of 20% to 40% for policies that include outdoor temporary power work. Some carriers won't write it at all. If outdoor events are a significant part of your business, you need a broker who specializes in entertainment or electrical contractor placements, not a generalist who has to shop your account to 15 carriers before finding one that will even quote it.

Trade-Specific Policy Components and Clauses

The fine print in your policy matters more than the declarations page. These clauses determine whether your coverage actually works when you need it.

Care, Custody, and Control Exclusions in Venue Settings

This is the clause that burns stage electricians most often. Your GL policy excludes damage to property in your care, custody, or control. When you're working on a venue's electrical system, that system is arguably in your care. If you damage a theater's dimmer rack while servicing it, your GL policy may deny the claim under this exclusion.

The fix is an installation floater or a care, custody, and control endorsement that specifically covers venue property you're working on. Without it, you're self-insuring every piece of venue equipment you touch.

| Coverage Type | What It Covers | Typical Annual Cost | Who Needs It |

|---|---|---|---|

| General Liability | Third-party bodily injury, property damage | $2,500 - $8,000 | All stage electricians |

| Professional Liability | Design errors, consulting mistakes | $1,200 - $3,500 | Electricians who design or consult |

| Inland Marine | Portable equipment in transit/on-site | $800 - $3,000 | Anyone transporting gear |

| Rigger's Liability | Overhead installation failures | $1,500 - $4,500 | Electricians doing overhead rigging |

| Pyro Endorsement | Special effects electrical work | 15-25% GL premium increase | Anyone near pyrotechnics |

Waiver of Subrogation for Venue Contracts

Almost every venue contract requires a waiver of subrogation. This means your insurance carrier agrees not to pursue the venue's insurance company to recover claim payments, even if the venue was partially at fault. It's standard in the industry, but you need to request it from your carrier before signing the venue contract, not after a claim.

Most carriers add waivers of subrogation for a small additional premium, typically $50 to $200 per waiver. The catch is that some carriers limit the number of waivers per policy period. If you're working 30 different venues a year, make sure your policy allows blanket waivers.

Risk Management and Premium Reduction Strategies

Smart risk management doesn't just prevent claims: it directly lowers your premiums.

Safety Certification Impacts on Underwriting

ETCP (Entertainment Technician Certification Program) certification is the gold standard for stage electricians, and underwriters notice it. Certified electricians demonstrate verifiable competence in electrical safety, rigging, and venue-specific protocols. Carriers that write entertainment risks often offer 5% to 15% premium credits for ETCP-certified staff.

OSHA 30 certification, first aid/CPR training, and documented safety meetings also factor into underwriting decisions. Keep records of everything. A well-documented safety program is your strongest negotiating tool at renewal.

Contractual Indemnification and Additional Insured Status

Production companies and venues will ask you to indemnify them in your contracts and add them as additional insureds on your policy. This is normal, but read the indemnification language carefully. Broad-form indemnification clauses can make you responsible for the venue's own negligence, not just yours.

Work with your insurance professional to review contract language before signing. A program like Joule Pro, backed by Fusco Orsini & Associates Insurance Services, gives you direct access to a licensed producer who can review these clauses and confirm your policy will respond as expected. That's the kind of support that matters when a venue hands you a 40-page contract at load-in and expects it signed before you plug in a single cable.

FAQ

Do I need separate insurance if I work as both a stage electrician and a residential electrician? Yes. The risk profiles and policy structures are different enough that you'll likely need endorsements or separate policies to cover both operations properly.

Will my insurance cover rented lighting equipment? Only if you have an inland marine policy or rented equipment endorsement. Your standard GL policy excludes property in your care, custody, or control.

How do I get insurance for touring work if carriers keep declining my application? Specialty programs focused on electrical contractors have established relationships with carriers that understand entertainment risk. A generalist agent often can't access these markets.

Does my policy cover me if a performer is injured by a lighting failure? Your GL policy covers third-party bodily injury, including performers, as long as the failure resulted from your covered operations and not an excluded activity.

What happens if I don't have a waiver of subrogation and a venue requires one? You'll likely be unable to work at that venue until you obtain one from your carrier. Most carriers can add them quickly, but don't wait until the day of load-in.

Making the Right Choice for Your Stage Electrician Coverage

Stage and theater electrical work sits at the intersection of high-voltage risk and high-value assets, and your insurance needs to reflect that reality. The right policy isn't just a GL certificate you hand to a venue manager: it's a carefully constructed stack of coverages that addresses everything from overhead rigging failures to errors in your lighting design.

Don't settle for a generalist agent who treats you like every other electrician. Find a specialty program that understands entertainment electrical work, reviews your contracts, and builds coverage around your actual operations. If you're ready to get a policy that matches the complexity of your trade, reach out to Joule Pro for a quote built specifically for licensed electrical contractors.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.