Business Insurance

Self-Employed Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

A single spark can cause a house fire. A misrouted wire can trigger an arc fault weeks after you leave the job site. And if a client trips over your extension cord and breaks a wrist, you're the one getting the call from their attorney. Running your own electrical business means absorbing risks that a W-2 employee never thinks about, and the right insurance is what stands between a bad day on the job and a financial catastrophe.

This guide covers the full insurance picture for self-employed electricians: general liability, workers' comp, tools and equipment coverage, commercial auto, and the trade-specific risks that generic business policies tend to miss. Solo residential electricians in 2026 should budget between $3,000 and $5,000 annually for a comprehensive insurance package, though your actual costs depend on revenue, location, and the type of work you take on. That's a real number worth planning around, not a vague "it depends."

Essential Liability Protection for Electrical Contractors

Liability coverage is the foundation of any electrician's insurance program. Without it, you're one lawsuit away from losing everything you've built. The three forms below each protect against different scenarios, and most self-employed electricians need all of them.

General Liability: Protecting Against Property Damage and Bodily Injury

General liability (GL) insurance covers third-party bodily injury and property damage that happens during your work. If you accidentally drill through a water pipe while running conduit and flood a client's kitchen, GL pays for the damage. If a homeowner trips over your toolbox and needs stitches, GL covers the medical bills and any legal defense costs.

Most general contractors and property managers won't let you on a job site without a certificate of insurance showing at least $1 million per occurrence and $2 million aggregate in GL coverage. These are standard minimums in the electrical trade, and some commercial projects require higher limits. Your GL policy also covers advertising injury claims, like if a competitor alleges you copied their business name or marketing.

One thing to keep in mind: GL does not cover faulty workmanship itself. It covers the resulting damage, but not the cost to redo your own work. That distinction matters more than most electricians realize until they file a claim.

Completed Operations and Product Liability

Here's where things get interesting for electricians specifically. Completed operations coverage, which is typically included in your GL policy, protects you after you've finished a job and left the site. If a panel you installed six months ago causes a fire due to a defective breaker, completed operations responds to the claim.

Product liability works similarly but applies when a product you installed or recommended fails. Electrical contractors face unique product liability exposure because you're installing components manufactured by others. If a client's home is damaged by a faulty GFCI outlet you supplied and installed, you could be named in the lawsuit alongside the manufacturer.

Many electricians don't realize their completed operations coverage has a separate aggregate limit. Check your policy declarations page to confirm your limits haven't been eroded by prior claims during the policy period.

Professional Liability and Errors & Omissions

If you design electrical systems, create load calculations, or provide consulting services, professional liability (also called errors and omissions, or E&O) fills a gap that GL doesn't touch. GL covers physical damage. E&O covers financial losses caused by your professional advice or design errors.

Say you spec an undersized panel for a commercial tenant improvement, and the client has to shut down operations for three days while it's replaced. The client's lost revenue isn't a GL claim: it's an E&O claim. Electricians who pull their own permits and create their own plans carry more E&O exposure than those who work strictly from engineer-stamped drawings.

E&O policies for electricians typically run $500 to $1,500 per year depending on your revenue and scope of services. If you're doing any design-build work, this coverage is not optional.

By: Michael Fusco

President of Joule Pro

INDEX

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

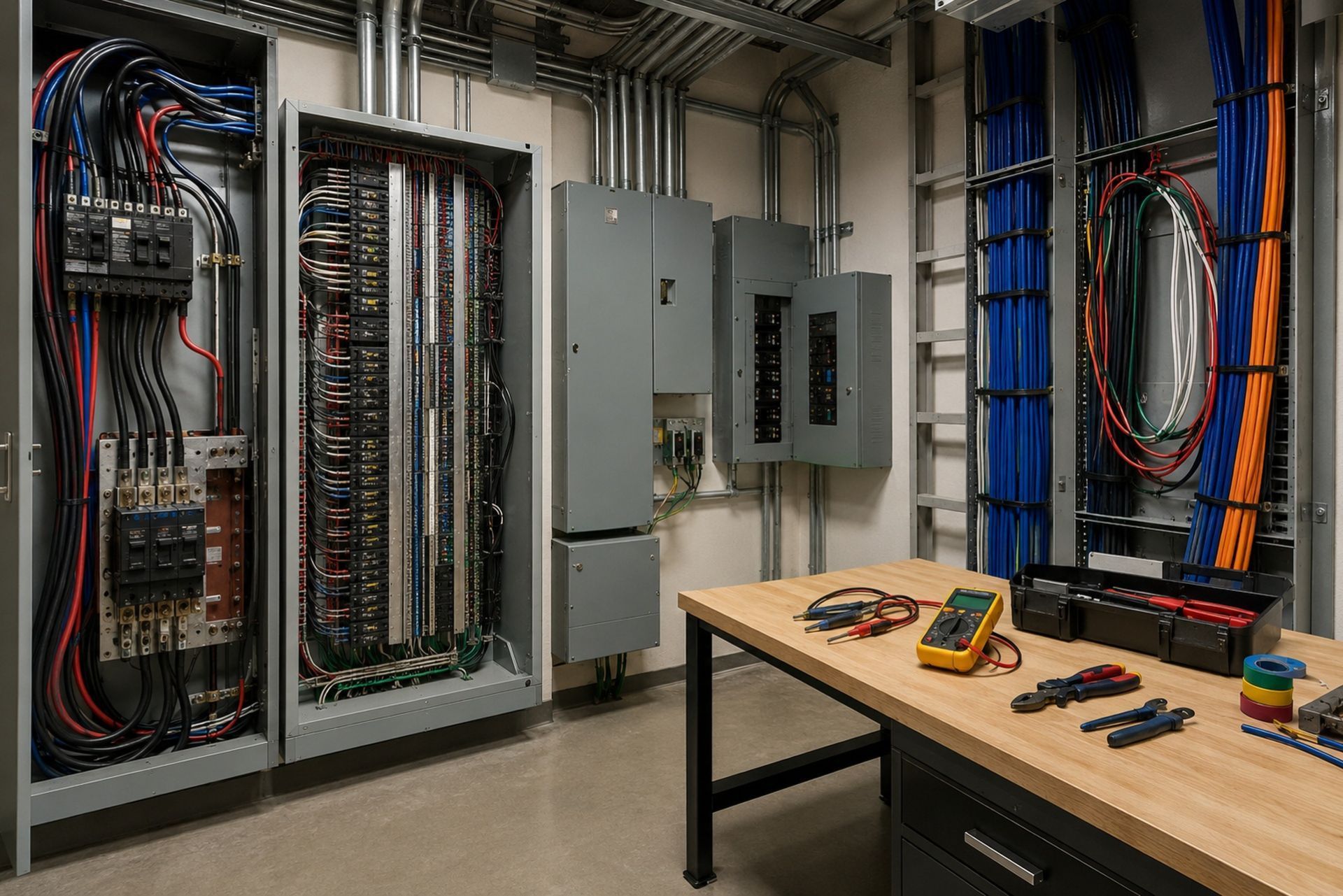

Protecting Your Assets: Tools, Equipment, and Vehicles

Your tools and your truck are how you make a living. Losing either one to theft, an accident, or a fire can shut your business down overnight.

Inland Marine Insurance for Tools and Mobile Equipment

Despite the confusing name, inland marine insurance has nothing to do with boats. It covers tools, equipment, and materials in transit or stored at job sites: basically anything that moves around with you. A standard business property policy only covers items at your listed business location, which doesn't help when $15,000 worth of meters, benders, and power tools gets stolen from a job site trailer.

Inland marine policies for electricians typically cover:

- Hand and power tools (owned or leased)

- Testing and diagnostic equipment like meggers and thermal cameras

- Materials and supplies in transit

- Rented or borrowed equipment (with the right endorsement)

Replacement cost coverage is worth the small premium increase over actual cash value. A five-year-old Fluke meter still costs the same to replace as a new one, and depreciated payouts leave you short. Programs like Joule Pro, which is built specifically for licensed electrical contractors, can structure inland marine coverage that matches the way electricians actually work: tools spread across vans, shops, and active job sites.

Commercial Auto Insurance for Work Vans and Trucks

Your personal auto policy almost certainly excludes business use. If you're hauling tools and materials to job sites in your van, you need a commercial auto policy. Period. A personal policy claim denial after a work-related accident is one of the most common and most expensive surprises self-employed electricians face.

Commercial auto covers liability, collision, and comprehensive damage for vehicles used in your business. It also extends to hired and non-owned auto situations: if you rent a truck for a large project or if a helper uses their personal vehicle for a work errand, you're still protected.

Coverage limits of $1 million combined single limit are standard for most electrical contractors. If you tow a trailer with equipment, make sure your policy includes trailer coverage and adequate limits for the contents inside.

Workers' Compensation and Personal Income Protection

Legal Requirements for Workers' Comp as a Sole Proprietor

Workers' comp requirements vary dramatically by state. In California, for example, all employers must carry workers' compensation even if they have just one employee. Some states allow sole proprietors with no employees to exempt themselves, while others require it regardless.

Here's the practical reality: even in states where you can opt out as a sole proprietor, many general contractors and commercial clients require you to carry workers' comp before they'll hire you. If you don't have it, they have to add you to their policy, which they'll either refuse to do or deduct from your pay.

| Situation | Workers' Comp Required? | Recommended? |

|---|---|---|

| Solo, no employees (most states) | Often optional | Yes, if GCs require it |

| Solo, no employees (CA, NY, certain states) | May be required | Yes |

| 1+ employees (all states) | Yes | Yes |

| Using subcontractors | Depends on state classification | Yes, verify sub's coverage |

If you hire even one part-time helper, you almost certainly need workers' comp. The penalties for non-compliance range from fines to criminal charges depending on your state.

Disability Insurance: Securing Your Income After an Injury

Workers' comp covers on-the-job injuries. But what happens if you blow out your knee playing basketball on a Saturday, and you can't climb ladders for three months? That's where disability insurance comes in.

Short-term disability policies typically replace 60% of your income for up to six months. Long-term disability kicks in after that and can continue for years or until retirement age. For a self-employed electrician earning $80,000 to $120,000 annually, a good disability policy costs roughly $100 to $300 per month.

This is the coverage most sole proprietors skip, and it's the one that destroys the most businesses. Your body is your primary asset. Protect it.

Navigating Trade-Specific Risks and Endorsements

Pollution Liability for Hazardous Material Handling

Standard GL policies exclude pollution-related claims. If you're working in older buildings, you may encounter asbestos, lead paint, or PCB-containing ballasts. Disturbing these materials, even accidentally, can trigger cleanup costs and health claims that your GL policy won't touch.

A pollution liability endorsement or standalone policy fills this gap. It covers cleanup costs, third-party bodily injury from pollutant release, and legal defense. Electricians doing renovation or retrofit work in pre-1980 buildings should seriously consider this coverage. A single asbestos disturbance claim can easily exceed $100,000.

Cyber Liability for Digital Client Records and Invoicing

If you store client information digitally, accept credit card payments, or use cloud-based project management tools, you have cyber exposure. A data breach affecting client financial information triggers notification requirements in all 50 states, and the costs add up fast.

Cyber liability policies for small contractors typically cost $500 to $1,000 per year and cover breach notification expenses, credit monitoring for affected clients, and legal defense. This is increasingly relevant as more electricians move to digital invoicing and smart-home system installations that connect to client networks.

Determining Costs and Choosing the Right Policy

Factors Influencing Electrician Insurance Premiums

Your premiums depend on several interconnected factors. Revenue is the biggest driver for GL: a $500,000-revenue operation pays significantly more than a $150,000 one. Your NCCI classification code (typically 5190 for electrical wiring) determines your base workers' comp rate, and your experience modification rate adjusts it based on your claims history.

Other factors include your geographic location, years in business, types of projects (residential vs. commercial vs. industrial), and whether you do any high-voltage work. An electrician doing residential service calls in a suburban area will pay far less than one pulling wire in industrial plants.

Bundling Coverage with a Business Owner's Policy (BOP)

A Business Owner's Policy bundles GL, commercial property, and business income coverage into a single policy, usually at a lower combined premium than buying each separately. For self-employed electricians with a shop or office, a BOP can save 10% to 15% compared to standalone policies.

That said, a BOP won't cover everything. You'll still need separate policies for commercial auto, workers' comp, inland marine, and any specialty endorsements. Working with a program like Joule Pro, backed by Fusco Orsini & Associates Insurance Services, gives you access to specialty markets and underwriter relationships that understand electrical trade risks, so your coverage actually fits your business instead of forcing you into a generic contractor template.

Your Next Steps

Getting the right coverage isn't about buying the cheapest policy you can find. It's about building a coverage stack that matches the specific risks you face as an electrician: fire damage claims, completed operations exposure, tool theft, and the physical demands that could sideline you without warning. Start by assessing your current gaps. Do you have completed operations coverage? Is your van actually covered for business use? Would a disability keep you from paying your mortgage?

A specialty insurance producer who works exclusively with electrical contractors can identify gaps that a general agent might miss. Reach out to Joule Pro for a coverage review tailored to your trade, your revenue, and the types of projects you take on. The best time to fix a coverage gap is before you need to file a claim.

FAQ

Do I need insurance if I only do side jobs on weekends? Yes. Your exposure to liability exists regardless of whether electrical work is your full-time gig. A single property damage or injury claim can exceed $50,000 easily.

Can I use my personal auto insurance for my work van? Almost never. Personal auto policies exclude vehicles used for business purposes. If you're hauling tools to job sites, you need commercial auto coverage.

How much general liability coverage do I actually need? Most clients and general contractors require $1 million per occurrence and $2 million aggregate as a minimum. Some commercial and government projects require $5 million, typically achieved with an umbrella policy.

What's the difference between inland marine and a tools floater? They're essentially the same thing. "Tools floater" is an older term for the inland marine coverage that protects portable tools and equipment away from your primary business location.

Does my insurance cover work done by a subcontractor I hire? Your GL policy may extend some coverage, but you should always verify that your subs carry their own insurance and add you as an additional insured on their policies.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.