Business Insurance

Tools and Equipment Insurance For Electricians

★★★★★ 150+ Five-Star Reviews · Google & Facebook

A single van break-in can wipe out $15,000 worth of Fluke meters, Megger testers, and cordless tool kits overnight. For most electrical contractors, tools aren't just equipment: they're the revenue engine. Lose them, and you lose the ability to finish jobs, meet deadlines, and get paid. Yet a surprising number of electricians assume their general liability policy or commercial auto coverage handles tool theft and damage. It doesn't, and finding that out after a loss is a painful lesson.

This guide covers everything electrical contractors need to know about insuring their tools and equipment, from coverage limits and valuation methods to real claims scenarios and the exclusions that catch people off guard. Whether you're a solo journeyman running residential service calls or managing a crew handling commercial buildouts, understanding this coverage can mean the difference between a minor inconvenience and a financial hit that stalls your business for weeks.

The average monthly cost for this type of policy sits around $43 for small to mid-sized contractors, with annual premiums typically starting around $500. That's a fraction of what a single tool replacement could cost, which makes the math pretty straightforward.

Understanding Inland Marine Insurance for Electrical Contractors

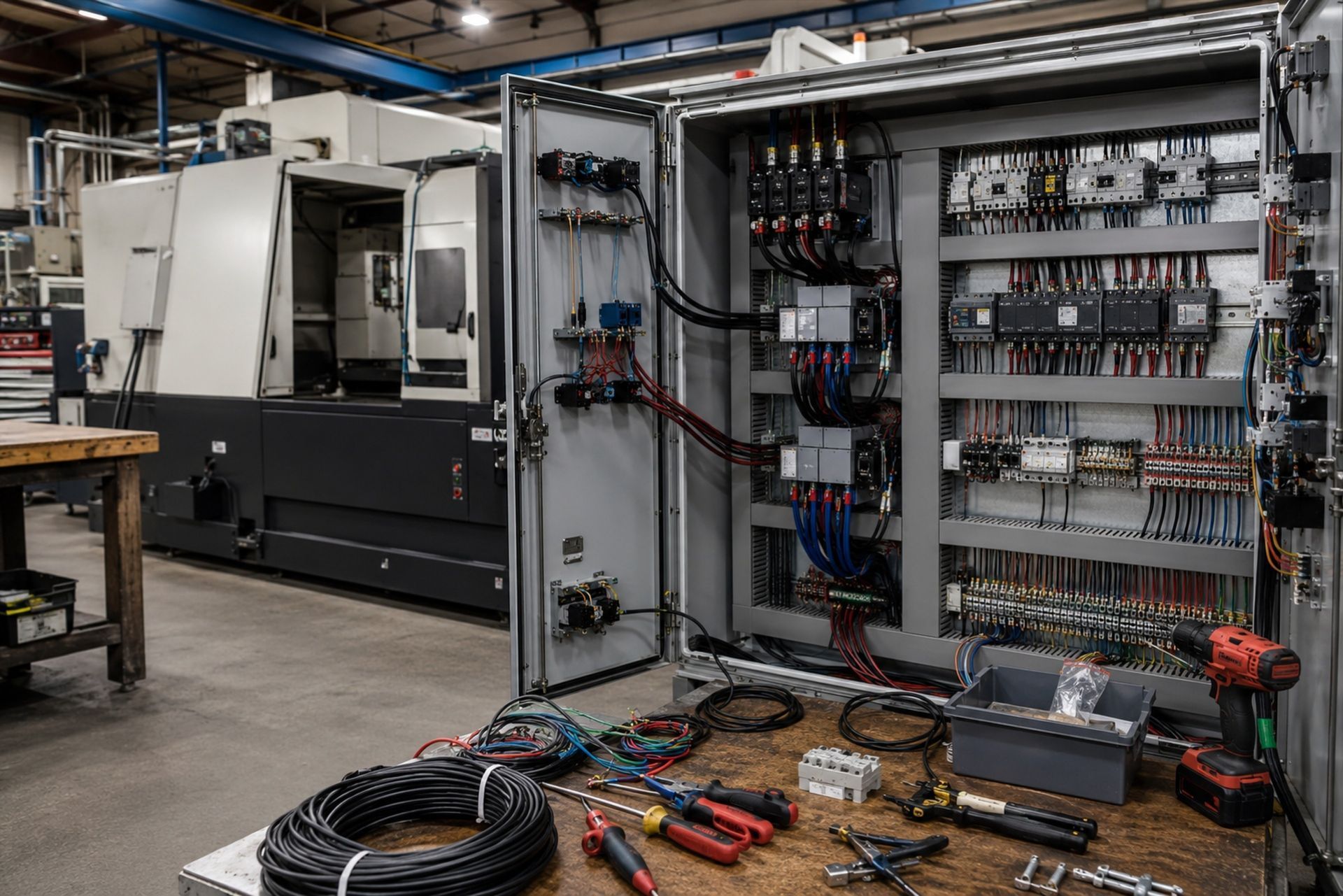

The term "inland marine" sounds like it belongs on a cargo ship, not in an electrician's insurance portfolio. But inland marine insurance is the industry name for coverage that protects property in transit or stored at locations other than your primary business address. For electricians, that means your tools, testing equipment, and portable machinery are covered whether they're in your van, on a jobsite, or temporarily stored in a client's garage.

This is the policy type that actually protects your gear. It's designed for property that moves, which is exactly how electrical contractors operate. You're not working from a fixed location with everything bolted to the floor. Your Fluke 1587 insulation tester rides in the van. Your conduit bender sits on a trailer. Your wire pullers go wherever the job is. Inland marine coverage follows those items.

Why Standard General Liability Isn't Enough for Your Gear

General liability protects you when you cause damage to someone else's property or when a third party gets injured because of your work. It does not cover your own tools. If your $3,500 thermal imaging camera falls off a ladder and shatters, GL won't pay for it. If someone steals your Milwaukee M18 kit from a jobsite, GL won't reimburse you.

Commercial auto insurance covers the vehicle itself and sometimes permanently installed equipment like ladder racks. But the tools inside? Those are considered "contents," and most commercial auto policies either exclude them entirely or cap coverage at absurdly low amounts, sometimes just $500. That's barely enough to replace a decent set of pliers and a headlamp.

The Difference Between Scheduled and Unscheduled Tool Coverage

Scheduled coverage means you list specific high-value items on the policy with their individual values. Think of your oscilloscope, your power quality analyzer, or a specialized cable puller. Each item gets its own line and its own coverage amount.

Unscheduled coverage provides a blanket limit that covers all your tools collectively without itemizing each one. This works well for hand tools and lower-value power tools where tracking every item individually would be impractical.

Most electrical contractors benefit from a hybrid approach: schedule your expensive diagnostic and testing equipment individually while keeping a blanket unscheduled limit for everything else. Joule Pro structures policies this way for electrical contractors specifically, which helps avoid gaps that generalist agencies often miss.

By: Michael Fusco

President of Joule Pro

INDEX

Understanding Inland Marine Insurance for Electrical Contractors

Defining Coverage Limits and Valuation Methods

Common Policy Exclusions and Risk Mitigation

Real-World Claims Examples for Electrical Businesses

How to Properly Document Inventory for Faster Payouts

Selecting the Right Policy for Your Specific Electrical Niche

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Defining Coverage Limits and Valuation Methods

Getting the right coverage amount matters just as much as having the policy in the first place. Underinsure your tools and you'll collect a check that doesn't come close to replacing what you lost.

Replacement Cost vs. Actual Cash Value for Specialized Testers

These are the two main ways insurers value your equipment at the time of a claim:

| Factor | Replacement Cost | Actual Cash Value (ACV) |

|---|---|---|

| What you receive | Full cost of a new equivalent item | Depreciated value based on age and condition |

| Premium cost | Higher | Lower |

| Best for | Expensive testers, newer equipment | Older tools nearing end of life |

| Example payout | $4,200 for a new Fluke 1760 | $1,800 for a 5-year-old Fluke 1760 |

For specialized electrical testing equipment, replacement cost coverage is almost always the right call. A Megger insulation tester that cost $2,800 three years ago still costs $2,800 to replace today, but ACV might only pay you $1,400. That gap comes straight out of your pocket.

Per-Item Limits and Aggregate Policy Caps

Most policies set both a per-item limit and a total aggregate cap. A typical policy might have a $2,500 per-item limit with a $25,000 aggregate. If your most expensive single tool is a $6,000 power quality analyzer, you need to schedule it separately or raise your per-item limit.

Review your aggregate cap against your total inventory value annually. Electrical contractors tend to accumulate tools gradually, and it's easy to outgrow your coverage without realizing it. A quick annual inventory check prevents nasty surprises.

Common Policy Exclusions and Risk Mitigation

Every insurance policy has exclusions, and tools and equipment coverage for electricians is no exception. Knowing what isn't covered is just as important as knowing what is.

Wear, Tear, and Mechanical Breakdown Exclusions

Your policy won't pay for tools that simply wear out from normal use. A drill motor that burns out after five years of daily use isn't a covered loss. Neither is a battery that no longer holds a charge or a meter that drifts out of calibration.

Some policies also exclude mechanical or electrical breakdown unless you add a specific endorsement. This matters for expensive diagnostic equipment with electronic components. If your thermal imager's sensor fails outside of warranty, a standard inland marine policy likely won't cover the repair. Ask about equipment breakdown endorsements if you rely on high-value electronic testers.

Theft from Unattended Vehicles and Jobsite Security Requirements

Here's where claims get denied most often. Many policies require that vehicles be locked and that tools be stored in a secured, enclosed compartment, not just sitting on the passenger seat. Some insurers require additional security measures like GPS tracking on high-value items or locking toolboxes bolted to the truck bed.

Jobsite theft is another common trigger for claim denials. If your policy requires tools to be stored in a locked gang box or secured trailer overnight and you left them sitting on the floor of an open construction site, the insurer has grounds to deny the claim. Read your policy's security requirements carefully and follow them consistently.

Real-World Claims Examples for Electrical Businesses

Abstract policy language makes more sense when you see how it plays out in actual scenarios.

Scenario: Van Break-ins and Power Tool Extraction

A residential electrician parks his work van in his driveway overnight. Someone smashes the rear window and takes two Milwaukee M18 FUEL combo kits, a Fluke 87V multimeter, a Fluke 1587 insulation tester, and assorted hand tools. Total loss: roughly $8,500.

With a properly structured inland marine policy, the contractor files a claim, provides the police report and purchase receipts, and receives a replacement cost payout within two to three weeks. Without coverage, he's buying everything out of pocket and likely missing a week of billable work while he scrambles to re-equip.

The key detail: the van was locked, and the tools were in an enclosed cargo area. If the van had been left unlocked, the claim could have been denied based on the security requirements discussed earlier.

Scenario: Damage to Rented Conduit Benders and Scissor Lifts

A commercial electrical contractor rents a hydraulic conduit bender for a large office buildout. During transport, the bender falls off the trailer and sustains $4,000 in damage. The rental company holds the contractor responsible.

Most inland marine policies cover rented equipment, but there are limits and conditions. Some policies cap rented equipment coverage at a lower amount than owned equipment. Others require you to list rented items if they exceed a certain value. The contractor in this case had rented equipment coverage through his inland marine policy, which paid the rental company directly after a $500 deductible.

For scissor lifts and other heavy equipment rentals, check whether the rental company's damage waiver or your own policy provides better coverage. Sometimes carrying your own coverage and declining the rental waiver saves money, but only if your policy explicitly covers rented equipment at adequate limits.

How to Properly Document Inventory for Faster Payouts

The speed of your claim payout depends almost entirely on how well you've documented your inventory before the loss occurs. Insurers aren't going to take your word for it that you had $20,000 in tools.

Here's what actually speeds up claims:

- Keep a running spreadsheet with item descriptions, serial numbers, purchase dates, and costs

- Photograph or video-record your van contents and shop inventory quarterly

- Save digital copies of receipts in cloud storage: not just in the van that might get stolen

- Update your inventory list whenever you buy or replace a significant tool

- Store a copy of your inventory documentation somewhere separate from the tools themselves

Joule Pro recommends that electrical contractors maintain this documentation as part of their broader risk management program. When a claim hits, contractors who can hand over a clean inventory list with receipts typically see payouts processed in half the time compared to those who have to reconstruct their inventory from memory.

One practical tip: use your phone to snap a photo of every new tool receipt the day you buy it and email it to yourself. It takes five seconds and creates a timestamped digital record that's hard to dispute.

Selecting the Right Policy for Your Specific Electrical Niche

Not all electrical contractors face the same risks, and your policy should reflect your specific operation. A solar installation company hauling expensive inverters and monitoring equipment has different needs than a residential service electrician carrying basic hand tools and a few meters.

Consider these factors when choosing coverage:

- Total tool and equipment inventory value, including diagnostic equipment

- Whether you rent heavy equipment regularly

- How many vehicles carry tools

- Whether employees take tools home or store them at the shop

- Your typical jobsite security conditions

A specialty insurance program built for electrical contractors, like Joule Pro, can match these variables to the right policy structure because they understand the trade. Generalist agencies often default to cookie-cutter inland marine policies that leave gaps for trade-specific equipment like wire pullers, cable testers, and conduit threading machines.

Get quotes from at least two providers, but make sure at least one specializes in contractor coverage. The premium difference is usually small, but the coverage differences can be significant when you file a claim.

Frequently Asked Questions

Does my homeowner's policy cover tools stolen from my work van? Generally no. Most homeowner's policies exclude business property or limit it to very small amounts, often $2,500 or less. A dedicated inland marine policy is the proper coverage.

Can I insure tools my employees own? Typically, your policy covers tools owned by the business. Employee-owned tools usually need to be covered under the employee's own policy or added to yours with a specific endorsement.

What's the typical deductible for a tools and equipment claim? Deductibles usually range from $250 to $1,000, depending on the policy and your total coverage amount. Higher deductibles lower your premium but increase your out-of-pocket cost per claim.

Are tools covered if I leave them at a client's property overnight? It depends on your policy's terms. Most policies cover tools at jobsites, but many require them to be in a locked container or secured area. Leaving tools unsecured could void coverage for theft.

Do I need separate coverage for each work vehicle? Most inland marine policies cover your tools regardless of which vehicle they're in, but confirm this with your agent. Some policies tie coverage to specific vehicles listed on the policy.

Making the Right Choice for Your Business

Protecting your tools isn't complicated, but it does require attention to the details: proper valuation, adequate limits, honest inventory documentation, and understanding your exclusions. The cost of coverage is minimal compared to the cost of replacing a van full of specialized electrical equipment out of pocket.

If you're unsure whether your current policy actually covers what you think it does, pull it out and read the exclusions section. That's where the real answers live. And if you want a policy specifically designed for the way electrical contractors actually work, reach out to Joule Pro for a quote from a licensed professional who understands your trade inside and out.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.