Business Insurance

Texas Commercial Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

Underwriting Preferences for Residential vs. Industrial Projects

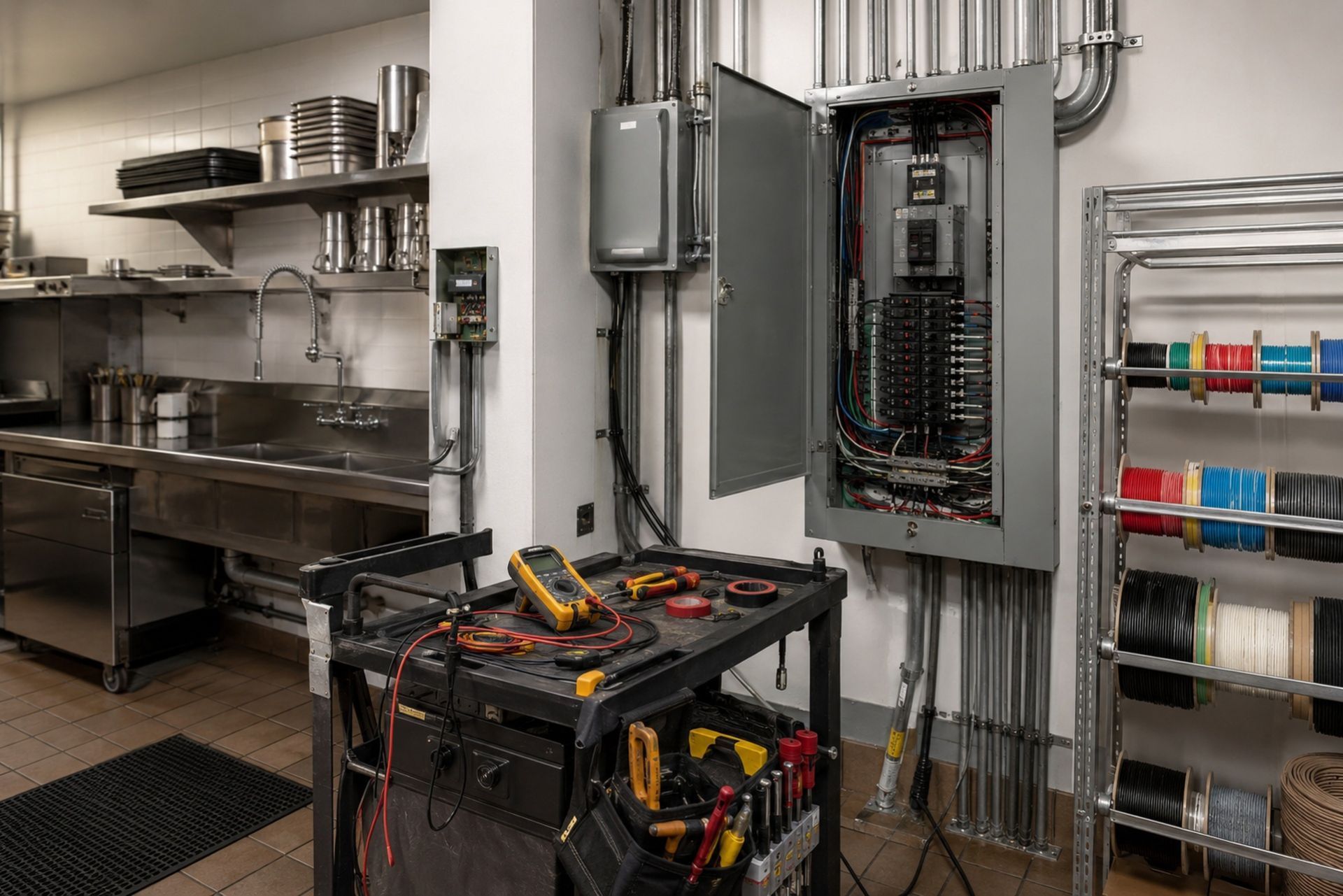

Running an electrical contracting business in Texas means dealing with risks that most general contractors never face: arc flash incidents, fire liability from faulty wiring, expensive tools stolen from job sites, and workers' comp claims that can shut down a small shop overnight. The state's construction market continues to boom, with data centers, commercial build-outs, and industrial facilities driving demand for licensed electricians across the DFW Metroplex, Houston, Austin, and San Antonio. But that growth comes with exposure, and the wrong insurance setup can leave you personally liable for six- or seven-figure claims.

Getting the right insurance coverage as a Texas electrical contractor isn't just about checking a box for your license renewal. It's about structuring policies that actually respond when something goes wrong on a job site, in transit, or years after a project wraps up. This guide covers the specific policies you need, how Texas licensing requirements shape your insurance obligations, the trade-specific risks that keep underwriters up at night, and what carriers actually look for when they decide whether to write your policy.

Essential Insurance Policies for Texas Commercial Electricians

Every commercial electrician in Texas needs a core stack of policies working together. Missing one piece can create a gap that voids another policy's coverage or leaves you exposed to a claim type you assumed was covered. Here's what that stack looks like and why each piece matters.

General Liability and Completed Operations Coverage

Commercial general liability (CGL) is the foundation. It covers bodily injury and property damage claims arising from your work, both while you're on the job and after you leave. For electricians, the "completed operations" portion is arguably more important than the premises/operations coverage. Why? Because electrical failures often show up months or years after installation. A panel you wired in 2025 that causes a fire in 2027 triggers your completed operations coverage, not your standard ops coverage.

Most Texas general contractors require subcontractors to carry at least $1 million per occurrence and $2 million aggregate in GL coverage. Many larger commercial projects demand higher limits or umbrella policies on top. One mistake electricians make is buying the cheapest GL policy without checking whether completed operations coverage is included or excluded. Some carriers write it separately or cap it at a lower limit. A specialty program like Joule Pro structures these policies specifically for electrical contractors, so the completed operations coverage matches the actual risk profile of the trade.

Workers' Compensation in the Lone Star State

Texas is one of the few states where workers' comp isn't technically mandatory for private employers. That said, going without it is a terrible idea. Non-subscribers lose critical legal protections and face unlimited liability in employee injury lawsuits. Texas approved an average 11.5% decrease in workers' compensation loss cost benchmarks effective July 1, 2025, which means rates have been trending favorably for contractors with clean safety records.

For electrical contractors specifically, workers' comp classification codes (like 5190 for electrical wiring) carry moderate to high rates because of the inherent danger of the work. Your experience modification rate, or e-mod, directly affects your premium. An e-mod below 1.0 means you're safer than average; above 1.0 means you're paying a surcharge.

Commercial Auto and Inland Marine for Tools and Equipment

Your trucks, vans, and trailers need commercial auto coverage, not personal auto policies. Personal policies exclude vehicles used for business, and a single denied claim can cost you everything. Texas requires minimum liability limits of 30/60/25, but most contractors carry $1 million combined single limit to meet contract requirements.

Inland marine coverage protects your tools, equipment, and materials in transit or stored at job sites. A standard business property policy only covers items at your listed business location. If someone breaks into your van and steals $15,000 worth of meters, conduit benders, and power tools, inland marine is what pays that claim. Joule Pro bundles this coverage into its contractor programs because tool theft and job site losses are so common in the electrical trades.

By: Michael Fusco

President of Joule Pro

INDEX

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Texas Department of Licensing and Regulation (TDLR) Requirements

Mandatory Liability Limits for Master and Journeyman Licenses

The Texas Department of Licensing and Regulation requires all licensed electrical contractors to maintain general liability insurance as a condition of licensure. Master electricians must carry a minimum of $300,000 in general liability coverage to hold an active license. This is a floor, not a ceiling: most commercial projects require significantly higher limits.

Your license can be suspended or revoked if your insurance lapses. TDLR monitors this through certificate of insurance filings, and they don't give much grace period. If your carrier cancels your policy for non-payment and you don't replace it immediately, you risk losing your ability to pull permits and work legally in the state.

Certificate of Insurance (COI) Filing Procedures

TDLR requires that your insurance carrier or agent file a certificate of insurance directly with the department. This isn't something you can handle with a self-printed COI from your agent's portal. The filing must come from the insurer or authorized representative and must list TDLR as a certificate holder.

When you renew your license, TDLR cross-references your insurance filing. If there's a gap, your renewal gets flagged. The practical advice here: work with an agent or program that handles COI filings routinely for electrical contractors. A generalist agent who writes one electrician policy a year might not know the TDLR filing process, which creates unnecessary delays and compliance headaches.

Mitigating High-Risk Electrical Exposures

Arc Flash and Fire Hazard Liability

Arc flash incidents are among the most catastrophic events in the electrical trades. An arc flash can generate temperatures exceeding 35,000 degrees Fahrenheit, causing severe burns, blast injuries, and fatalities. From an insurance perspective, a single arc flash claim can easily exceed $1 million when you factor in medical costs, lost wages, and potential wrongful death litigation.

Carriers underwriting electrical contractors pay close attention to your arc flash safety protocols. Do you follow NFPA 70E standards? Do your crews use proper PPE and perform energized work permits? These aren't just safety questions: they're underwriting questions. A contractor with documented arc flash training and incident-free history gets better rates and broader coverage options than one who can't demonstrate basic compliance.

Fire liability is the other major exposure. Electrical fires account for a significant portion of commercial structure fires nationally. If a fire is traced back to your installation, you're looking at property damage claims, business interruption claims from the building owner, and potentially claims from neighboring tenants. Your completed operations coverage is what responds here, which circles back to why that coverage piece is so critical.

Professional Liability for Design-Build Projects

If your firm handles design-build electrical work, you need professional liability (errors and omissions) coverage. Standard GL policies exclude claims arising from professional services like engineering or design. A design error in a power distribution system that causes equipment damage or project delays falls outside your GL policy entirely.

This is a coverage gap that catches a lot of growing electrical firms off guard. As you take on more complex projects: data centers, solar installations, EV charging infrastructure, the design component increases, and so does your professional liability exposure.

Understanding Carrier Appetite for Texas Electrical Contractors

Preferred Risks vs. High-Hazard Classification

Not every insurance carrier wants to write electrical contractor policies. The trade carries inherent risks that make many standard market carriers uncomfortable. Carrier appetite refers to the types of businesses an insurer actively seeks versus those it avoids or prices aggressively to discourage.

Preferred electrical risks typically look like this:

- Clean loss history: Three to five years with minimal or no claims

- Licensed and compliant: Active TDLR license with no disciplinary actions

- Established safety programs: Written safety manuals, regular training, documented toolbox talks

- Moderate project scope: Commercial tenant improvements, service work, light industrial

High-hazard classifications include contractors doing high-voltage transmission work, petrochemical facility wiring, or heavy industrial installations. These risks require specialty carriers with specific appetite for hazardous electrical exposures.

Impact of Project Type on Underwriting and Premiums

| Factor | Lower Premium Impact | Higher Premium Impact |

|---|---|---|

| Project type | Commercial TI, retail, office | Industrial, petrochemical, utility |

| Voltage range | Under 600V | Over 600V, high-voltage |

| Annual revenue | Under $2M | Over $5M |

| Claims history | No claims, 3+ years | Multiple claims, open litigation |

| E-mod | Below 0.85 | Above 1.2 |

| Safety program | Written, documented, trained | No formal program |

Underwriters evaluate your entire risk profile, not just your classification code. Two electricians with the same revenue can see dramatically different premiums based on project mix, claims history, and safety documentation. Working with a program like Joule Pro that specializes in electrical contractor placements means your submission gets routed to carriers with genuine appetite for your specific risk profile, rather than getting declined by generalist underwriters who don't understand the trade.

Strategies for Lowering Insurance Costs and Managing Claims

Implementing Safety Programs and OSHA Compliance

The single most effective way to lower your insurance costs over time is reducing claims through genuine safety improvements. OSHA's electrical standards (29 CFR 1926 Subpart K for construction) provide the baseline, but carriers reward contractors who exceed minimums.

Practical steps that actually move the needle on your premiums:

- Conduct weekly documented toolbox talks focused on electrical hazards

- Maintain current CPR/First Aid and NFPA 70E certifications for all field employees

- Implement a formal lockout/tagout program with regular audits

- Track and report near-misses, not just actual incidents

These aren't just feel-good measures. Carriers review your safety documentation during audits and renewals. A well-documented program signals to underwriters that you're a lower risk, which translates directly to better pricing.

Navigating Multi-Year Claims History and Experience Modifiers

Your experience modifier follows you for three years. A bad year in 2024 is still affecting your 2026 and 2027 premiums. If you're carrying a high e-mod from past claims, the path back to competitive pricing requires consistent claim-free performance and proactive loss control.

One strategy that works: request a loss run from your current carrier and review it with your agent before renewal. Identify any open claims that could be closed or reserved amounts that seem inflated. Sometimes a single open claim with an inflated reserve is driving your e-mod higher than it should be. Your agent can work with the carrier's claims department to get reserves adjusted to realistic levels.

FAQ

Do I legally need workers' comp insurance in Texas? Texas doesn't mandate it for private employers, but going without exposes you to unlimited liability in employee injury lawsuits. Most general contractors require it from subs anyway.

What's the minimum GL coverage required for a Texas electrical license? TDLR requires at least $300,000 in general liability coverage for master electricians. Commercial project contracts typically require $1 million per occurrence minimum.

How does my experience modifier affect my premium? Your e-mod compares your actual losses to expected losses for your classification. An e-mod of 1.2 means you're paying 20% more than baseline; 0.8 means you're paying 20% less.

Can I use a personal auto policy for my work truck? No. Personal auto policies exclude commercial use. If you're in an accident while driving to a job site, your personal policy will likely deny the claim.

Does general liability cover design errors? It does not. Design-build electrical contractors need a separate professional liability (E&O) policy to cover claims arising from design or engineering errors.

What This Means for Your Business

Getting your insurance right as a Texas electrical contractor comes down to three things: meeting TDLR requirements, matching your coverage to your actual risk exposures, and presenting your business in a way that carriers want to write. Cutting corners on any of these creates problems that cost far more than the premium savings.

If you're unsure whether your current coverage matches your risk profile, or you're tired of getting declined by carriers that don't understand electrical work, reach out to Joule Pro. Our team works exclusively with licensed electrical contractors and places coverage through specialty markets built for this trade. A quick conversation with a licensed producer can identify gaps you didn't know existed and potentially save you money on premiums you're overpaying.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.