Business Insurance

Virginia Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

Running an electrical contracting business in Virginia means juggling licensing boards, bonding requirements, and a patchwork of insurance obligations that can vary wildly depending on whether you're wiring a single-family home in Henrico County or pulling cable for a data center in Loudoun. Getting an electrician insurance quote in Virginia isn't just about finding the cheapest premium: it's about understanding what the Commonwealth demands, what your contracts require, and which carriers actually want to write your type of work. Most electricians I've worked with don't realize how much money they leave on the table by not understanding these details before they start shopping. The right coverage stack, paired with a carrier that has genuine appetite for electrical risks, can save you thousands annually while keeping your license intact and your business protected. This guide breaks down what Virginia electricians actually need to know about coverage, licensing, bonds, and how carriers evaluate your operation.

Essential Insurance Coverages for Virginia Electricians

General Liability and Property Damage Protection

General liability is the foundation of every electrician's insurance program, and in Virginia, it's non-negotiable for licensure. This policy covers third-party bodily injury and property damage claims: think a homeowner tripping over your extension cord, or an accidental fire sparked during a panel upgrade. Most Virginia contracts require a minimum of $1 million per occurrence and $2 million aggregate, though commercial GCs often push for higher limits.

What catches many electricians off guard is the completed operations exposure. If a junction box you installed two years ago causes a fire, your GL policy's products-completed operations coverage is what responds. This is a huge deal in electrical work because defects can stay hidden for years. Make sure your policy doesn't sunset this coverage prematurely.

One common mistake: assuming your GL policy covers faulty workmanship itself. It doesn't. GL covers the resulting damage to other property, not the cost to redo your own work. That distinction matters when you're negotiating with an adjuster after a claim.

Workers' Compensation Requirements in the Commonwealth

Virginia requires workers' compensation insurance for any employer with two or more employees, including part-time and seasonal workers. Sole proprietors and partners can exempt themselves, but subcontractors without their own coverage often get added to your payroll by auditors, which inflates your premium.

Here's some good news for 2026: workers' compensation costs in Virginia are projected to decrease by 7.7% in the voluntary market effective April 1, 2026. That rate reduction reflects improved loss experience across the state, and electricians stand to benefit directly.

Electrical work carries a higher class code rating (NCCI code 5190 for wiring) than many other trades, so your comp premiums will naturally be higher than, say, a painting contractor. Safety training programs and a clean claims history are the fastest ways to bring those costs down. Programs like Joule Pro, built specifically for licensed electrical contractors, can connect you with carriers that understand the nuances of electrical class codes rather than lumping you in with general construction.

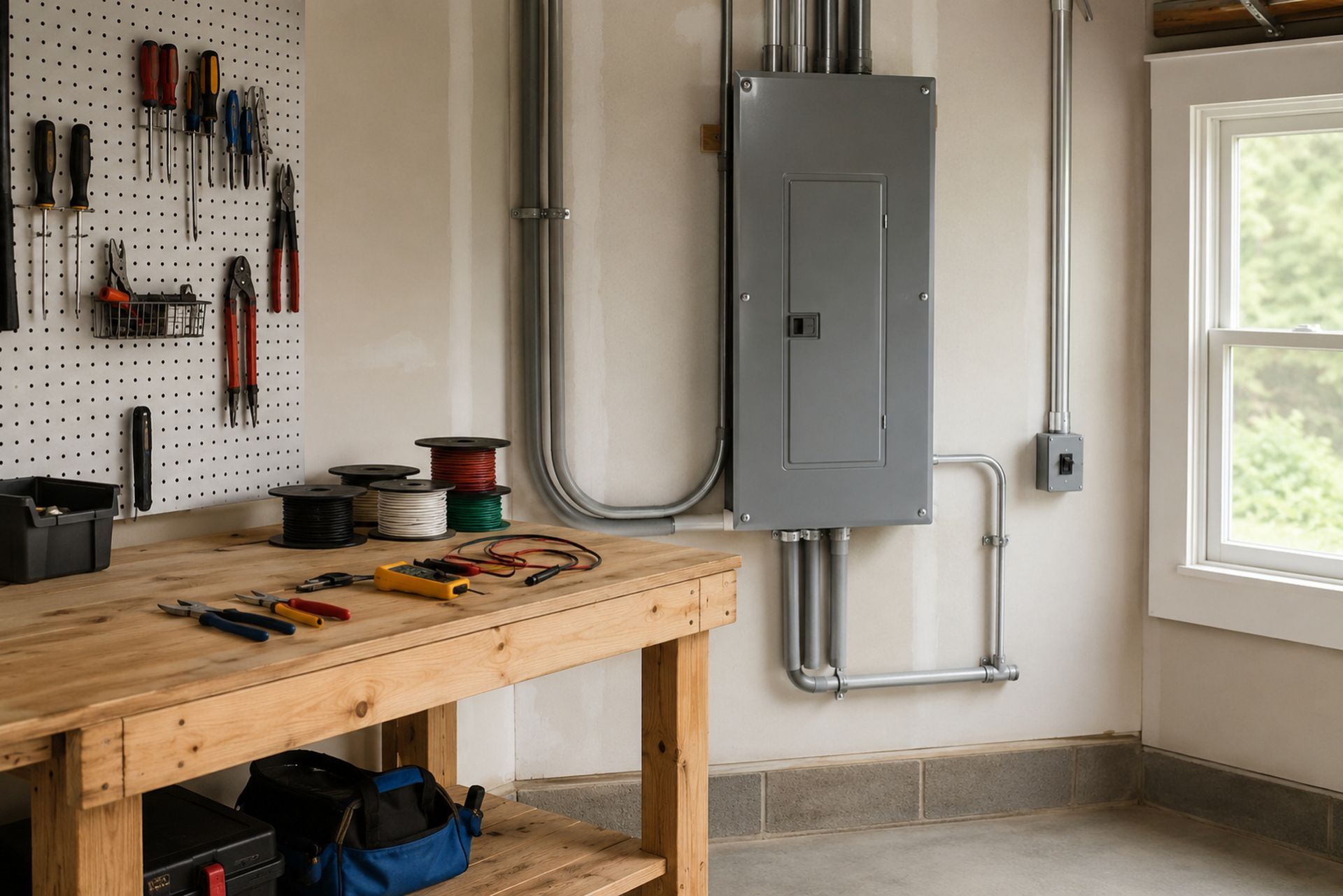

Commercial Auto and Inland Marine for Tools and Equipment

Your work trucks and vans need commercial auto coverage: personal auto policies won't cover vehicles used for business, period. Virginia requires minimum liability limits of $30,000/$60,000 for bodily injury and $20,000 for property damage, but most contractors carry at least $1 million in combined single-limit coverage to satisfy contract requirements.

Inland marine insurance is the policy that protects your tools, equipment, and materials in transit or stored at job sites. A standard commercial property policy only covers items at your listed business location. If your $15,000 wire puller gets stolen from a job site in Norfolk, inland marine is what pays for it.

| Coverage Type | What It Covers | Typical Virginia Minimums | Recommended Limits |

|---|---|---|---|

| General Liability | Third-party injury, property damage | $1M/$2M | $1M/$2M or higher |

| Workers' Comp | Employee injuries on the job | Statutory (2+ employees) | Statutory + $500K/$500K/$500K EL |

| Commercial Auto | Business vehicle accidents | $30K/$60K/$20K state minimum | $1M CSL |

| Inland Marine | Tools, equipment, materials in transit | Not required by law | Replacement cost of your inventory |

By: Michael Fusco

President of Joule Pro

INDEX

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Virginia Licensing and DPOR Insurance Compliance

Class A, B, and C License Requirements

Virginia's Department of Professional and Occupational Regulation (DPOR) issues three classes of contractor licenses, and each has distinct insurance requirements. Class A licenses cover projects over $120,000, Class B covers $10,000 to $120,000, and Class C handles work between $1,000 and $10,000.

Class A contractors must carry at least $1 million in general liability insurance. Class B requires a minimum of $500,000, and Class C requires $100,000. All three classes require proof of coverage on file with DPOR, and your insurer must notify the board if your policy lapses or cancels. A lapse can trigger license suspension faster than you'd expect.

The electrical trade specialty (ELE) falls under these same tiers. If you're a master electrician running jobs over $120,000 in contract value, you need that Class A license and the insurance minimums that come with it. Many electricians start at Class C and scale up, which means your insurance program needs to grow with you.

The Role of Surety Bonds in Professional Licensing

Virginia requires surety bonds for Class A and Class B contractors. Class A needs a $50,000 bond, and Class B requires $25,000. These bonds protect the public if you fail to complete a contract or violate regulations: they're not insurance for you, they're a guarantee for your clients and the state.

Your bond premium is typically 1% to 3% of the bond amount, depending on your personal credit score and financial history. A $50,000 Class A bond might cost you $500 to $1,500 annually. If a claim is filed against your bond, the surety company pays out and then comes after you for reimbursement, so treat it seriously.

One thing to keep in mind: bonds and insurance serve different purposes. Your bond doesn't cover property damage or injuries. Your GL policy doesn't satisfy the bonding requirement. You need both.

Understanding Carrier Appetite for Electrical Risks

Residential vs. Commercial and Industrial Operations

Carrier appetite is a term that describes how eager (or reluctant) an insurance company is to write a particular type of risk. For Virginia electricians, this matters enormously because not every carrier wants your business.

Residential electrical contractors generally find the most carrier options. Rewiring homes, panel upgrades, outlet installations: these are well-understood risks with predictable claim patterns. Most standard market carriers will quote residential electrical work without much hesitation.

Commercial electricians face a tighter market. Office buildouts and retail tenant improvements are usually fine, but once you get into industrial plants, manufacturing facilities, or high-rise construction, the carrier pool shrinks. The higher the project values and the more complex the systems, the fewer carriers want to play. This is exactly where a specialty program like Joule Pro adds value: their underwriter relationships are built around electrical trade risks specifically, so they can access markets that a generalist agent simply can't.

High-Risk Services: Solar, Alarms, and High-Voltage Work

If your Virginia electrical business includes solar panel installation, fire alarm systems, or high-voltage work above 600V, expect a harder time finding coverage. These operations carry elevated risk profiles that make many standard carriers decline outright.

Solar installation adds roof exposure and product liability for panel performance. Alarm system work introduces monitoring liability and potential errors-and-omissions claims. High-voltage industrial work carries obvious severity risk: a single incident can generate a seven-figure claim.

The key is disclosing these operations accurately on your application. Underwriters will find out eventually, and a misrepresentation can void your policy entirely. Be upfront about what you do, and work with a producer who knows which carriers have appetite for these specialties.

Factors Influencing Your Electrician Insurance Quote

Claims History and Safety Training Programs

Your loss history is the single biggest factor in your premium. A clean five-year claims record can qualify you for preferred rates, while even one or two significant claims can push you into surplus lines or assigned risk territory.

Investing in documented safety programs pays off directly. OSHA 10 and OSHA 30 certifications for your crew, regular toolbox talks, and written safety manuals all signal to underwriters that you take risk management seriously. Some carriers offer premium credits of 5% to 15% for formal safety programs.

Experience modification rates (EMR) on your workers' comp policy tell a similar story. An EMR below 1.0 means you're performing better than average for your class code, and that translates to lower premiums across the board.

Payroll Size and Annual Gross Receipts

Workers' comp premiums are calculated directly from payroll, so accurate payroll reporting is critical. Overestimate and you overpay all year (though you'll get an audit refund). Underestimate and you'll face a painful audit bill.

General liability premiums for electricians are typically rated on gross receipts. A Virginia electrical contractor doing $2 million in annual revenue will pay significantly more than one doing $500,000, even if the work type is identical. As your business grows, your insurance costs scale with it: budget accordingly.

Subcontractor costs can sometimes be excluded from your gross receipts calculation if those subs carry their own insurance. Get certificates of insurance from every sub, every time. Your auditor will ask for them.

How to Secure the Best Rates and Policy Terms in Virginia

The best electrician insurance quotes in Virginia don't come from clicking the first online ad you see. They come from working with a producer who understands electrical contracting risks and has access to multiple carriers with real appetite for your work type.

Start by getting your documentation in order: current DPOR license, EMR worksheet, three to five years of loss runs, a list of your operations by percentage of revenue, and your most recent tax return or financial statement. The more complete your submission, the better your quotes will be.

Request quotes from at least three sources, but compare more than just price. Look at carrier AM Best ratings, policy form differences (occurrence vs. claims-made), deductible structures, and whether the carrier has a track record of fair claims handling in the electrical space. A policy that's $2,000 cheaper but excludes completed operations coverage is no bargain.

Working with a specialty program like Joule Pro, backed by Fusco Orsini & Associates Insurance Services (CA Lic. 0H16057), gives you direct access to a licensed producer who handles quotes, proposals, and binders personally rather than routing you through a generic online portal. That human expertise matters when your policy needs endorsements specific to electrical work.

Frequently Asked Questions

Does Virginia require electricians to carry general liability insurance? Yes. DPOR requires proof of GL coverage for all three contractor license classes, with minimums ranging from $100,000 (Class C) to $1 million (Class A).

Can I exempt myself from workers' comp as a sole proprietor? You can, but if you hire even one additional employee, you'll need coverage once your total headcount hits two. Uninsured subs may also be counted as your employees during audits.

How much does electrician insurance typically cost in Virginia? It varies widely. A small residential shop might pay $3,000 to $6,000 annually for a basic GL policy, while a larger commercial operation could pay $15,000 or more. Workers' comp, auto, and inland marine add to the total.

What happens if my insurance lapses? DPOR is notified by your carrier, and your license can be suspended. Reinstatement requires proof of new coverage and potentially additional fees.

Do I need separate coverage for solar installation work? Most standard GL policies either exclude or heavily restrict solar operations. You'll likely need a specific endorsement or a carrier with explicit appetite for solar electrical work.

Your Next Steps

Virginia's insurance and licensing requirements for electricians are specific, interconnected, and unforgiving if you get them wrong. The right coverage protects your license, your crew, and the business you've built. The wrong coverage, or worse, a gap you didn't know existed, can unravel everything after a single claim.

Get your paperwork together, understand what your license class demands, and talk to a producer who specializes in electrical contractor insurance. If you want a quote from a team that works exclusively with licensed electricians, reach out to Joule Pro and get a proposal tailored to your Virginia operations. Your business deserves more than a one-size-fits-all policy from someone who doesn't know a service panel from a subpanel.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.