Business Insurance

Richmond, VA Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

Underwriting Preferences for Residential vs. Industrial Projects

Richmond's electrical contracting market sits at a unique crossroads. The city blends centuries-old architecture with rapid commercial development, creating a demand for skilled electricians that shows no signs of slowing. But that mix of old and new also creates insurance challenges you won't find in most Virginia metros. Whether you're pulling wire through a 19th-century Fan District rowhouse or wiring up a new mixed-use building in Scott's Addition, the risks - and the coverage you need - look different here than anywhere else in the state. This guide to electrician insurance in Richmond, VA breaks down local permitting quirks, city-specific exposures, and which carriers actually want to write electrical risks in this market.

Navigating the Richmond Electrical Contracting Landscape

Richmond's construction economy has been on a tear. Between the ongoing development along the Riverfront and steady renovation activity in neighborhoods like Church Hill and Carytown, electrical contractors are busy. But busy also means exposed. The city's mix of federal, state, and local regulations creates a compliance environment that's more layered than what you'd find in surrounding counties like Henrico or Chesterfield. Understanding how licensing and insurance interlock here is the first step toward protecting your business.

The Intersection of Local Licensing and Insurance Requirements

Virginia requires electrical contractors to hold a valid license through the Department of Professional and Occupational Regulation (DPOR), and the City of Richmond adds its own registration requirements on top of that. You can't pull a permit without showing proof of both a valid state license and active insurance. The city's permitting office will ask for a Certificate of Insurance before issuing permits, and they're not casual about it. Your COI needs to list the City of Richmond as the certificate holder, and the coverage limits must meet or exceed what the specific project scope demands.

Most Richmond general contractors won't even consider subbing electrical work to a firm that can't produce a COI within 24 hours. If your insurance program isn't set up to issue certificates quickly, you're losing jobs. This is one area where working with a specialty program like Joule Pro pays off: because we focus exclusively on electrical contractors, our team can turn around COIs fast and ensure they meet Richmond's specific formatting requirements.

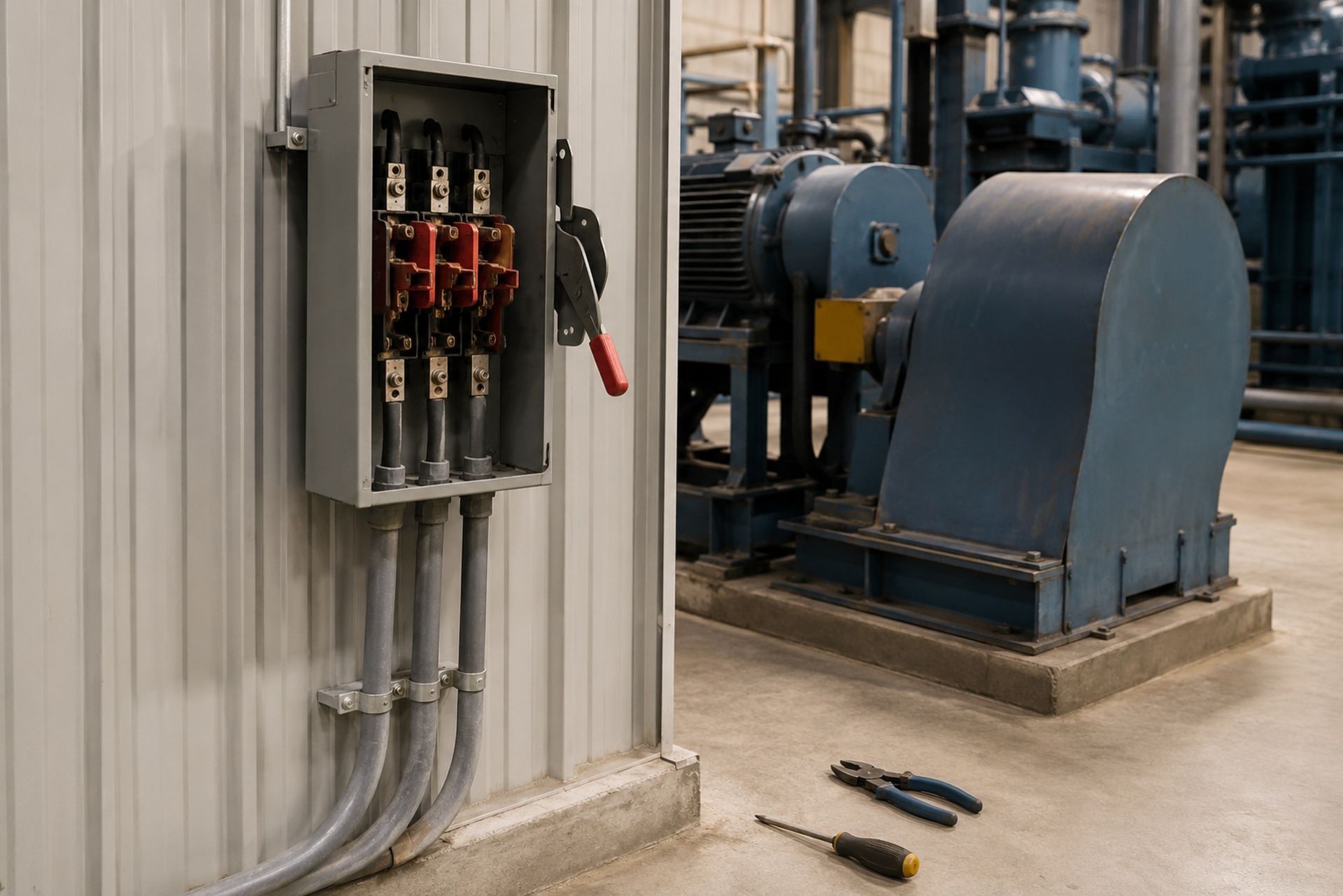

Richmond-Specific Risks: Historic Renovations and Urban Infrastructure

A huge portion of Richmond's housing stock predates modern electrical codes. Knob-and-tube wiring, aluminum branch circuits, and undersized panels are common finds in the Fan, Oregon Hill, and Jackson Ward. Working on these systems carries elevated risk: fire damage claims, property damage to irreplaceable plaster and woodwork, and even potential lead or asbestos exposure during demolition phases.

The city also has aging underground infrastructure. Electricians doing service upgrades or panel replacements in older neighborhoods sometimes encounter unexpected conditions: shared neutrals, deteriorated underground feeds, or utility conflicts that can lead to outages or property damage. These aren't hypothetical risks. They're the kinds of claims that Richmond electricians actually file, and they're exactly why your coverage needs to account for the specific work you're doing in this city.

By: Michael Fusco

President of Joule Pro

INDEX

Navigating the Richmond Electrical Contracting Landscape

Core Coverage Essentials for Richmond Electricians

Local Permitting and Compliance Obligations

Analyzing Carrier Appetite for Virginia Electrical Risks

Specialized Endorsements for Modern Electrical Work

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Core Coverage Essentials for Richmond Electricians

Getting the right coverage stack isn't about buying every policy available. It's about matching your coverage to the work you actually perform and the risks you actually face. Here's what most Richmond electrical contractors need as a baseline.

General Liability and Property Damage Protection

General liability is your foundation. It covers third-party bodily injury and property damage claims arising from your operations. In Richmond, the most common GL claims for electricians involve damage to existing structures during renovation work: cracked tile, scorched drywall, or water damage from accidentally hitting a pipe while running conduit. A standard GL policy with $1 million per occurrence and $2 million aggregate is the minimum most general contractors and property managers will accept.

One thing to keep in mind: completed operations coverage matters just as much as your premises/operations coverage. If a circuit you installed six months ago causes a fire, your completed operations coverage is what responds. Make sure your policy doesn't sunset this coverage too early.

Workers' Compensation for Virginia Contractors

Virginia law requires workers' compensation insurance for any employer with two or more employees. Even if you're a sole proprietor with one helper, you're legally required to carry it once that second person comes on. The Virginia Workers' Compensation Commission enforces this aggressively, and penalties for non-compliance include fines and potential criminal charges.

Electrical work carries a higher class code rating than many other trades, which means your premiums reflect the inherent danger of the work. Your experience modification rate (EMR) plays a big role here. A clean safety record can bring your EMR below 1.0 and save you thousands annually, while a couple of lost-time injuries can push it above 1.0 and make it harder to find willing carriers.

Tools and Equipment Floaters for Mobile RVA Crews

Your van full of meters, benders, drill kits, and wire isn't covered under your general liability policy. A tools and equipment floater (sometimes called an inland marine policy) protects your gear against theft, damage, and loss - whether it's on the job site, in your vehicle, or in your shop. Richmond has seen a rise in tool theft from vehicles, particularly in areas with active construction. A floater with a low deductible and agreed-value coverage is worth every dollar.

Local Permitting and Compliance Obligations

Richmond's permitting process is more structured than many surrounding jurisdictions, and the insurance documentation requirements are tightly woven into the system.

Bonding Requirements for City of Richmond Public Works

If you're bidding on City of Richmond public works projects - street lighting, traffic signal maintenance, municipal building upgrades - you'll need a performance bond and often a payment bond as well. Bond amounts typically match the contract value, and the surety company will underwrite your financials, credit, and insurance program before issuing the bond. Having a clean, well-structured insurance portfolio makes the bonding process smoother and can improve your bonding capacity.

Certificate of Insurance (COI) Standards for Residential and Commercial Permits

Richmond residential electrical permits carry a $63.00 base fee for the first $2,000 of work plus $6.07 per additional thousand, and every permit application requires proof of insurance. Commercial permits demand even more documentation, often including additional insured endorsements naming the property owner and general contractor.

The city's building inspectors have been known to verify insurance status during inspections, not just at the permit counter. If your policy lapses mid-project, you could face a stop-work order. Setting up automatic renewal reminders and keeping your agent in the loop on project timelines prevents this entirely.

Analyzing Carrier Appetite for Virginia Electrical Risks

Not every insurance company wants to write electricians. The trade carries higher loss frequency than, say, painting or landscaping, and carriers that don't understand electrical work tend to either decline the risk or price it punitively.

Preferred Carriers for New Construction vs. Service Work

Carrier appetite splits along the type of work you perform. New construction electricians working on ground-up residential or commercial projects generally find broader carrier options, because the risks are more predictable. Service and repair work - especially in older buildings - narrows the field. Carriers worry about completed operations exposure and the unpredictability of working with existing, potentially defective systems.

Specialty programs that focus on electrical contractors, like Joule Pro, maintain relationships with underwriters who specifically understand these distinctions. That means a service electrician working in Richmond's historic districts can get coverage that accurately reflects their risk, rather than being lumped into a generic contractor classification.

Factors Influencing Premiums in the Greater Richmond Area

Several factors drive your premium in the Richmond market:

- Claims history: Even one large claim can increase premiums 20-40% at renewal

- Revenue and payroll: Higher volume means higher exposure and higher premiums

- Subcontractor use: Using uninsured subs is a red flag for underwriters

- Type of work: Residential service vs. commercial new construction vs. industrial

- Safety programs: Documented safety training can earn premium credits

| Factor | Lower Premium Impact | Higher Premium Impact |

|---|---|---|

| Claims history | Zero claims in 3+ years | Multiple open claims |

| Work type | New residential construction | Industrial/high-voltage service |

| EMR | Below 0.85 | Above 1.2 |

| Subcontractor management | All subs insured, COIs on file | Uninsured or unverified subs |

| Safety program | Written program with training logs | No formal program |

Specialized Endorsements for Modern Electrical Work

Standard policies cover standard risks. But electrical work in 2026 increasingly involves specialized exposures that require endorsements or separate policies.

Professional Liability for Design-Build Projects

More Richmond electricians are taking on design-build roles, especially for EV charging installations, solar tie-ins, and smart building systems. If you're designing electrical systems - not just installing them - your general liability policy won't cover design errors. A professional liability (errors and omissions) endorsement protects you if a design flaw leads to system failure, code violations, or property damage. This coverage is becoming essential as the line between installer and designer continues to blur.

Pollution and Mold Coverage for Existing Structures

Working in older Richmond buildings means potential exposure to environmental hazards. If your work disturbs asbestos-containing materials or causes a water intrusion that leads to mold growth, standard GL policies typically exclude these claims. A contractor's pollution liability endorsement fills this gap. Given Richmond's climate - humid summers that accelerate mold growth - this isn't optional for electricians doing renovation work in pre-1980 structures.

Strategic Steps to Secure Comprehensive Local Coverage

The right insurance program for a Richmond electrician isn't something you piece together from random online quotes. It requires understanding how your specific work, location, and growth plans intersect with available coverage options.

Start by documenting your actual scope of work in detail. Are you pulling permits in the city proper, or also working in Henrico and Chesterfield? Do you do any high-voltage or industrial work? Are you subbing work out? These details shape your coverage needs and determine which carriers will compete for your business. Joule Pro, backed by Fusco Orsini & Associates Insurance Services, specializes in building coverage programs for exactly this kind of contractor - and because every quote is handled by a licensed professional, you get real answers instead of algorithmic guesses.

Get your insurance reviewed annually, not just at renewal. Your risk profile changes as you take on new project types or hire additional crews. A mid-year check-in can catch gaps before they become claims.

Frequently Asked Questions

Do I need separate insurance for Richmond city work versus Henrico County work? No, but your COI requirements differ. Richmond has stricter documentation standards, so make sure your agent knows you're pulling permits in the city.

How much does general liability cost for a Richmond electrician? Expect $2,500 to $6,000 annually for a small crew doing residential and light commercial work. Pricing varies based on revenue, claims history, and work type.

Can I add my apprentice to my workers' comp policy? Yes, and you should. Virginia requires coverage once you have two or more employees, including apprentices and part-time helpers.

What happens if my insurance lapses while I have an open permit? The city can issue a stop-work order, and your permit may be revoked. Reinstatement requires new proof of insurance and potentially a new permit application.

Does my general liability cover damage to a customer's existing wiring? Typically yes, as long as the damage results from your operations. Damage to your own work product is usually excluded - that's a workmanship issue, not an insurance issue.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.