Business Insurance

General Liability Insurance For Electricians in Idaho

★★★★★ 150+ Five-Star Reviews · Google & Facebook

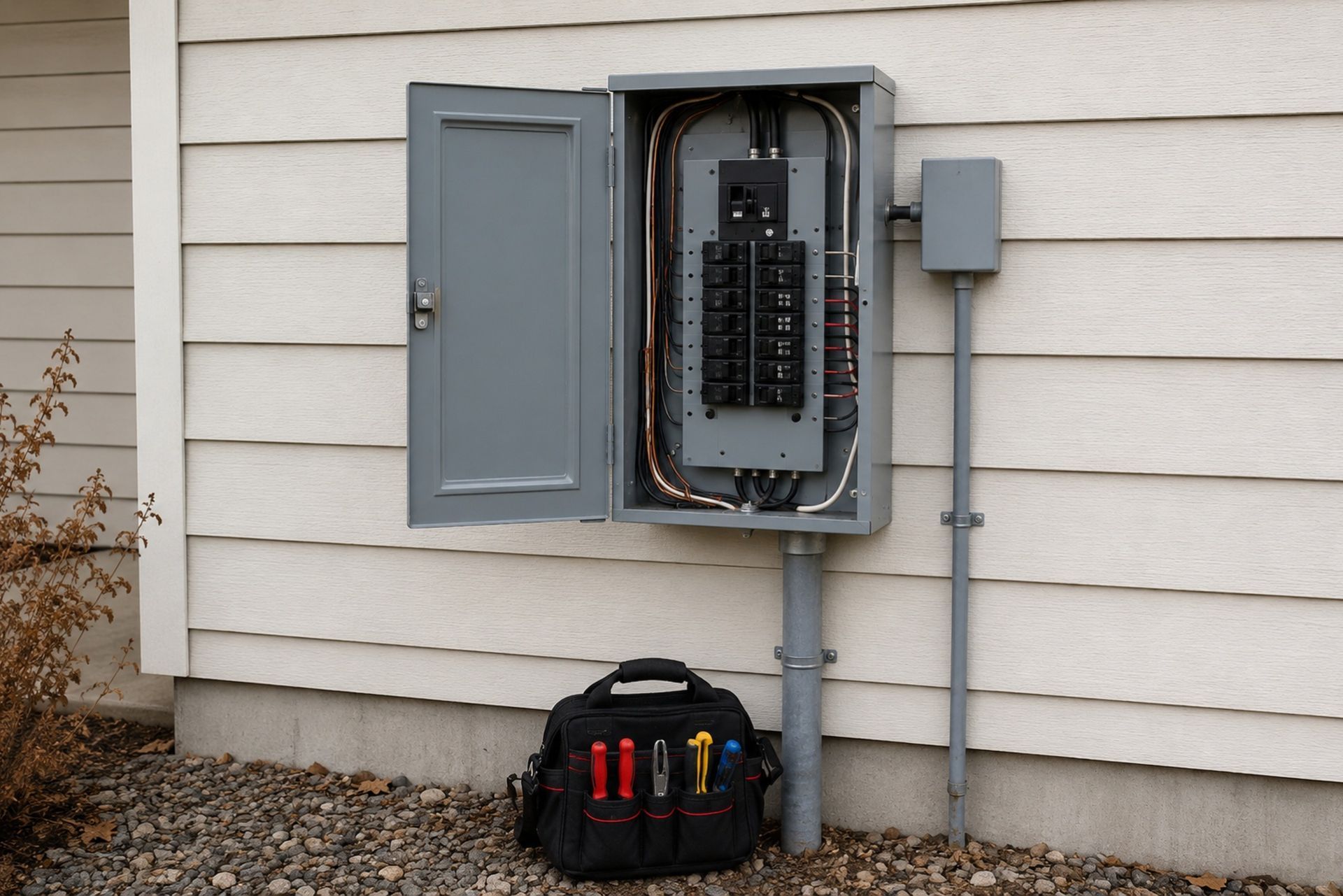

Running an electrical contracting business in Idaho means dealing with risks that most other trades don't face: arc flash incidents, fire damage from faulty wiring, property destruction during panel upgrades. A single claim from a residential customer or general contractor can wipe out years of profit if you're not properly insured. General liability insurance is the foundation of any Idaho electrician's risk management program, but the details matter far more than most contractors realize. Coverage limits, state-mandated minimums, and which carriers actually want to write electrical risks all play into what you'll pay and how well you're protected. This guide breaks down what Idaho electricians specifically need to know about liability coverage, from DOPL licensing requirements to carrier appetite and premium factors that hit your bottom line.

Idaho State Licensing and Insurance Requirements for Electricians

Division of Occupational and Professional Licenses (DOPL) Standards

Idaho's Division of Occupational and Professional Licenses governs electrical contractor licensing, and they don't mess around with insurance verification. Before DOPL will issue or renew your electrical contractor license, you need to show proof of general liability insurance meeting their minimum threshold. This isn't optional or negotiable: no valid insurance certificate, no license.

DOPL requires a minimum of $300,000 in general liability coverage for electrical contractors. That's the floor, not a recommendation. The division cross-references your insurance status, and if your policy lapses or gets cancelled, DOPL can suspend your license until you reinstate coverage. Idaho treats this seriously because electrical work carries inherent fire and electrocution risks that affect public safety.

Your insurance carrier must be admitted in Idaho or otherwise authorized to write coverage in the state. Certificates of insurance need to list DOPL as a certificate holder so they receive cancellation notices directly. This means your carrier will notify the state if your policy drops, which triggers a licensing issue fast.

Mandatory Liability Limits for Journeymen and Master Electricians

The $300,000 DOPL minimum applies to the contracting entity, not individual journeymen or master electricians working as employees. If you're a sole proprietor master electrician pulling permits under your own license, you carry the insurance obligation personally. Journeymen working under someone else's contractor license are typically covered by their employer's policy.

Here's the practical problem: $300,000 in coverage is dangerously low for most electrical work. A single house fire caused by alleged faulty wiring can generate claims well into six figures for property damage alone, before you even factor in bodily injury. Most general contractors and commercial property owners require $1,000,000 per occurrence as a minimum to get on their approved subcontractor list. Meeting DOPL's minimum keeps your license active, but it won't get you on most job sites.

By: Michael Fusco

President of Joule Pro

INDEX

Idaho State Licensing and Insurance Requirements for Electricians

Core Coverage Components of General Liability Insurance

Determining Optimal Coverage Limits for Idaho Contractors

Understanding Carrier Appetite for Electrical Risks

Factors Influencing Insurance Premiums in the Idaho Market

Best Practices for Managing Your Electrical Insurance Program

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Core Coverage Components of General Liability Insurance

Bodily Injury and Property Damage Protection

General liability insurance for electricians covers two primary exposure categories: bodily injury and property damage caused by your operations. If a homeowner trips over your tool bag and breaks a wrist, that's bodily injury. If you accidentally drill through a water line while running conduit, the resulting water damage is property damage.

For electricians specifically, the property damage exposure tends to be the bigger concern. Electrical fires, damaged drywall from rough-in work, and short circuits that fry expensive electronics are all common claim scenarios. Your GL policy responds to these third-party claims, covering defense costs and settlements up to your policy limits. Defense costs are typically covered outside the aggregate limit, which is a detail worth confirming with your carrier.

Products and Completed Operations for Electrical Work

This is where electrical contractors face unique risk compared to other trades. Products and completed operations coverage protects you after you've finished a job and left the site. If a panel you installed six months ago causes a fire, this coverage responds.

Electrical work has a long tail of liability exposure. Wiring defects might not manifest for months or years. Idaho's statute of limitations for property damage claims gives plaintiffs time to file, meaning a job you completed in 2024 could still generate a claim in 2026 or beyond. Your GL policy's completed operations coverage is arguably more critical than your premises/operations coverage, yet many electricians don't fully understand what triggers it. Programs like Joule Pro, built specifically for licensed electrical contractors, structure completed operations coverage to match the actual risk profile of electrical trade work rather than using generic contractor forms.

Determining Optimal Coverage Limits for Idaho Contractors

The Difference Between $1M/$2M and $2M/$4M Policies

Most Idaho electricians carry either a $1,000,000 per occurrence / $2,000,000 aggregate policy or a $2,000,000 per occurrence / $4,000,000 aggregate policy. Here's a quick comparison:

| Feature | $1M/$2M Policy | $2M/$4M Policy |

|---|---|---|

| Per Occurrence Limit | $1,000,000 | $2,000,000 |

| General Aggregate | $2,000,000 | $4,000,000 |

| Typical Premium Increase | Baseline | 15-30% more |

| GC/Commercial Requirements | Meets most residential GC needs | Required for many commercial projects |

| Fire Damage Sublimit | Usually $100,000 | Often $300,000+ |

The $1M/$2M policy satisfies most residential and light commercial contract requirements. But if you're bidding on commercial tenant improvement work, hospital projects, or government contracts, you'll likely need $2M/$4M limits or higher. The premium difference is usually modest relative to the additional protection.

When to Consider Commercial Umbrella or Excess Liability

An umbrella policy sits on top of your GL (and often your auto and workers comp) to provide additional limits. For Idaho electricians doing mixed residential and commercial work, a $1M umbrella over a $1M/$2M GL policy is often more cost-effective than jumping straight to a $2M/$4M primary policy.

Umbrella policies typically cost between $800 and $2,500 annually for small electrical contractors, depending on revenue and risk profile. They're especially valuable if you work on projects where contract requirements specify $5M or more in total liability coverage. One thing to keep in mind: umbrella carriers want to see clean claims history, so maintaining a strong safety record directly affects your ability to get this coverage at reasonable rates.

Understanding Carrier Appetite for Electrical Risks

Preferred Risks: Residential vs. Commercial Service Work

Not every insurance carrier wants to write electrical contractors. Carrier appetite refers to the types of risks an insurer actively seeks versus those they avoid or price aggressively. For Idaho electricians, understanding appetite saves you time and money during the quoting process.

Carriers generally prefer residential service electricians doing panel upgrades, rewiring, and new construction rough-in. Small commercial service work like office build-outs and retail tenant improvements also falls into the "preferred" category. These operations have predictable claim frequency and severity, which makes underwriters comfortable. An electrician doing $500,000 in annual revenue on residential service calls with no claims history is exactly what most standard market carriers want to see.

Specialty programs like Joule Pro maintain relationships with underwriters who specifically understand electrical trade risks, which means faster quotes and better terms than going through a generalist agent who writes one electrician policy a year.

High-Hazard Exclusions: Industrial and High-Voltage Projects

If your work involves high-voltage systems (above 600V), industrial process controls, or utility-scale solar installations, your carrier options narrow significantly. Many standard GL carriers exclude or sublimit coverage for work on systems above certain voltage thresholds. Power plant work, substation construction, and medium-voltage distribution projects fall into the "hard-to-place" category.

Idaho's growing data center market around Boise has increased demand for electricians doing high-voltage commercial work, but finding carriers willing to cover this exposure requires specialty market access. Industrial electricians should expect higher premiums, more restrictive policy terms, and longer underwriting timelines. Getting declined by two or three carriers before finding the right fit is normal for these risk profiles.

Factors Influencing Insurance Premiums in the Idaho Market

Payroll, Revenue, and Subcontractor Exposure

Your GL premium is calculated using a rate applied to your revenue or payroll, depending on the carrier's rating methodology. Most electrical contractor GL policies use gross revenue as the primary rating basis. An Idaho electrician generating $750,000 in annual revenue will pay meaningfully more than one generating $250,000, all else being equal.

Subcontractor usage also affects your premium. If you sub out work, carriers want to see certificates of insurance from every sub. Uninsured subcontractor costs often get added to your payroll or revenue base for rating purposes, inflating your premium. Keeping clean sub records and requiring COIs before anyone steps on your job site protects your insurance costs and your license.

Claims History and Safety Certification Impacts

Your loss history over the past three to five years is the single biggest factor in what you'll pay beyond your revenue size. One or two small claims might not move the needle much, but a six-figure fire claim will follow you for years. Carriers pull your loss runs during underwriting, and poor claims experience can push you out of standard markets entirely.

On the positive side, safety certifications and formal training programs can earn premium credits. OSHA 10 or OSHA 30 certifications for your crew, documented safety meetings, and arc flash training all signal to underwriters that you're a better risk. Some carriers offer 5-10% credits for verified safety programs, which adds up over time.

Best Practices for Managing Your Electrical Insurance Program

Treat your insurance program like any other business system: review it annually, not just when renewal notices arrive. Start by auditing your certificates of insurance at least quarterly to make sure your coverage matches your current operations. If you added commercial work or started a new service line, your policy needs to reflect that.

Keep your loss runs organized and request them from your carrier every six months. Knowing your claims history before your broker does puts you in a stronger negotiating position at renewal. Build relationships with brokers or programs that specialize in electrical contractor insurance: Joule Pro, for example, offers direct producer access so you're working with a licensed professional who understands the specific risks of your trade, not a chatbot or generic call center.

Track your subcontractor certificates religiously. Require updated COIs before every project, not just once a year. And budget for insurance as a real cost of doing business: Idaho electricians should expect to spend roughly 1.5-3% of gross revenue on their GL premium, depending on their risk profile and claims history.

Frequently Asked Questions

Does Idaho require electricians to carry general liability insurance? Yes. DOPL requires a minimum of $300,000 in general liability coverage to obtain or renew an electrical contractor license.

What GL limits do most Idaho general contractors require from electrical subs? Most GCs require $1,000,000 per occurrence and $2,000,000 aggregate as a minimum. Commercial and government projects often require higher limits.

How much does general liability insurance cost for an Idaho electrician? Premiums vary widely, but a small residential electrical contractor can expect to pay roughly $1,500 to $4,500 annually for a $1M/$2M policy, depending on revenue and claims history.

Will my GL policy cover work I completed last year? Yes, if your policy includes products and completed operations coverage, which is standard on most GL forms. The coverage applies to claims arising from work you've already finished.

What happens if my insurance lapses in Idaho? DOPL receives notification from your carrier and can suspend your electrical contractor license until you provide proof of reinstated coverage.

Your Next Steps

Getting the right liability coverage in Idaho isn't just about meeting DOPL's $300,000 minimum: it's about protecting your business from the real-world claims that electrical contractors face. Match your limits to your actual contract requirements, understand which carriers have appetite for your specific type of work, and keep your safety record clean to maintain competitive premiums. If you're unsure whether your current policy fits your operations, reach out to a specialty program like Joule Pro that works exclusively with licensed electrical contractors. A 15-minute conversation with someone who understands electrical trade risks can save you thousands in misplaced coverage or, worse, a denied claim.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.