Business Insurance

New Electrical Business Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

A single electrical fire claim can wipe out a new contracting business before it ever gains traction. One misrouted wire, one apprentice injury, one stolen van full of tools: these aren't hypothetical scenarios. They're Tuesday for electrical contractors who skipped the right insurance coverage. Whether you're pulling your first permit as a sole proprietor or scaling a crew of fifteen, understanding the full coverage stack for an electrical business is what separates contractors who survive from those who fold. The stakes are high because the risks are trade-specific: arc flash injuries, property damage from faulty wiring, and expensive diagnostic equipment that walks off job sites. This guide breaks down every major policy type you need, how your business structure changes the equation, and what to prioritize at each growth stage so you're never caught paying out of pocket for something a $50/month policy would have covered.

Foundational Liability and Workers' Compensation Requirements

General Liability for Electrical Accidents and Property Damage

General liability (GL) is your first line of defense and, in most states, the minimum insurance you'll need before a general contractor will even let you on site. A standard $1M/$2M GL policy for electricians averages around $379 per month nationally, though your actual rate depends heavily on your state, claims history, and the type of work you perform.

GL covers third-party bodily injury and property damage. Think: a homeowner trips over your cable run, or your work causes a short that damages a client's server room. It also covers completed operations, meaning if wiring you installed six months ago causes a fire, GL responds to that claim.

Here's where electrical contractors face unique exposure. Unlike a painter or landscaper, your work interacts with a building's core systems. A wiring error can cause catastrophic property damage or serious injury well after you've left the job. That's why many commercial clients and GCs require you to carry at least $1M per occurrence and $2M aggregate before signing a subcontract.

Workers' Compensation for On-the-Job Injuries

If you have employees, workers' comp isn't optional: nearly every state mandates it. Even in Texas, where it's technically elective, going without it exposes you to direct lawsuits from injured workers with no cap on damages.

Electrical work ranks among the higher-risk trades for workers' comp classification. Your premiums are calculated using NCCI class codes specific to electrical work, and rates vary dramatically by state. California and New York tend to be the most expensive, while states like Indiana and Virginia run significantly lower.

Workers' comp covers medical bills, lost wages, and rehabilitation for employees injured on the job. For electrical contractors, common claims include electrical burns, falls from ladders, and repetitive strain injuries. One serious injury without coverage can easily generate a six-figure liability.

Professional Liability and Errors & Omissions

This is the policy most new electrical contractors overlook. Professional liability, sometimes called errors and omissions (E&O), covers claims arising from your professional advice or design work. If you spec the wrong panel size for a commercial buildout, or your load calculations lead to a system failure, GL won't cover that: it's a professional services error, not property damage from your physical work.

E&O becomes especially important if you do any design-build work, energy audits, or EV charging station installations where engineering judgment is part of the deliverable.

By: Michael Fusco

President of Joule Pro

INDEX

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

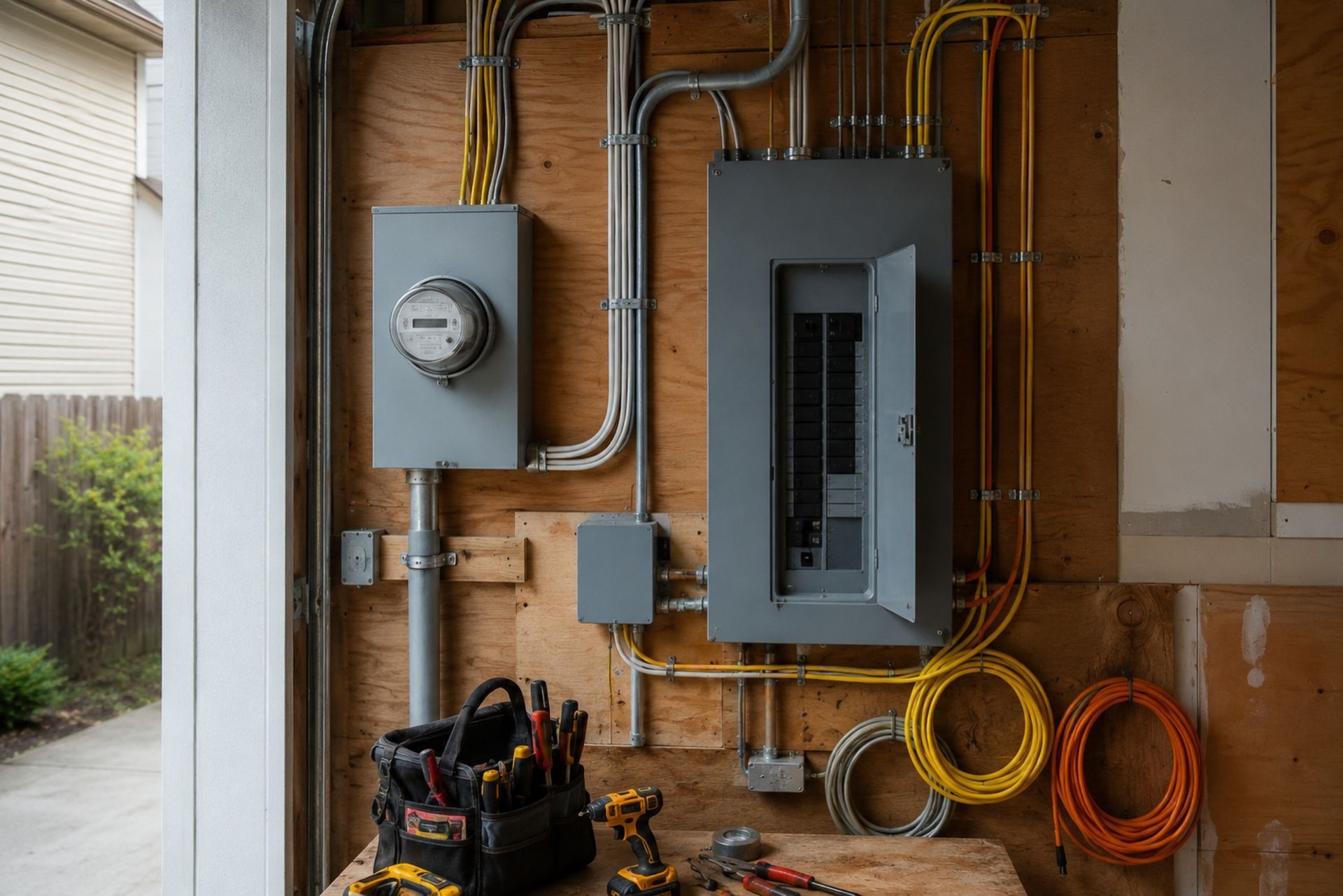

Protecting Physical Assets: Tools, Equipment, and Vehicles

Inland Marine Insurance for Tools and Mobile Equipment

Your tools travel with you. A standard commercial property policy only covers items at a fixed location, which means your $15,000 worth of meters, benders, and power tools riding in your van are unprotected without inland marine coverage.

Inland marine insurance covers tools and equipment in transit, at job sites, or stored in temporary locations. Policies can be written on a scheduled basis (listing specific high-value items) or as a blanket covering everything up to a set limit. For most electrical contractors starting out, a blanket policy between $10,000 and $50,000 covers the essentials without requiring an itemized inventory.

Theft from job sites and vehicle break-ins are the most common claims. Keep receipts and serial numbers for everything: it speeds up the claims process significantly.

Commercial Auto Insurance for Service Vans and Trucks

Your personal auto policy won't cover an accident that happens while you're driving to a job. Period. Commercial auto insurance is required for any vehicle used for business purposes, and it covers liability, collision, and comprehensive damage.

For electrical contractors running service vans, the policy should include hired and non-owned auto coverage if employees ever use personal vehicles for work errands. A single at-fault accident in an uninsured work vehicle can expose your entire business to a lawsuit. Programs like Joule Pro bundle commercial auto with other contractor-specific coverages, which often results in better rates than buying each policy separately from different carriers.

Commercial Property Insurance for Warehouses and Offices

If you lease or own a shop, warehouse, or office, commercial property insurance protects the building contents, inventory, and business income if a covered event like fire or storm damage shuts you down. Even a small 800-square-foot shop with a parts inventory, computers, and office furniture can represent $50,000+ in replacement value.

Business interruption coverage, often included or available as an add-on, replaces lost income during the downtime. For contractors who store significant material inventory, this policy is essential.

Coverage Considerations by Business Structure

Sole Proprietorships and Independent Contractors

As a sole proprietor, there's no legal separation between you and your business. Every claim, every lawsuit, every unpaid judgment hits your personal assets: your house, your savings, your truck. This makes adequate insurance coverage even more critical because insurance is essentially your only liability shield.

| Coverage Type | Sole Proprietor Priority | LLC/Corp Priority |

|---|---|---|

| General Liability | Essential (often required for licensing) | Essential |

| Workers' Comp | May be exempt if no employees (state-dependent) | Required with employees |

| Professional Liability | Recommended for design-build work | Recommended |

| Commercial Auto | Essential if using vehicle for work | Essential |

| Inland Marine | Highly recommended | Highly recommended |

Many states exempt sole proprietors with no employees from workers' comp requirements, but some GCs still require you to carry it before they'll sub work to you. Check your state's specific rules: getting this wrong can cost you contracts or trigger fines.

LLCs and Corporations: Protecting Personal Assets

Forming an LLC or corporation creates a legal wall between your personal assets and business liabilities. But that wall has holes. Courts can "pierce the corporate veil" if you commingle funds, skip insurance, or operate recklessly. Insurance fills the gaps your business structure leaves open.

For LLCs and corporations, the coverage stack looks similar but the stakes shift. Your business entity can be sued directly, and adequate insurance protects the company's assets and keeps operations running. Officers and directors coverage may also become relevant as you add partners or investors.

Scaling Coverage Through Business Growth Stages

Startup Phase: Minimum Legal Requirements and Licensing

Most states require proof of GL insurance before issuing an electrical contractor's license. This is your non-negotiable starting point. A basic GL policy, commercial auto (if you have a work vehicle), and inland marine for your tools form the minimum viable coverage stack.

At this stage, a specialty program like Joule Pro can be particularly helpful because getting quotes as a brand-new contractor is notoriously difficult. Generalist agencies often don't have markets willing to write new electrical businesses, while specialty programs maintain underwriter relationships specifically designed for this situation.

Budget $3,000 to $6,000 annually for startup-phase insurance, depending on your state and coverage limits.

Growth Phase: Adding Employees and Fleet Management

Hiring your first employee triggers workers' comp requirements in most states and changes your risk profile overnight. You're now responsible for someone else's safety on job sites with live electrical systems.

This phase typically requires adding workers' comp, increasing GL limits, expanding commercial auto to cover multiple vehicles, and potentially adding an umbrella policy for extra protection. Fleet management becomes a real concern: tracking driver records, implementing vehicle use policies, and ensuring every truck is properly covered.

Your premiums will increase, but so will your revenue. The key is scaling coverage in step with your actual exposure rather than either over-insuring or leaving dangerous gaps.

Expansion Phase: Umbrella Policies and Cyber Liability

Once you're running multiple crews, bidding large commercial projects, or expanding into new service areas like solar or EV infrastructure, your exposure multiplies. An umbrella policy provides an extra layer of liability coverage (typically $1M to $5M) above your existing GL, auto, and workers' comp limits. For a mid-size electrical contractor, umbrella policies often cost between $1,200 and $3,000 annually: relatively cheap for the protection they provide.

Cyber liability has become relevant for contractors who store customer data, process payments digitally, or use connected building management systems. A data breach or ransomware attack can be just as devastating as a physical loss.

Risk Management and Premium Optimization Strategies

Bundling with Business Owner's Policies (BOP)

A Business Owner's Policy bundles GL, commercial property, and business interruption into a single package, usually at a 10-20% discount compared to buying each separately. For electrical contractors with a physical office or shop, a BOP simplifies administration and reduces cost.

Not every contractor qualifies: BOPs are typically designed for businesses under a certain revenue or employee threshold. But for startups and small shops, they're often the most cost-effective way to get broad coverage.

Safety Programs and Their Impact on Premiums

Insurers reward contractors who actively manage risk. Implementing a formal safety program can reduce workers' comp premiums through experience modification rate (EMR) improvements over time. An EMR below 1.0 signals to underwriters that your business is safer than average, which translates directly to lower premiums.

Practical steps that move the needle: regular toolbox talks, documented safety training, proper PPE enforcement, and incident reporting protocols. Some carriers offer premium credits of 5-15% for contractors with written safety programs and clean loss histories.

Frequently Asked Questions

How much does insurance cost for a new electrical contractor? Expect to spend $3,000 to $8,000 annually for a basic coverage stack including GL, commercial auto, and inland marine. Workers' comp adds significantly more depending on payroll and state rates.

Do I need workers' comp if I'm a one-person operation? It depends on your state. Many states exempt sole proprietors with no employees, but some GCs require a workers' comp certificate regardless. Check your state's labor department website for specifics.

Can I use my personal auto insurance for my work van? No. Personal auto policies exclude business use. If you're in an accident while driving to a job site, your personal insurer will likely deny the claim.

What's the difference between general liability and professional liability? GL covers physical damage and bodily injury caused by your work. Professional liability covers financial losses from your professional advice, designs, or specifications.

Does my insurance need to change when I hire employees? Yes. Hiring triggers workers' comp requirements and may require increased GL limits, additional insured endorsements, and expanded auto coverage.

Making the Right Choice for Your Electrical Business

Getting insurance right from the start saves you from painful surprises later. The contractors who struggle most are the ones who bought the cheapest policy they could find without understanding what it actually covered, then discovered the gaps during a claim.

Match your coverage to your actual risk exposure, not just the minimum your state requires. As your business grows, revisit your policies annually: what worked for a one-person startup won't protect a ten-person operation. Working with a specialty program like Joule Pro, which focuses exclusively on electrical contractors, means your coverage is built around the risks you actually face rather than a generic template designed for all trades. Reach out to a licensed producer who understands electrical contracting and can walk you through the specifics for your state, your structure, and your growth plans.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.