Business Insurance

Chandler, AZ Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

Running an electrical contracting business in Chandler means dealing with a unique mix of desert climate risks, rapid suburban growth, and municipal requirements that don't always mirror what you'd find in Phoenix or Tempe. The insurance you carry needs to reflect those realities, not just check a box for your ROC license. Too many electricians grab a generic policy from a generalist agent and discover the gaps only after a monsoon fries a panel they installed last summer or a worker collapses from heat exhaustion on a rooftop in July. This guide covers what Chandler electricians actually need: the right coverage components, local permitting nuances, city-specific hazards, and which carriers are writing policies for electrical contractors in the Phoenix metro area right now. Whether you're a one-truck residential shop or running commercial crews across Maricopa County, the details here should save you real money and real headaches.

Navigating the Chandler Electrical Landscape and Insurance Essentials

Chandler's growth trajectory hasn't slowed. The city continues attracting semiconductor manufacturing, data center construction, and large-scale residential developments, all of which create steady demand for licensed electricians. But that growth also means the city and state have specific compliance expectations that directly affect your insurance requirements.

Arizona Registrar of Contractors (ROC) Bond Requirements

Every licensed electrical contractor in Arizona must carry a contractor's license bond through the ROC. For residential contractors, the bond amount is $10,000; for commercial and dual-licensed contractors, it's $15,000. This bond isn't insurance: it protects consumers if you fail to perform contracted work or violate ROC statutes. But here's the catch: many carriers and project owners look at your bond status as a baseline credibility check. If your bond lapses, your license becomes inactive, and you can't legally pull permits in Chandler or anywhere else in Arizona.

A common mistake is confusing the ROC bond with general liability coverage. They serve entirely different purposes. The bond covers regulatory violations and consumer complaints. Your GL policy covers third-party bodily injury and property damage claims arising from your work.

Aligning General Liability with Chandler Business Licensing

Chandler requires a city business license for any contractor operating within city limits. While the city doesn't mandate a specific GL limit for the license itself, most general contractors and property managers in the area require $1 million per occurrence and $2 million aggregate before they'll let you on a jobsite. For commercial projects near the Price Road corridor or in the Chandler Airpark area, you'll often see $5 million umbrella requirements.

Matching your GL limits to the work you're actually bidding on matters more than carrying the bare minimum. If you're consistently losing bids because your certificate of insurance doesn't meet project requirements, your policy is costing you revenue, not just premiums.

By: Michael Fusco

President of Joule Pro

INDEX

Navigating the Chandler Electrical Landscape and Insurance Essentials

Core Coverage Components for Chandler Electricians

City-Specific Risks: Monsoon Season and Extreme Heat

Local Permitting and Inspection Compliance in Chandler

Carrier Appetite and Underwriting in the Phoenix Metro Area

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Core Coverage Components for Chandler Electricians

Getting the right stack of policies in place is where many contractors either overpay for coverage they don't need or leave dangerous gaps.

Workers' Compensation for High-Heat Environments

Arizona doesn't let employers opt out of workers' comp if they have even one employee. The good news: workers' compensation voluntary loss costs in Arizona saw a 6.7% reduction effective January 1, 2026, marking continued decreases that have brought rates down significantly over the past decade. For electricians working in Chandler's extreme summer heat, where rooftop and attic temperatures can exceed 150°F, heat-related illness claims are a real and recurring issue.

Your workers' comp policy should account for the physical demands of desert electrical work. Carriers that specialize in electrical trades, like those Joule Pro works with, understand that classification codes for electricians carry specific risk profiles tied to environment, not just task.

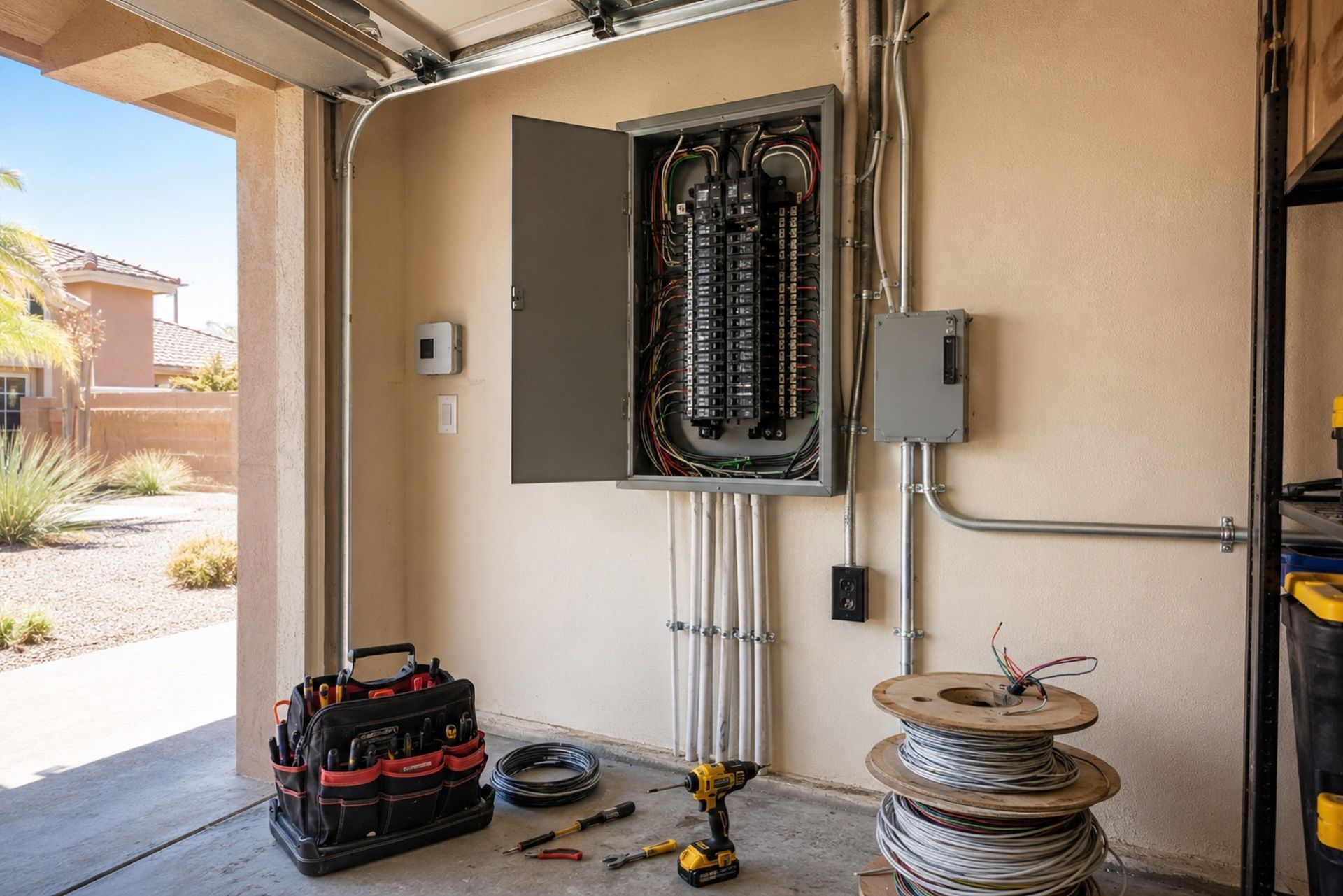

Inland Marine and Tool Coverage for Mobile Operations

Most electricians in Chandler operate from service vans or trucks loaded with $15,000 to $50,000 worth of tools, meters, wire, and diagnostic equipment. A standard commercial auto policy doesn't cover tools stolen from a vehicle or damaged in transit. That's where inland marine coverage fills the gap.

If your crew works across multiple Chandler jobsites daily, your tools spend most of their life in transit or on temporary locations. Inland marine policies are designed exactly for this: covering property that moves between locations rather than sitting in a fixed building.

Professional and Pollution Liability for Solar Installations

Chandler's solar adoption rate continues climbing, and electricians handling PV system design, installation, and grid interconnection face risks that standard GL policies often exclude. Professional liability (errors and omissions) covers claims arising from faulty system design or incorrect load calculations. Pollution liability covers scenarios like battery electrolyte leaks from energy storage systems.

If you're doing any solar work, ask your agent specifically whether your policy includes or excludes photovoltaic installation. Many standard electrical contractor policies treat solar as a separate class of risk.

City-Specific Risks: Monsoon Season and Extreme Heat

Chandler's climate creates insurance exposures that electricians in cooler, drier states simply don't face.

Managing Electrical Surge and Storm Damage Claims

Monsoon season runs from mid-June through September, and Chandler regularly sees dust storms, lightning strikes, and flash flooding. Lightning-induced power surges can damage electrical systems you've installed, and customers sometimes file claims against the installer rather than their homeowner's policy. Having a GL policy that clearly covers completed operations is critical here: it protects you against claims for work you finished weeks or months ago.

One pattern we see repeatedly: an electrician installs a panel or subpanel, a monsoon surge damages connected equipment, and the homeowner's insurance company subrogate against the electrician's policy. If your completed operations coverage has low sublimits or restrictive endorsements, you're exposed.

Mitigating Fire Risks in High-Density Residential Developments

Chandler's newer master-planned communities pack homes close together, and many feature wood-frame construction during the build phase. Electrical fires during rough-in or finish work can spread rapidly in these environments. The National Fire Protection Association tracks electrical distribution as a leading cause of home structure fires, and insurers pay close attention to contractors working in high-density residential zones.

Your GL policy's fire damage legal liability sublimit matters here. The standard $100,000 sublimit may be inadequate if a fire spreads to adjacent units. Talk to your agent about increasing this limit, especially if you're doing new construction in developments like those south of Ocotillo Road.

Local Permitting and Inspection Compliance in Chandler

Chandler's permitting process is more digitized than many Arizona municipalities, but the insurance documentation requirements remain strict.

Insurance Certificates for City of Chandler Projects

The City of Chandler requires certificates of insurance for permitted electrical work, and municipal projects typically demand the city be listed as an additional insured on your GL policy. The city's Development Services department handles permit applications and will verify your insurance status before issuing permits for commercial or multi-family projects.

Turnaround time on certificate requests matters. If your insurance provider takes three to five business days to issue a certificate, you could lose a project to a competitor who gets theirs same-day. Joule Pro's direct producer access means certificates, endorsements, and policy changes are handled by a licensed professional who understands the urgency of contractor timelines.

Liability Impacts of NEC Adoption and Local Amendments

Arizona adopts the National Electrical Code on a statewide basis, and Chandler follows the state-adopted version with limited local amendments. The 2023 NEC is currently enforced, with provisions for GFCI and AFCI protection that have expanded significantly. If you install work that meets code at the time of installation but a claim arises later, your policy's coverage trigger date and occurrence definition become critical.

Electricians who stay current on code changes reduce their claims exposure. Carriers view code-compliant contractors as lower risk, which directly affects your premium.

Carrier Appetite and Underwriting in the Phoenix Metro Area

Not every insurance carrier wants to write electrical contractor policies in Arizona. Understanding which carriers have appetite for your specific type of work saves you from wasting time on quotes that go nowhere.

Preferred Carriers for Residential vs. Commercial Contractors

| Factor | Residential Electricians | Commercial Electricians |

|---|---|---|

| Typical GL Premium Range | $2,500 - $6,000/year | $5,000 - $15,000+/year |

| Carrier Appetite | Broad: many admitted carriers | Narrower: specialty markets preferred |

| Common Exclusions | Solar, pool wiring | EIFS, high-rise work |

| Certificate Turnaround | 1-3 business days | Same-day often required |

| Umbrella Availability | Readily available | May require excess placement |

Residential electricians in Chandler generally find more carrier options because the risk profile is well-understood. Commercial contractors, especially those working on data centers or industrial facilities near the Intel campus, often need specialty markets. Joule Pro's underwriter relationships are built specifically for electrical contractors, which means access to markets that generalist agencies can't place.

Factors Influencing Premiums for Maricopa County Electricians

Your premium isn't just about revenue and payroll. Carriers in the Phoenix metro area weigh several Chandler-specific factors: your claims history over the past five years, the percentage of work that's new construction versus service and repair, whether you do any high-voltage or solar work, and your safety program documentation. Contractors with formal heat illness prevention plans often receive credits from carriers familiar with Arizona's climate risks.

Loss runs tell the story. If you've had two or more claims in three years, expect to pay 20-40% more than a clean contractor with identical revenue.

Optimizing Your Policy for Long-Term Business Growth

Getting the cheapest policy isn't a strategy: it's a gamble. The electricians who build sustainable businesses in Chandler treat their insurance program as a competitive advantage. A strong certificate of insurance opens doors to better projects. Clean loss runs earn you lower premiums year over year. Proper coverage limits mean a single claim doesn't bankrupt the business you've spent years building.

Review your policy annually, ideally 60-90 days before renewal. That gives your agent time to market your account to multiple carriers and negotiate better terms. If your current agent doesn't specialize in electrical contractor insurance, you're likely overpaying or underinsured, possibly both.

For Chandler electricians ready to get a coverage review from someone who actually understands the electrical trade, reach out to Joule Pro. Every quote is handled by a licensed insurance professional who knows the difference between a 200-amp residential service upgrade and a 480V commercial distribution project, and prices your policy accordingly.

FAQ

Do I need separate insurance for solar installation work in Chandler? Not always a separate policy, but your GL policy must explicitly include solar or photovoltaic work. Many standard electrical contractor policies exclude it, so verify with your agent before bidding solar jobs.

How much general liability coverage do most Chandler general contractors require? The standard requirement is $1 million per occurrence with a $2 million aggregate. Commercial projects and municipal work often require a $5 million umbrella on top of that.

Does my ROC bond replace general liability insurance? No. Your ROC bond protects consumers against license violations and failure to perform. General liability covers third-party injury and property damage claims. You need both.

Are heat-related worker injuries covered by workers' comp in Arizona? Yes. Heat exhaustion, heat stroke, and related conditions sustained on the job are covered under Arizona workers' compensation. Carriers expect you to have a documented heat illness prevention program.

How often should I review my electrician insurance policy? At least annually, and ideally 60-90 days before your renewal date. This gives enough time to shop the market and adjust coverage for any changes in your business operations.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.