Business Insurance

Oakland, CA Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

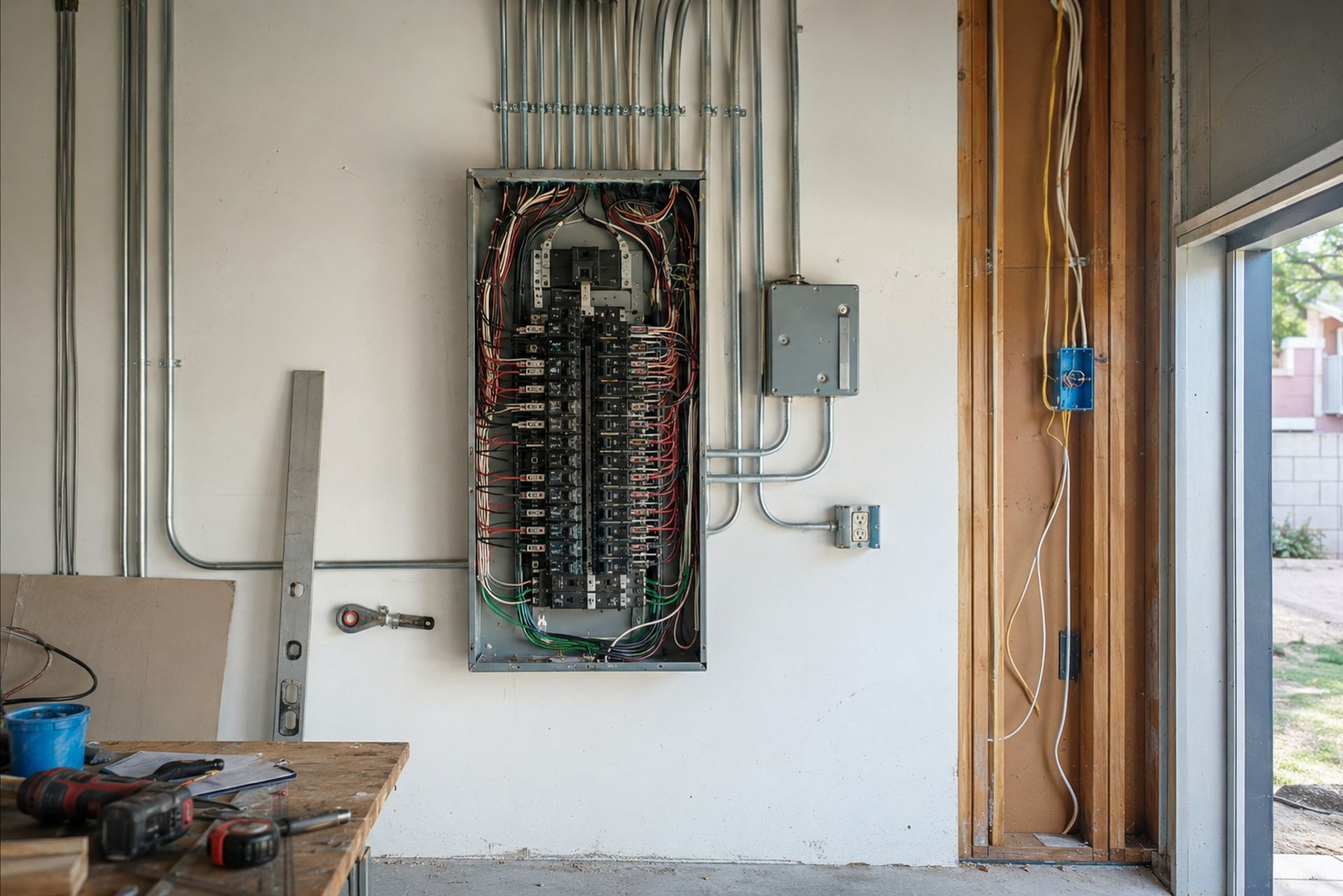

Oakland's mix of century-old Victorians, seismic retrofit mandates, and dense commercial corridors creates a unique risk profile that most generalist insurance agents simply don't understand. If you're a licensed electrician pulling permits in Alameda County, your insurance needs look nothing like those of an electrician working new construction in Fresno or residential service calls in San Diego. This guide covers the specific coverage requirements, city-specific risks, and carrier appetite factors that Oakland electrical contractors need to know in 2026 - from the permits the city demands to the endorsements that keep your business protected when things go sideways on a job site. Whether you're a solo C-10 holder or running a crew of fifteen across the East Bay, getting the right insurance stack isn't optional. It's the foundation your business runs on.

The Oakland Electrical Landscape: Insurance Requirements and City Compliance

Oakland's regulatory environment is tighter than many California cities, and the insurance requirements reflect that. Between the city's own permit mandates and the state's licensing standards, electricians working here face a layered compliance structure that can trip up even experienced contractors.

Oakland Planning and Building Department Permit Insurance Mandates

The Oakland Planning and Building Department requires contractors to carry valid insurance before pulling most electrical permits. For commercial and multi-family residential work, you'll typically need to show proof of general liability insurance with minimum limits of $1 million per occurrence and $2 million aggregate. Workers' compensation coverage is mandatory if you have even one employee, and the city will ask for certificates of insurance naming the property owner or general contractor as an additional insured on many projects.

One thing that catches contractors off guard: Oakland has been increasingly strict about insurance verification since updating its permitting processes. If your COI doesn't match what's on file, expect delays. The city also requires a valid Oakland business tax certificate, and your insurance documentation needs to align with the entity name on that certificate. Mismatches between your LLC name, your license, and your insurance policy are one of the most common reasons permits get held up.

California C-10 License Bond and State-Level Liability Standards

Beyond Oakland's local requirements, every C-10 electrical contractor in California must maintain a $25,000 contractor's license bond through the Contractors State License Board. This bond protects consumers, not you - it's a guarantee that you'll comply with state regulations and fulfill contractual obligations.

The CSLB also requires workers' compensation insurance or a valid exemption certificate if you're a sole proprietor with no employees. California doesn't mandate a specific general liability limit at the state level, but practically speaking, most general contractors and property managers in the Bay Area won't let you on site without at least $1 million/$2 million in GL coverage. Many larger commercial projects in Oakland now require $5 million umbrella policies as standard.

By: Michael Fusco

President of Joule Pro

INDEX

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Essential Insurance Policies for Oakland Electrical Contractors

General Liability for Property Damage and Third-Party Injuries

General liability is the backbone of your insurance program. It covers third-party bodily injury, property damage, and completed operations claims - the scenarios that can bankrupt a small electrical business overnight. Think: a homeowner trips over your cable run and breaks a wrist, or a faulty panel installation causes a fire six months after you finished the job.

In Oakland specifically, completed operations coverage matters more than many electricians realize. The city's aging housing stock means you're often tying new work into old systems, and the liability window extends well beyond the day you leave the job site. A typical GL policy for an Oakland electrician runs between $1,200 and $3,500 annually for a small operation, though rates vary significantly based on revenue, payroll, and claim history.

Workers' Compensation for Multi-Employee Bay Area Crews

Bay Area workers' comp rates for electrical contractors remain among the highest in the state. California's classification code 5190 (electrical wiring) carries a base rate that, combined with your experience modification factor, can make this your single largest insurance expense. For a crew of five electricians in Oakland, annual workers' comp premiums can easily exceed $25,000 to $40,000.

The key to managing this cost is your experience mod (or E-Mod). A clean safety record over three years can drop your modifier below 1.0, saving thousands annually. Conversely, even one serious claim can push your mod above 1.2 and make you nearly uninsurable with preferred carriers. Programs like Joule Pro, built specifically for electrical contractors, can help you find competitive workers' comp markets even with a less-than-perfect mod, because specialty underwriters understand the trade's risk profile better than generalist carriers.

Inland Marine and Tool Coverage for Urban Job Site Security

Tool theft is a real and persistent problem in Oakland. Roughly 89% of tradespeople report being victims of tool theft at some point in their career, and recovery rates for stolen equipment hover in the single digits. Oakland's urban density, combined with overnight street parking and multi-site operations, makes your tools and equipment especially vulnerable.

Inland marine insurance covers your tools, testing equipment, and materials both in transit and at job sites. A standard policy can cover $10,000 to $100,000 or more in equipment, with deductibles typically ranging from $250 to $1,000. If you're running wire pullers, meters, conduit benders, and diagnostic equipment across multiple Oakland job sites, this coverage pays for itself the first time something walks off a truck.

Mitigating Oakland-Specific Operational Risks

Navigating Seismic Retrofitting Risks in Older East Bay Structures

Oakland sits squarely in one of the most seismically active regions in the country. The Hayward Fault runs directly through the East Bay, and the city has mandatory seismic retrofit requirements for soft-story buildings. Electricians working on these retrofit projects face unique exposures: you're opening walls in buildings that may contain asbestos, knob-and-tube wiring, or other hazards that increase both your liability and your workers' health risks.

Pollution liability endorsements become relevant here. If your crew disturbs asbestos during an electrical upgrade in a 1920s apartment building, a standard GL policy won't cover the remediation costs. You need either a pollution liability endorsement or a separate environmental policy. This is one area where working with a specialty program like Joule Pro pays off - they understand which endorsements electrical contractors actually need versus the generic add-ons a generalist agent might recommend.

High-Density Residential and Commercial Multi-Tenant Liability

Oakland's multi-tenant buildings present a concentration of risk that single-family residential work doesn't. When you're wiring a 40-unit apartment building, a single mistake can affect dozens of tenants and trigger multiple claims simultaneously. Fire damage from an electrical fault in a dense residential building can generate claims in the millions.

Commercial work in downtown Oakland and the Jack London district carries similar concentration risks. Tenant improvement projects in mixed-use buildings often require higher liability limits, and property managers increasingly demand contractor-specific endorsements that address the unique exposures of electrical work in occupied spaces. Your policy needs to account for business interruption claims from tenants, not just direct property damage.

Carrier Appetite and Underwriting in the Oakland Market

Identifying Preferred Carriers for Northern California Artisans

Not every insurance carrier wants to write electrical contractors in Oakland. Wildfire risk in the surrounding hills, earthquake exposure, and the city's litigation environment make some carriers cautious about the entire East Bay market. The carriers with genuine appetite for Oakland electricians tend to be specialty markets that understand artisan contractor risk - companies that write hundreds or thousands of electrical policies nationally and can price the risk accurately.

| Factor | Preferred Carriers | Standard Market Carriers |

|---|---|---|

| Electrical trade experience | Deep understanding of C-10 risks | Generalist underwriting |

| Oakland appetite | Active in Bay Area market | May decline or surcharge |

| Included with competitive terms | Included with competitive terms | Often restricted or excluded |

| Premium range (small contractor) | $1,200 - $3,000/year GL | $2,500 - $5,000+/year GL |

| Endorsement flexibility | Trade-specific options available | Limited customization |

Working through a program that has established relationships with these specialty carriers - rather than shopping the open market yourself - typically results in better coverage terms and lower premiums.

Factors Influencing Premiums: Experience, Revenue, and Claim History

Your premium is driven by five primary factors: annual revenue, payroll, years in business, claim history, and the type of work you perform. An Oakland electrician doing $500,000 in annual revenue with residential service work will pay significantly less than one doing $2 million in commercial tenant improvements.

Claim history is the single biggest swing factor. One liability claim in the past three years can double your premium. Two claims can make you nearly unplaceable in the standard market. This is why proactive risk management - safety programs, documented procedures, photo documentation of completed work - isn't just good practice. It directly affects your bottom line every year at renewal.

Best Practices for Securing and Maintaining Coverage

Managing Certificates of Insurance (COIs) for General Contractors

If you subcontract under general contractors in Oakland, you're issuing COIs constantly. Every GC wants to be listed as an additional insured, and many require specific policy language or endorsements. The fastest way to lose a job is being unable to produce a compliant COI within 24 hours of a request.

Keep your insurance agent's contact information readily accessible, and make sure they understand the turnaround expectations in the Bay Area construction market. Joule Pro, for instance, provides direct producer access - meaning a licensed professional handles your COI requests rather than routing them through an automated system. That speed matters when a GC needs documentation before you can start on Monday morning.

Annual Policy Audits and Adjusting Coverage for Business Growth

Your insurance needs shift as your business grows. An annual policy audit ensures your coverage limits, payroll estimates, and revenue projections match reality. Underreporting payroll to save on workers' comp premiums is a common mistake that leads to painful audit adjustments at the end of the policy term - sometimes tens of thousands of dollars owed in a lump sum.

Review your tool and equipment schedule annually too. If you've added a $15,000 wire puller or upgraded your testing equipment, your inland marine policy needs to reflect those values. Undisclosed equipment isn't covered when it's stolen.

Your Next Steps

Getting the right insurance coverage for electrical work in Oakland means understanding both the city's specific requirements and the broader California regulatory framework. The combination of seismic risks, aging building stock, dense multi-tenant properties, and strict permitting creates an environment where generic insurance simply isn't enough.

Start by confirming your coverage meets Oakland's permit requirements. Then evaluate whether your current policies address completed operations, pollution liability, and adequate tool coverage. If you're unsure whether your carrier actually has appetite for Oakland electrical contractors, that's a red flag worth investigating.

Reach out to a specialty program that focuses exclusively on electrical contractors. The difference between a generalist agent and one who understands C-10 risks can mean thousands in premium savings and - more importantly - coverage that actually responds when you need it.

Frequently Asked Questions

How much does general liability insurance cost for an Oakland electrician? Most small electrical contractors in Oakland pay between $1,200 and $3,500 per year for GL coverage, depending on revenue, crew size, and claim history.

Do I need separate earthquake insurance for my electrical business? Standard GL policies cover damage you cause during work, but they don't cover earthquake damage to your own property or equipment. A commercial property policy with earthquake endorsement handles that.

Can I pull permits in Oakland without workers' comp if I'm a sole proprietor? California allows sole proprietors with no employees to file a workers' comp exemption with the CSLB. However, some GCs and property owners still require it before allowing you on site.

What happens if my insurance lapses while I have active permits in Oakland? The city can suspend your permits, and the CSLB can suspend your C-10 license. Reinstatement involves penalties, fees, and potential gaps in your coverage history that future carriers will flag.

Does my GL policy cover work I did six months ago if a fire starts? Yes, if your policy includes completed operations coverage - which most standard GL policies do. Check your declarations page to confirm it's not excluded.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.