Business Insurance

Independence, MO Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

Running an electrical contracting business in Independence, Missouri, means dealing with a unique mix of risks that contractors in other parts of the metro don't face. Between the city's aging housing stock, its own municipal utility system, and a permitting process that differs from Kansas City proper, your insurance needs aren't cookie-cutter. This guide breaks down the specific coverage electricians in Independence need, how local permitting and bonding requirements affect your policies, what environmental and historical risks to watch for, and which carriers are actually writing policies for electrical contractors in the Jackson County area right now. If you've been quoted a generic policy that doesn't account for the realities of working in Independence, you're probably either overpaying or underinsured - and neither is a good place to be.

Essential Insurance Policies for Independence Electricians

General Liability and Property Damage Protection

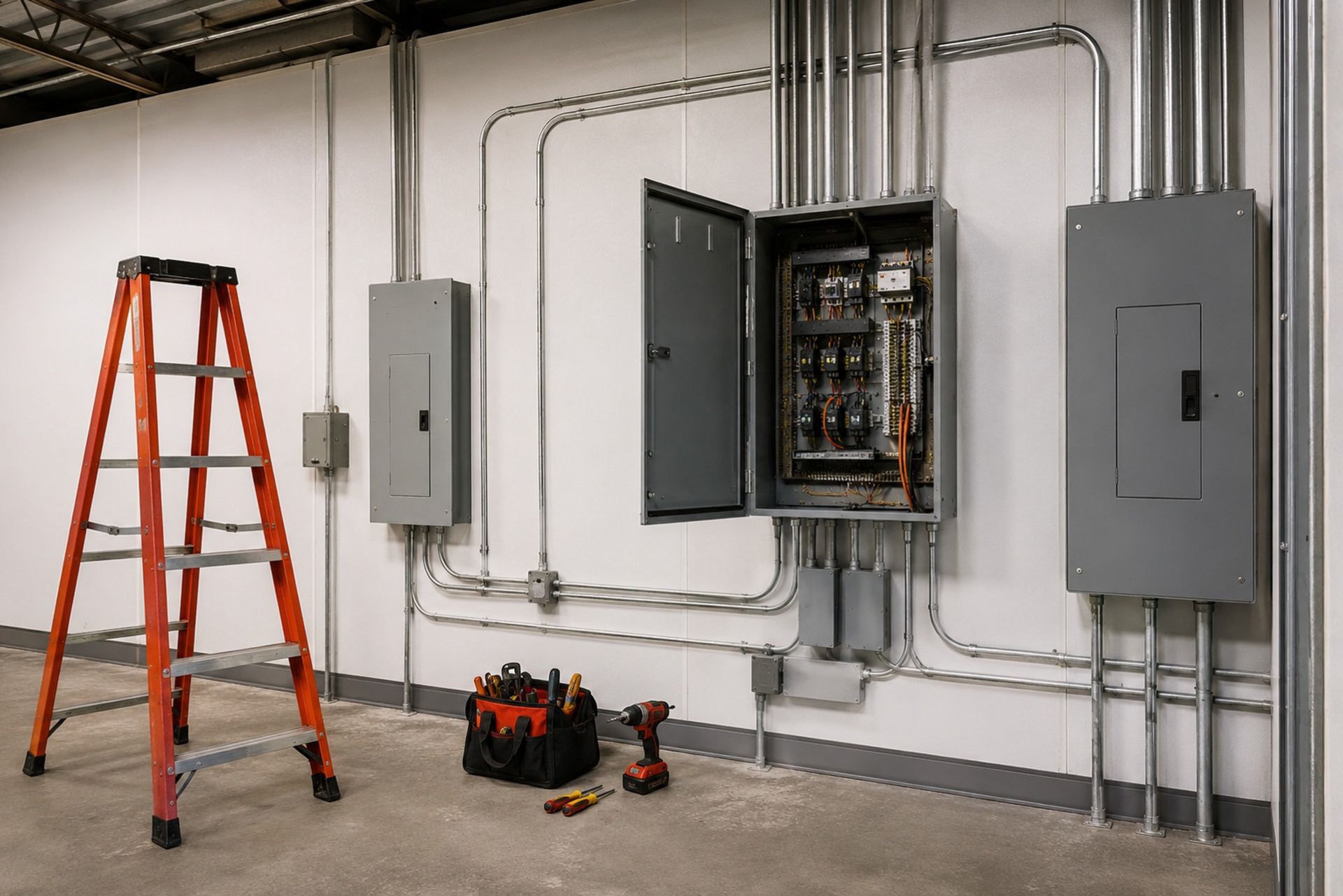

General liability is the foundation of every electrician's insurance program, and in Independence, the stakes are real. A significant portion of the city's residential housing was built before 1980, which means you're regularly working around older wiring systems, knob-and-tube remnants, and panels that don't meet current code. One accidental fire sparked during a panel upgrade can generate a six-figure claim before the smoke clears.

Your GL policy should cover bodily injury, property damage, and completed operations. That last piece is critical: completed operations coverage protects you if a job you finished six months ago causes damage down the line. A bad connection that eventually overheats and causes a fire? That's a completed operations claim. Most standard GL policies for electricians in Missouri carry limits of $1 million per occurrence and $2 million aggregate, but some commercial and industrial jobs in the Independence area will require higher limits or umbrella coverage.

One mistake I see contractors make is assuming their GL policy covers faulty workmanship itself. It doesn't. GL covers the resulting damage from faulty work, not the cost to redo the work. That distinction matters when you're negotiating contracts with general contractors on larger projects.

Workers' Compensation Requirements in Missouri

Missouri requires workers' compensation for any employer with five or more employees, but here's the catch: in the construction trades, the requirement kicks in with just one employee. If you have even a single W-2 worker, you need a workers' comp policy. Sole proprietors can exempt themselves, but doing so can cost you jobs since many GCs won't let you on-site without proof of coverage.

Workers' comp rates in Missouri for electricians typically fall under class code 5190, which covers electrical wiring within buildings. Your experience modification rate (EMR) directly impacts your premium. An EMR above 1.0 means you're paying more than the industry average due to past claims. Getting that number down through documented safety programs and return-to-work protocols can save you thousands annually.

Joule Pro works specifically with electrical contractors to find workers' comp markets that understand the trade, which matters because a generalist agent might not know how to properly classify your payroll or structure your policy to avoid audit surprises.

Inland Marine Coverage for Specialized Electrical Tools

Your tools and equipment aren't cheap. A fully stocked service van can easily carry $15,000 to $30,000 worth of meters, benders, wire pullers, and diagnostic equipment. Standard commercial property policies typically don't cover tools in transit or on job sites - that's where inland marine fills the gap.

Inland marine policies cover your tools and equipment wherever they go: in your van, on a job site, or in temporary storage. In Independence, tool theft from work vehicles remains a persistent problem, particularly in commercial areas along Noland Road and near the I-70 corridor. A good inland marine policy replaces stolen or damaged equipment at replacement cost, not depreciated value, so you're not stuck buying used replacements out of pocket.

By: Michael Fusco

President of Joule Pro

INDEX

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Navigating Independence City Permitting and Bonding

City of Independence Contractor Licensing Requirements

Independence operates its own contractor licensing system separate from Kansas City. Electrical contractors must hold a valid license through the city's Community Development Department, and the application process requires proof of insurance. Specifically, you'll need to show current certificates for general liability and workers' compensation before your license is issued or renewed.

The city also has its own electrical code enforcement, and inspections are handled locally. Independence has been transitioning to Advanced Metering Infrastructure through its municipal utility, Independence Power and Light, which means electricians working on service upgrades and meter base replacements need to understand the specific requirements IPL sets for new installations. Your insurance should reflect the type of work you're actually performing, because a policy written for basic residential maintenance won't adequately cover you if you're doing commercial service upgrades tied to new smart meter installations.

Surety Bonds and Performance Guarantees

Independence requires electrical contractors to carry a surety bond as part of the licensing process. This bond protects the city and its residents if you fail to complete permitted work or violate code requirements. The bond amount is typically $10,000 for electrical contractors, though it can vary based on the scope of your license.

A surety bond is not insurance - it's essentially a guarantee that you'll fulfill your obligations. If a claim is made against your bond, the surety company pays out and then comes after you for reimbursement. Your credit score, financial history, and business track record all affect your bond premium. Contractors with strong credit can expect to pay 1-3% of the bond amount annually, while those with credit issues may pay significantly more.

Performance bonds are a separate consideration, usually required on larger commercial or municipal projects. If you're bidding on public work in Independence or Jackson County, expect to provide both a performance bond and a payment bond.

Local Risk Factors and Environmental Considerations

Severe Weather and Storm Damage Risks in Jackson County

Jackson County sits squarely in tornado alley, and Independence takes its share of severe weather hits. Straight-line winds, hail, and ice storms create surges in emergency electrical work - downed service lines, damaged panels, and storm-related fires. While that's good for business, it also increases your exposure.

Storm-related work often happens under time pressure, in dangerous conditions, and sometimes on properties with structural damage you can't fully assess. Your GL and workers' comp policies need to account for this elevated risk. If you're doing storm restoration work, make sure your policy doesn't exclude emergency or temporary repairs, and confirm that your coverage extends to work performed outside normal business hours.

Flooding along the Little Blue River and its tributaries also affects parts of Independence. Electricians called in to restore power in flood-damaged buildings face unique hazards: standing water, compromised grounding systems, and mold exposure. These are real risks that should be addressed in your safety protocols and reflected in your insurance program.

Historic District Restoration and Liability

Independence has a proud history, including the Harry S. Truman National Historic Landmark District and several other historically designated neighborhoods. Working on homes and buildings in these areas comes with additional liability because repairs and upgrades must often comply with preservation standards alongside modern electrical code.

The cost of a mistake in a historic property is amplified. Damaging original materials, failing to meet preservation guidelines, or causing a fire in a historically significant structure can result in claims that far exceed what you'd see in a standard residential job. If you regularly work in these areas, talk to your insurance provider about whether your policy limits are adequate for the increased exposure.

Carrier Appetite and Market Trends in the Kansas City Metro

Top-Rated Insurance Carriers for Missouri Tradesmen

Not every insurance carrier wants to write policies for electricians. The trade carries inherent fire risk, which makes some carriers cautious. In the Kansas City metro, the carriers with the strongest appetite for electrical contractor risks tend to be specialty or surplus lines markets rather than big national brands.

| Factor | Standard Market Carriers | Specialty/Surplus Lines |

|---|---|---|

| Electrical contractor appetite | Limited, often declined | Strong, actively seeking |

| Premium pricing | Higher due to risk aversion | Competitive for clean accounts |

| Underwriting flexibility | Rigid class codes | Tailored to trade specifics |

| Claims handling | General adjusters | Trade-experienced adjusters |

| Availability in MO | Varies widely | Consistent through specialty brokers |

Joule Pro maintains relationships with specialty underwriters who focus specifically on the electrical trade. That matters because a carrier that understands the difference between residential service work and industrial controls installation will price your policy more accurately than one that lumps all electricians into the same bucket.

Factors Affecting Premium Rates in Independence

Your premium isn't just about your trade classification. Several Independence-specific factors influence what you'll pay. The age of the housing stock increases completed operations risk. Your proximity to flood zones affects property coverage. Even your municipal utility work exposure through IPL projects can change your risk profile.

Claims history is the single biggest factor. A clean loss run over three to five years can mean premium savings of 20-30% compared to a contractor with recent claims. Revenue and payroll size, subcontractor usage, and the types of projects you take on all feed into the calculation. Contractors who primarily do new construction generally pay less than those focused on renovation and service work, simply because the risk profile differs.

Strategic Risk Management and Safety Best Practices

The cheapest insurance claim is the one that never happens. Independence electricians should implement documented safety programs that include regular toolbox talks, proper PPE protocols, and job-site hazard assessments. Missouri's Division of Workers' Compensation offers resources for employers looking to build compliant safety programs, and maintaining those records can directly reduce your EMR over time.

Investing in ongoing training pays off in multiple ways. OSHA 10 and OSHA 30 certifications for your crew signal to carriers that you take safety seriously, which can influence underwriting decisions. Documenting everything - from daily job logs to incident reports - creates a paper trail that protects you during audits and claims investigations.

Frequently Asked Questions

Do I need separate insurance to work on Independence Power and Light projects? You may need higher liability limits or specific endorsements depending on the project scope. IPL often has its own insurance requirements for contractors working on utility-connected infrastructure.

Can I use my Kansas City contractor license in Independence? No. Independence maintains its own licensing system, and you'll need to apply separately through the city's Community Development Department with proof of insurance and bonding.

How much does general liability cost for an electrician in Independence? Expect to pay between $2,500 and $6,000 annually for a standard $1M/$2M policy, depending on your revenue, claims history, and the type of work you perform.

What happens if I don't carry workers' comp in Missouri? You face penalties including fines up to $50,000, potential criminal charges, and personal liability for any workplace injuries. GCs will also refuse to let you on their job sites.

Does my inland marine policy cover tools left in an unlocked vehicle?

Most policies require evidence of forced entry for theft claims. Leaving your van unlocked could void your coverage for stolen tools.

Making the Right Choice for Your Business

Getting the right insurance for your Independence electrical contracting business isn't about finding the cheapest quote. It's about matching your coverage to the actual risks you face: older homes, storm exposure, historic properties, and a local permitting environment that demands specific documentation. A program built specifically for electrical contractors, like what Joule Pro offers through its specialty markets, gives you coverage that fits your trade rather than a one-size-fits-all policy designed for general contractors. Reach out to a licensed producer who understands the electrical trade and can walk you through your options based on the work you actually do in Independence.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.