Business Insurance

Great Falls, MT Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

Great Falls sits at the confluence of the Missouri River and some of Montana's harshest weather patterns, which means electricians here face a risk profile you won't find in Billings or Missoula. Between aging commercial infrastructure downtown, wind-driven wildfire seasons that seem to stretch longer every year, and a permitting process that tightened considerably in 2025, running an electrical contracting business in Cascade County demands more than just technical skill. It demands the right insurance stack. This guide covers the specific coverage requirements, local permitting nuances, city-specific hazards, and carrier appetite that Great Falls electricians need to understand before signing or renewing a policy. If you've been relying on a generalist agent who treats your trade the same as a plumber or roofer, you're probably leaving gaps on the table.

Core Insurance Requirements for Great Falls Electrical Contractors

General Liability and Property Damage Coverage

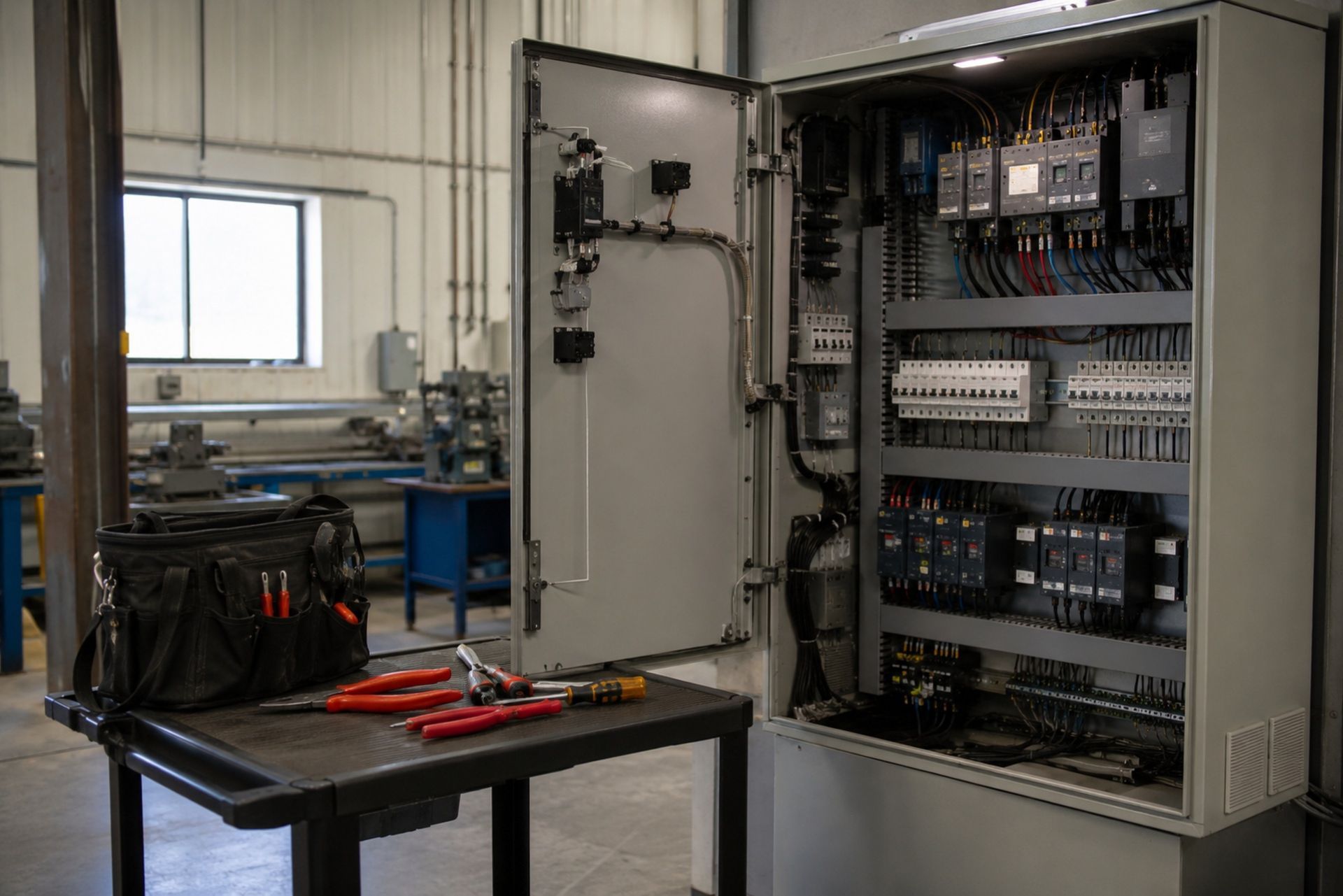

General liability (GL) is the foundation of every electrical contractor's insurance program, and in Great Falls, it carries some specific weight. A single arc flash incident during a panel upgrade in one of the city's older homes can cause tens of thousands of dollars in fire damage before the homeowner even calls 911. GL policies for electricians typically cover third-party bodily injury, property damage, and completed operations claims, which means you're protected even after the job is done and you've moved on.

Most Great Falls general contractors require subcontractors to carry at least $1 million per occurrence and $2 million aggregate in GL coverage before stepping onto a jobsite. Some commercial projects tied to Malmstrom Air Force Base or the Great Falls Clinic facilities push that to $5 million, often requiring an umbrella policy on top. If you're bidding on anything beyond basic residential service calls, your GL limits matter.

Montana Workers' Compensation Compliance

Montana is a mandatory workers' compensation state, and there's no wiggle room here. If you have even one employee, you need a workers' comp policy. The state classifies electrical work under NCCI code 5190, and premiums in Montana tend to run higher than the national average because of the smaller risk pool and elevated injury rates in the trades.

One thing to keep in mind: Montana's Independent Contractor Exemption Certificate (ICEC) doesn't automatically shield you from workers' comp obligations. If a subcontractor you hire doesn't carry their own coverage or a valid ICEC, you could be on the hook for their injuries. This is one of the most common and expensive mistakes I see small shops make.

Inland Marine Insurance for Tools and Equipment

Your wire pullers, conduit benders, and diagnostic meters don't stay in one place. They ride in your van, sit in job trailers, and sometimes spend weeks on a commercial site across town. A standard property policy won't cover tools and equipment in transit or at a temporary location, which is exactly why inland marine coverage exists.

For a typical Great Falls electrical shop running $30,000 to $75,000 in mobile tools and equipment, inland marine premiums are surprisingly affordable: often $500 to $1,500 annually. That's cheap protection against theft from a job trailer during a long weekend or damage from a vehicle break-in at a Cascade County worksite.

By: Michael Fusco

President of Joule Pro

INDEX

Core Insurance Requirements for Great Falls Electrical Contractors

Navigating Great Falls Permitting and Licensing Bonds

Mitigating Region-Specific Risks in Cascade County

Carrier Appetite and Market Trends for Montana Electricians

Customizing Your Coverage for Specialized Electrical Work

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Navigating Great Falls Permitting and Licensing Bonds

City of Great Falls Planning and Community Development Requirements

Great Falls tightened its contractor oversight recently. Starting January 1, 2025, electricians must submit an annual Contractor License Verification Form costing $45 and provide proof of current insurance coverage. The city's Planning and Community Development office handles electrical permits, and they've gotten more diligent about verifying that contractors carry active GL and workers' comp before issuing permits.

Electrical permits in Great Falls are required for nearly all work beyond simple fixture replacements. New circuits, panel upgrades, service changes, and any work in commercial buildings all require a permit and inspection. Failing to pull permits doesn't just risk fines: it can void your insurance coverage if a claim arises from unpermitted work. That's a gap that could sink a small business.

The Role of Surety Bonds in the Local Permitting Process

Montana requires electrical contractors to carry a surety bond as part of their state licensing. The bond amount is typically $5,000 to $10,000, depending on your license class. This bond protects consumers if you fail to complete work or violate licensing regulations.

Surety bonds are not insurance: they're a guarantee that you'll perform your obligations, and if the bonding company pays out a claim, they'll come after you for reimbursement. That said, maintaining a clean bond history makes you more attractive to both customers and insurance carriers. A specialty program like Joule Pro, which works exclusively with licensed electrical contractors, can often bundle bond facilitation alongside your core coverage to simplify the process.

Mitigating Region-Specific Risks in Cascade County

Extreme Weather Impacts on Electrical Infrastructure

Great Falls averages wind speeds that rank among the highest in Montana, and those sustained gusts wreak havoc on overhead service lines, exterior panels, and temporary power setups on construction sites. Winter temperatures regularly dip below zero for weeks at a stretch, creating freeze-thaw cycles that damage underground conduit and outdoor junction boxes.

Wildfire smoke and ash from surrounding forest and grassland fires have also become a growing concern for electrical contractors working on exterior installations. Smoke particulate can cause premature failure of outdoor electrical components, leading to warranty and completed operations claims. Your GL policy's completed operations coverage becomes critical in these scenarios: make sure it's included and not carved out.

Commercial vs. Residential Risk Profiles in Central Montana

Residential work in Great Falls tends to involve older homes, many built in the 1940s through 1970s, with aluminum wiring, outdated panels, and knob-and-tube remnants. These jobs carry higher fire risk and more frequent claims than new construction. Carriers know this, and your premium will reflect it if your book of work skews heavily toward older residential rewiring.

Commercial work, especially projects tied to the military base, healthcare facilities, or the growing renewable energy sector in central Montana, carries a different risk profile. Higher contract values mean higher potential claims, but the work is often more controlled and inspected. A balanced mix of residential and commercial work can actually help your insurance profile.

| Risk Factor | Residential (Older Homes) | Commercial/Industrial |

|---|---|---|

| Fire risk | Higher (aging wiring) | Moderate (code-compliant) |

| Average claim size | $5,000 - $25,000 | $25,000 - $150,000+ |

| Permit scrutiny | Moderate | High |

| Completed ops exposure | High | Very high |

| Carrier preference | Selective | Preferred with experience |

Carrier Appetite and Market Trends for Montana Electricians

Preferred Insurance Carriers for Small to Mid-Sized Shops

Not every carrier wants to write electricians, and fewer still are comfortable with Montana's small market and extreme weather exposure. The carriers that do write electrical contractors in Great Falls tend to be specialty or surplus lines markets rather than the big national names you see advertising during football games.

Joule Pro maintains relationships with underwriters who specifically understand electrical trade risks, which matters when you're trying to get competitive pricing on a GL policy that includes completed operations for panel upgrades in 80-year-old homes. A generalist agent submitting your application to a carrier that rarely writes electricians is a recipe for either a declination or an inflated premium.

Factors Influencing Premium Rates in the 406 Area Code

Several factors drive what you'll pay for electrician insurance in Great Falls specifically:

- Payroll size and employee count directly affect workers' comp premiums

- Your experience modification rate (EMR) can swing comp costs by 20-40%

- Revenue mix between residential, commercial, and industrial work

- Claims history over the past three to five years

- Whether you perform any high-voltage or renewable energy work

- The age and condition of your fleet vehicles (for commercial auto)

Great Falls contractors often pay 10-15% more than their counterparts in larger Montana cities simply because the local risk pool is smaller. Shopping your coverage through a program designed for electricians, rather than a general contractor program, can offset some of that premium pressure.

Customizing Your Coverage for Specialized Electrical Work

Running an electrical contracting business in Aurora means managing a specific set of risks that generic insurance advice doesn't address. Between the city's registration requirements, the historic building stock downtown, and the industrial facilities on the east side, your coverage needs to be tailored to the work you actually do.

The smartest move is working with a producer who understands electrical trade exposures - not a generalist who writes policies for restaurants and retail stores on the same desk. Joule Pro, backed by Fusco Orsini & Associates Insurance Services (CA Lic. 0H16057), offers direct producer access for Aurora electricians who want quotes and policy guidance from someone who speaks their language. Reach out to get a coverage review that matches your actual risk profile, not a one-size-fits-all template.

Professional Liability for Electrical Design and Consulting

If you're doing any design-build work, providing engineering consultation, or specifying equipment for commercial projects, your GL policy won't cover errors in your professional judgment. That's where professional liability, sometimes called errors and omissions (E&O), comes in.

A design flaw in a lighting control system for a Great Falls commercial building that leads to a project delay and cost overruns is a professional liability claim, not a GL claim. These policies typically start around $1,500 annually for small shops and scale with revenue and project complexity.

Pollution Liability for Industrial and Renewable Energy Projects

Electrical work sometimes intersects with environmental exposure, particularly when you're handling transformer oil, battery storage systems, or decommissioning older industrial equipment containing PCBs. Standard GL policies exclude pollution events, so if you're doing any industrial or renewable energy work in the Cascade County area, a pollution liability endorsement or standalone policy is worth the conversation.

Solar installations and battery storage projects are growing across central Montana, and the environmental liability associated with lithium-ion battery systems is something carriers are paying close attention to in 2026.

Best Practices for Maintaining Robust Protection

Keeping your insurance program effective year over year requires more than just paying premiums on time. Review your coverage annually, especially if your revenue, headcount, or scope of work has changed. A shop that added solar installations or started bidding on commercial projects needs a different coverage profile than one doing residential service calls.

Document everything: jobsite photos, signed contracts, permit records, and safety training logs. These records are your best defense when a claim hits, and carriers reward contractors who demonstrate strong risk management habits. Working with a specialty insurance provider like Joule Pro, which understands the specific exposures electrical contractors face, gives you access to a licensed producer who can spot coverage gaps before they become expensive lessons.

If you're a Great Falls electrician operating without a thorough coverage review in the last 12 months, now is the time. Reach out to Joule Pro to get a quote tailored to your specific trade, territory, and risk profile.

FAQ

Do I need insurance to pull an electrical permit in Great Falls? Yes. The city requires proof of active general liability and workers' compensation (if you have employees) before issuing electrical permits.

How much does general liability cost for a Great Falls electrician? Most small to mid-sized shops pay between $2,500 and $6,000 annually, depending on revenue, claims history, and scope of work.

Can I use my personal auto insurance for my work van? No. Personal auto policies exclude vehicles used for commercial purposes. You need a commercial auto policy to cover your work vehicles.

What happens if my subcontractor doesn't have insurance? In Montana, you can be held liable for their injuries and any damage they cause. Always verify subcontractor insurance certificates before they start work.

Is pollution liability really necessary for electricians? If you handle transformer oil, battery systems, or work on industrial sites with environmental exposure, yes. Standard GL policies exclude pollution events entirely.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.