Business Insurance

West Jordan, UT Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

West Jordan sits in a unique pocket of the Salt Lake Valley where rapid residential growth collides with aging commercial infrastructure, and that combination creates insurance scenarios most electricians don't think about until a claim hits. Whether you're pulling wire in a new subdivision near the Jordan River or upgrading panels in older buildings along Redwood Road, the coverage you carry needs to reflect the specific risks of working in this city. This guide breaks down the insurance requirements, local permitting rules, city-specific hazards, and carrier preferences that shape electrician insurance in West Jordan, UT, so you can make informed decisions about your coverage stack.

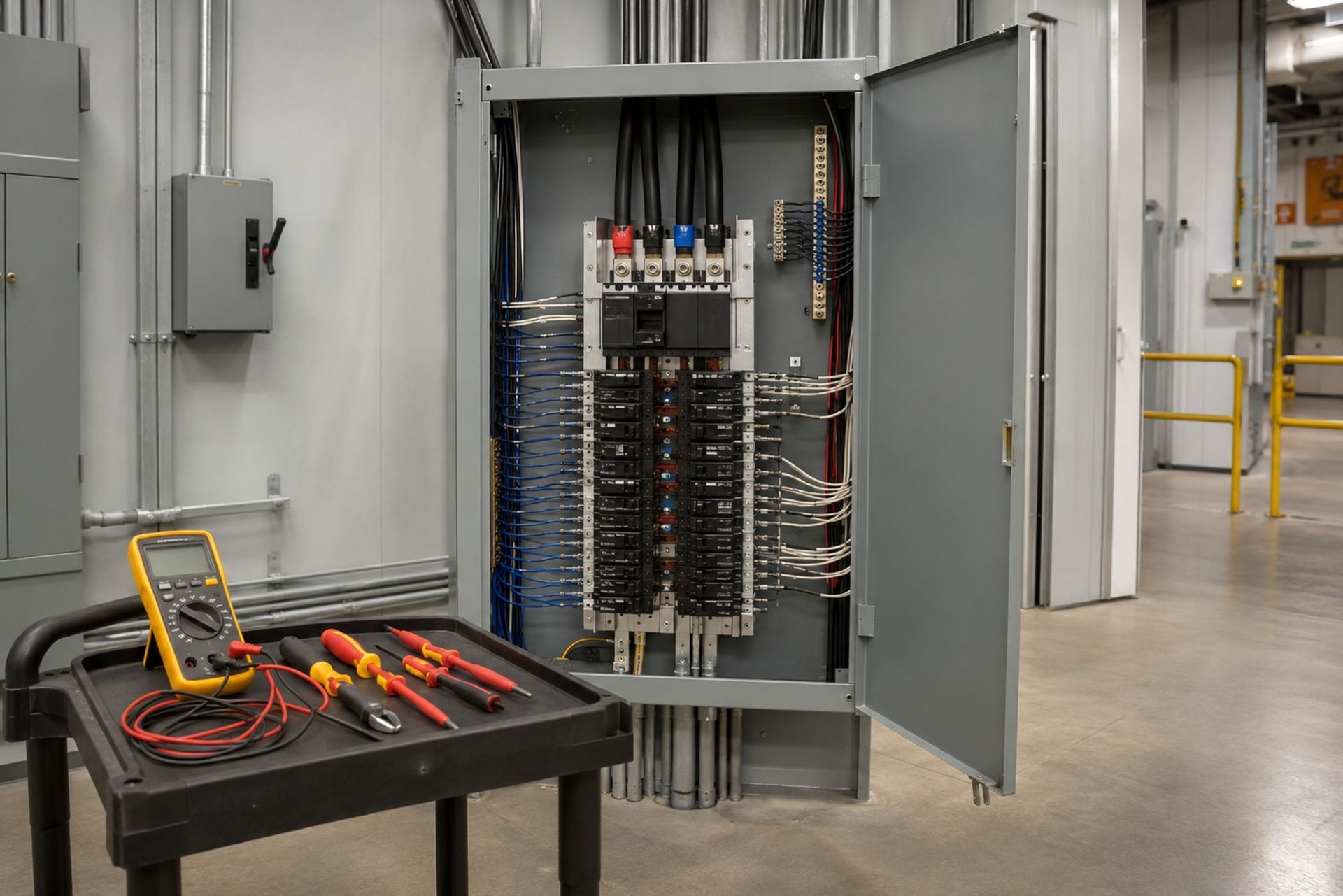

If you're a licensed electrical contractor operating here, you're dealing with a market that treats your trade differently than a general handyman or plumber. Insurers evaluate electricians based on fire risk, arc flash exposure, and the type of work you perform: residential rewires carry different weight than commercial tenant improvements. Understanding how carriers think about your business is half the battle. The other half is making sure your policies, permits, and bonds all line up so a single oversight doesn't shut down a job or leave you personally exposed.

Essential Insurance Policies for West Jordan Electrical Contractors

General Liability and Property Damage Coverage

General liability is the foundation of every electrical contractor's insurance program, and Utah has recently tightened its requirements. Effective April 20, 2026, Utah electricians must carry a minimum general liability insurance limit of $1,000,000 per occurrence. That's not optional: it's a licensing condition enforced by the state Division of Occupational and Professional Licensing (DOPL).

Most West Jordan electricians should carry limits of $1M/$2M (per occurrence/aggregate) at minimum. If you're doing commercial work or projects for general contractors, you'll often need $2M per occurrence just to get on a bid list. Your GL policy covers third-party bodily injury and property damage, which means if you accidentally start a fire in a client's home or a visitor trips over your equipment on a job site, the policy responds.

One coverage gap that catches electricians off guard is the completed operations exposure. If you finish a panel upgrade in March and the work causes a fire in September, your GL policy's completed operations coverage handles that claim, but only if you haven't let the policy lapse. Keep your GL active continuously, even during slow months.

Utah Workers' Compensation Requirements

Utah requires workers' compensation insurance for all employers, including electrical contractors with even one employee. Sole proprietors can exempt themselves, but subcontractors working under a general contractor will almost always be required to carry it regardless. If you don't have workers' comp and a GC's auditor catches it, you're off the project.

Workers' comp rates for electricians in Utah are based on NCCI class codes, with residential wiremen (class code 5190) typically paying less than those doing commercial or industrial work. Expect base rates in the range of $4 to $8 per $100 of payroll, depending on your experience modification factor and claims history. A clean three-year loss run can save you thousands annually.

Commercial Auto and Inland Marine for Tool Protection

Your personal auto policy won't cover your van if it's loaded with tools and used for business. Commercial auto insurance is essential for any electrician who drives to job sites, and in West Jordan's spread-out geography, that's basically everyone.

Inland marine coverage protects your tools and equipment whether they're in your vehicle, on a job site, or in transit. A single theft from an unlocked van can easily cost $10,000 to $30,000 in replacement tools. Programs built specifically for electrical contractors, like those offered through Joule Pro, bundle inland marine with your other policies so nothing falls through the cracks. This matters because a generalist agency might not know to ask whether your wire pullers, conduit benders, and testing equipment need scheduled coverage.

By: Michael Fusco

President of Joule Pro

INDEX

Essential Insurance Policies for West Jordan Electrical Contractors

Navigating West Jordan City Permitting and Bonding

Local Risk Factors and Environmental Hazards in the Salt Lake Valley

Carrier Appetite and Market Trends for Utah Electricians

Cost Optimization and Selecting a West Jordan Insurance Provider

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Navigating West Jordan City Permitting and Bonding

West Jordan Building Safety Department Requirements

West Jordan's Building Safety Department oversees electrical permits for all work within city limits. You'll need a permit for most electrical work beyond simple fixture replacements, and the city requires that permit applicants show proof of current insurance and state licensure.

Inspections in West Jordan follow the 2021 International Building Code (IBC) and the National Electrical Code (NEC) as adopted by Utah. The city has been processing permits more quickly since transitioning to an online portal, but plan for at least 3 to 5 business days for standard residential permits. Commercial projects take longer, especially if they involve plan review.

One practical tip: keep digital copies of your insurance certificates, state license, and bond documentation on your phone or in a cloud folder. West Jordan inspectors occasionally ask for proof on site, and having it ready avoids delays.

License Bonds and State of Utah DOPL Compliance

Utah DOPL requires electrical contractors to maintain a contractor license bond as a condition of licensure. The bond amount depends on your license classification, but most electrical contractors need a $50,000 surety bond. This bond protects consumers if you fail to complete a project or violate state contracting laws.

The bond is not insurance: it's a financial guarantee. If a claim is paid against your bond, you owe the surety company that money back. Your insurance policies (GL, workers' comp, auto) handle the actual risk transfer. Confusing the two is a common mistake among newer contractors who assume their bond covers property damage or injuries.

Renewal timing matters here. Your DOPL license, surety bond, and insurance policies all have different expiration dates. Set calendar reminders 60 days before each renewal to avoid any gaps that could trigger a license suspension.

Local Risk Factors and Environmental Hazards in the Salt Lake Valley

Seismic Activity and Structural Wiring Integrity

The Wasatch Fault runs directly through the Salt Lake Valley, and West Jordan sits squarely in a high seismic risk zone. For electricians, this means two things: first, the wiring in older homes and commercial buildings may have been compromised by years of minor seismic activity, creating hidden hazards during renovation work. Second, your liability exposure increases when you're working on structures that may not meet current seismic codes.

If you're doing retrofit work in pre-1990 buildings, document everything with photos before you start. Insurers want to see that existing damage wasn't caused by your work. A thorough pre-job documentation habit can be the difference between a denied claim and a covered one.

Seismic risk also affects your property coverage. If you own or lease a shop in West Jordan, make sure your commercial property policy includes earthquake coverage, which is typically a separate endorsement in Utah.

Wildfire Risks and Outdoor Electrical Infrastructure

West Jordan's western edge borders open land and foothills that carry wildfire risk during dry summers. Electricians working on outdoor installations, solar arrays, EV charging stations, or utility connections in these areas face heightened liability if their work is later connected to a fire ignition.

The Utah Division of Forestry, Fire and State Lands tracks wildfire risk zones, and several West Jordan neighborhoods fall within the wildland-urban interface. If you're installing outdoor electrical infrastructure in these areas, confirm that your GL policy doesn't exclude wildfire-related claims. Some carriers add wildfire exclusions in high-risk western states, and you don't want to discover that gap after a loss.

Carrier Appetite and Market Trends for Utah Electricians

Preferred Carriers for Residential vs. Commercial Specialists

Not every insurance carrier wants to write electrician policies, and the ones that do often have strong preferences about what type of electrical work they'll cover. Residential-focused electricians generally have an easier time finding coverage because the risk profile is more predictable. Carriers like Employers, BHHC, and several admitted markets actively write residential electrical contractors in Utah.

Commercial and industrial electricians face a tighter market. High-voltage work, fire alarm installations, and projects involving occupied buildings push many standard carriers away. That's where specialty programs matter. Joule Pro works with underwriters who specifically understand electrical trade risks, which means you're not trying to explain your business to a generalist underwriter who thinks all contractors are the same.

Carrier appetite also shifts based on geography. Utah's relatively low litigation environment compared to states like California or Florida makes the state attractive to many insurers, but individual carriers still evaluate West Jordan's claims trends separately from, say, Park City or St. George.

Impact of Local Claims History on Regional Premiums

Your individual claims history matters most, but regional loss data influences your premiums too. The Salt Lake Valley has seen increased construction activity over the past five years, and with more electrical work being performed, claim frequency has ticked upward. Water damage from improperly sealed exterior penetrations and fire losses from faulty connections are the two most common claim types for Utah electricians.

If your experience mod is above 1.0, expect to pay more and have fewer carrier options. Getting it below 1.0 requires at least three clean years, and it's worth the effort: a 0.85 mod on a $15,000 workers' comp premium saves you $2,250 annually.

Cost Optimization and Selecting a West Jordan Insurance Provider

The cheapest policy isn't always the best value, especially in a trade where a single fire claim can exceed $500,000. Here's a practical comparison of what different coverage tiers look like for a typical West Jordan electrical contractor:

| Coverage Element | Basic Package | Comprehensive Package |

|---|---|---|

| General Liability | $1M/$2M occurrence/aggregate | $2M/$4M occurrence/aggregate |

| Workers' Comp | State minimum | State minimum + lower mod discount |

| Commercial Auto | Liability only | Liability + comprehensive/collision |

| Inland Marine | $25,000 tool limit | $75,000+ scheduled equipment |

| Umbrella | None | $1M excess liability |

A basic package for a two-person residential shop might run $6,000 to $10,000 annually. A comprehensive package for a commercial crew of eight could range from $25,000 to $45,000, depending on payroll and vehicle count.

Working with a producer who specializes in electrical contractors, like the team at Joule Pro backed by Fusco Orsini & Associates Insurance Services (CA Lic. 0H16057), gives you access to markets that generalist brokers simply don't have. That direct producer access means your questions get answered by someone who understands the difference between a service upgrade and a tenant improvement, and why that distinction affects your premium.

Frequently Asked Questions

Do I need insurance to pull an electrical permit in West Jordan? Yes. West Jordan's Building Safety Department requires proof of current insurance and state licensure before issuing electrical permits.

How much does general liability cost for a West Jordan electrician? Solo operators typically pay $1,500 to $3,500 annually for a $1M/$2M policy. Larger crews and commercial specialists pay more based on revenue and payroll.

Can I exclude myself from workers' comp as a sole proprietor in Utah? You can, but most general contractors will require you to carry it anyway before they'll let you on their job sites.

Does my insurance cover earthquake damage to a client's property? Standard GL policies typically cover your negligence during an earthquake, but damage from the earthquake itself is usually excluded. Review your policy's earth movement exclusion carefully.

What's the difference between my surety bond and my liability insurance? Your bond protects consumers against contract violations and is repayable to the surety. Your insurance protects you against third-party claims and doesn't require repayment after a covered loss.

Making the Right Choice for Your Electrical Business

Getting your insurance right in West Jordan means accounting for the city's permitting requirements, the valley's seismic and wildfire exposures, and the specific way carriers evaluate electrical contractors. Don't treat insurance as a checkbox: treat it as the financial backbone of your business. A well-structured program protects your license, your assets, and your ability to keep bidding on work.

Start by reviewing your current policies against the requirements outlined here. If you're unsure whether your coverage matches your actual risk profile, reach out to a specialty producer who works exclusively with electricians. The right coverage at the right price exists, but it takes someone who knows this trade inside and out to find it.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.