Business Insurance

Albuquerque, NM Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

Underwriting Preferences for Residential vs. Industrial Projects

Running an electrical contracting business in Albuquerque means dealing with a unique mix of challenges you won't find in most other U.S. markets. Between the high-desert climate that punishes equipment, monsoonal storms that flood job sites without warning, and a local permitting process that demands specific insurance documentation, getting your coverage right isn't optional: it's the foundation your business stands on. This guide to electrician insurance in Albuquerque covers the coverage types you actually need, the city-specific risks that shape your policy, local permitting and bonding requirements, and which carriers have appetite for electrical contractors in central New Mexico. Whether you're a solo journeyman pulling permits in the North Valley or running a 30-person commercial crew near Kirtland Air Force Base, the insurance decisions you make here directly affect whether you can bid on work, survive a claim, and keep your doors open. Albuquerque's construction market has stayed active through 2026, with ongoing residential growth in the mesa west and commercial projects along the I-25 corridor. That growth means more opportunity, but also more exposure. Here's what you need to know to protect yourself properly.

Essential Insurance Coverages for Albuquerque Electrical Contractors

General Liability and Property Damage Requirements

General liability (GL) is the non-negotiable starting point for any Albuquerque electrician. It covers third-party bodily injury and property damage claims: think a homeowner tripping over your cable run, or an accidental fire caused during a panel upgrade. Most general contractors in Albuquerque require subcontractors to carry at least $1 million per occurrence and $2 million aggregate before they'll even consider adding you to a bid.

What catches some electricians off guard is the completed operations component. If a circuit you installed two years ago causes a house fire, your GL policy's completed operations coverage is what responds. Skipping this or letting it lapse after a project closes is one of the most common and costly mistakes I see contractors make.

For Albuquerque-specific work, pay attention to your policy's exclusion list. Some carriers exclude damage caused by work on adobe or older stucco structures, which are everywhere in the city's historic neighborhoods like Old Town and Barelas. If you're doing residential rewiring in those areas, confirm your policy doesn't leave you exposed.

Workers' Compensation Compliance in New Mexico

New Mexico requires workers' compensation insurance for virtually all employers, with very few exceptions. If you have even one employee, you need a policy. The state's Workers' Compensation Administration enforces this aggressively, and penalties for non-compliance include fines up to $10 per day per employee plus personal liability for any injuries.

Electrical work carries higher classification codes, which means your premiums reflect the real danger of the trade. In Albuquerque, where summer temperatures regularly exceed 100°F and crews work in attics that can hit 140°F, heat-related injuries drive claims frequency up. A strong safety program and clean loss history can earn you experience modification rate (EMR) credits that meaningfully reduce your premium over time.

One thing to keep in mind: New Mexico doesn't allow employers to opt out of workers' comp through alternative benefit plans like Texas does. There's no workaround here. Get the policy.

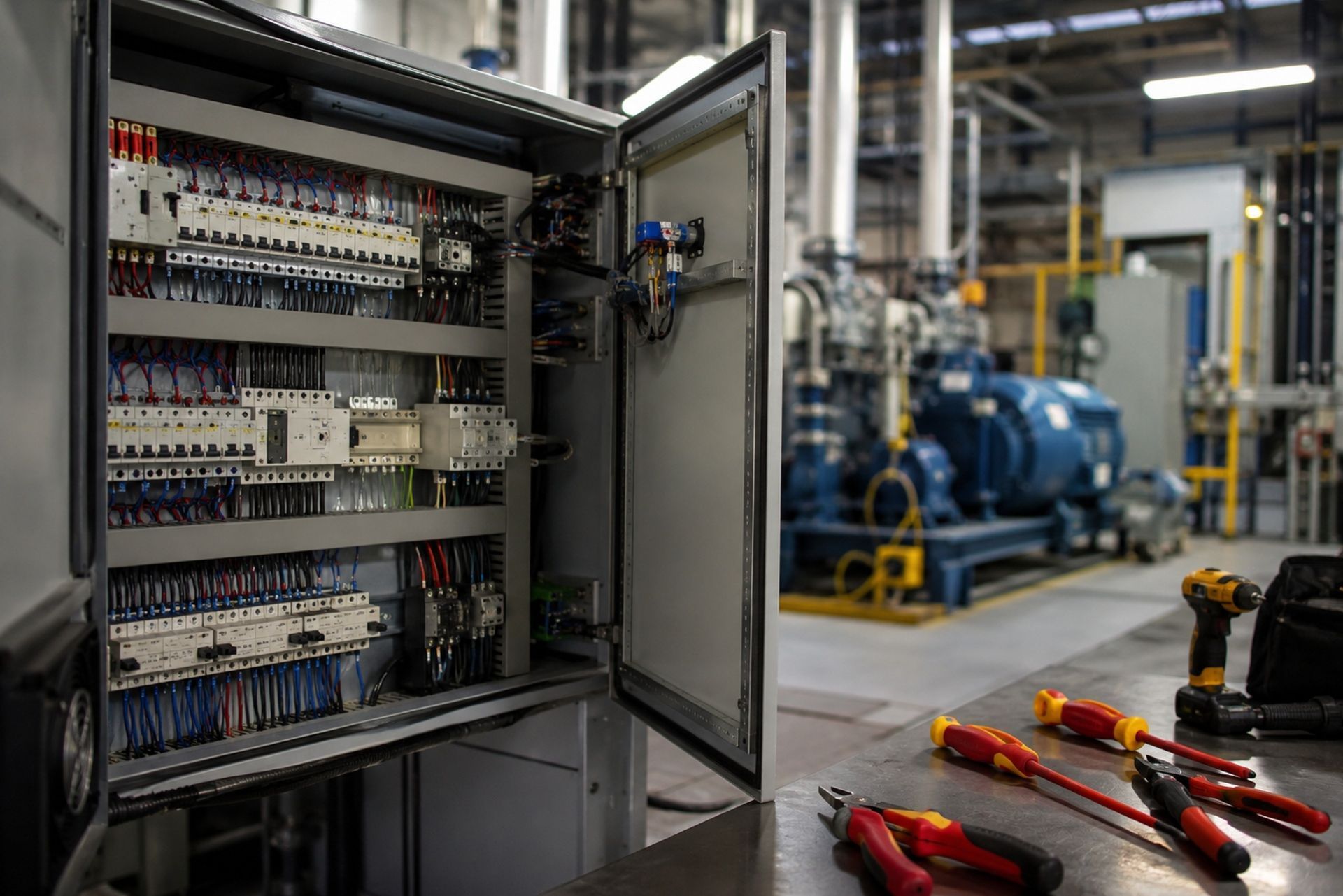

Inland Marine Insurance for Tools and Mobile Equipment

Your tools and diagnostic equipment travel with you, and a standard commercial property policy won't cover them once they leave your shop. That's where inland marine insurance comes in. The average cost of an inland marine policy with roughly $10,000 in tool coverage for Albuquerque electricians runs about $41 per month, a manageable expense that protects wire pullers, meters, conduit benders, and everything else in your van.

This coverage matters more in Albuquerque than in many cities because burglary rates rose 11% in 2024, and tool theft from work vans remains a persistent problem across Bernalillo County. If someone smashes your van window overnight and cleans out $8,000 worth of Fluke meters and Milwaukee power tools, inland marine is what makes you whole.

By: Michael Fusco

President of Joule Pro

INDEX

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Navigating City of Albuquerque Licensing and Bonding

Meeting CID and Albuquerque Planning Department Bond Mandates

New Mexico's Construction Industries Division (CID) oversees contractor licensing statewide, and you'll need an active CID license before pulling any electrical permits in Albuquerque. The CID requires a surety bond: $10,000 for general contractors and varying amounts depending on your license classification. This bond isn't insurance for you; it protects the public if you fail to complete work or violate regulations.

The City of Albuquerque's Planning Department layers additional requirements on top of state mandates. Depending on the project scope, you may need to show proof of bonding specific to the city's requirements before your permit application moves forward. Getting your CID license, your city business registration, and your bonding squared away before you start marketing saves enormous headaches. I've seen contractors lose weeks of billable time chasing paperwork they should have handled upfront.

Proof of Insurance for Local Electrical Permit Applications

When you apply for an electrical permit through the City of Albuquerque, you'll need to submit proof of insurance. The city typically requires a certificate of insurance (COI) showing active general liability coverage, and many project types require workers' comp documentation as well.

Here's where a specialty program like Joule Pro becomes genuinely useful. Because Joule Pro works exclusively with licensed electrical contractors, their team understands exactly what documentation Albuquerque's permitting office expects and can issue COIs quickly. That matters when you're trying to lock down a permit before a project timeline slips.

Keep your COIs current. An expired certificate can stall a permit renewal or trigger a stop-work order on an active job. Set calendar reminders 30 days before any policy expiration.

Mitigating High-Desert Risks and Local Environmental Hazards

Protecting Against Extreme Heat and Monsoonal Flash Flooding

Albuquerque's climate creates two distinct seasonal threats for electricians. Summer heat, often exceeding 105°F from June through August, accelerates equipment wear, increases the risk of heat illness among crews, and can cause conduit and wiring failures during installation. Your workers' comp policy covers heat-related injuries, but prevention is cheaper than claims.

Then there's monsoon season. From July through September, intense afternoon storms dump enormous amounts of rain in short bursts. Flash flooding is a real and recurring hazard across Bernalillo County, and job sites in low-lying areas near the Rio Grande or along the city's arroyos are especially vulnerable. Water damage to tools, materials, and partially completed electrical installations can be devastating.

Your inland marine policy should cover flood-related tool losses, but verify this explicitly. Some policies exclude flood damage or require a separate endorsement. Commercial auto comprehensive coverage also matters here: flash floods destroy work trucks every monsoon season in Albuquerque.

Theft Prevention and Commercial Auto Risks in Bernalillo County

Albuquerque has some of the highest property crime rates in the Southwest, and electrical contractors are frequent targets. Work vans loaded with copper wire and expensive tools are essentially rolling treasure chests for thieves. Beyond inland marine coverage, consider investing in GPS tracking for high-value tools, locking storage systems for your vans, and parking in secured lots overnight.

Commercial auto insurance is essential for any electrician operating vehicles in Albuquerque. Between the city's notorious intersection accidents along Central Avenue and the risk of flood damage during monsoon season, your trucks face real exposure daily. A minimum of $1 million in combined single-limit commercial auto coverage is standard for most contractor operations, and many GCs require it before you can bring a vehicle onto their job site.

| Coverage Type | What It Protects | Typical Minimum for ABQ Electricians |

|---|---|---|

| Typical Minimum for ABQ Electricians | Third-party injury/property damage | $1M per occurrence / $2M aggregate |

| Workers' Compensation | Employee injuries on the job | State-mandated; no minimum dollar threshold |

| Inland Marine | Tools and equipment in transit | $10,000-$50,000 depending on inventory |

| Commercial Auto | Work vehicles and liability | $1M combined single limit |

| Surety Bond (CID) | Public protection/license compliance | $10,000+ depending on classification |

Carrier Appetite and Market Trends in the Duke City

Preferred Carriers for Albuquerque Residential vs. Commercial Electricians

Not every insurance carrier wants to write electrical contractor policies, and among those that do, appetite varies significantly between residential and commercial work. Residential electricians doing panel upgrades, rewires, and new construction typically find broader carrier options because the exposure profile is more predictable. Commercial and industrial electricians, especially those working on high-voltage systems or government contracts near Kirtland or Sandia National Laboratories, face a narrower market.

Specialty programs with established underwriter relationships make a measurable difference here. Joule Pro, for example, maintains carrier partnerships specifically built around electrical contractor risk, which means faster quoting and better terms than you'd get from a generalist agency shopping your account to carriers unfamiliar with the trade. When carrier appetite is tight, those relationships matter.

Factors Influencing Insurance Premiums in Central New Mexico

Several factors drive your premium in the Albuquerque market. Your annual revenue, payroll size, number of employees, claims history, and the type of electrical work you perform all play a role. An electrician doing exclusively residential service calls will pay less than one pulling permits for commercial tenant improvements.

Your EMR is a big lever. A modifier below 1.0 signals to underwriters that your operation is safer than average, which can translate to significant premium savings. Conversely, even one serious workers' comp claim can push your EMR above 1.0 for three years, making every policy you carry more expensive.

Geographic factors also apply. Albuquerque's higher-than-average property crime rates influence inland marine and commercial auto pricing. Carriers price risk based on where you operate, and central New Mexico carries a different risk profile than, say, Santa Fe or Las Cruces.

Implementing Safety Protocols to Lower Albuquerque Insurance Costs

The fastest way to reduce your insurance costs isn't shopping for the cheapest carrier: it's reducing your claims. A documented safety program that includes regular toolbox talks, heat illness prevention protocols for Albuquerque summers, and vehicle safety training will improve your EMR over time and make your account more attractive to underwriters.

Specific steps that pay off: require daily vehicle inspections for all work trucks, install locking tool storage in every van, mandate hydration breaks during summer months, and conduct quarterly safety audits. Document everything. Carriers and auditors want to see paper trails, not just good intentions.

Investing in arc flash training and proper PPE compliance also signals to underwriters that you're serious about risk management. Some carriers offer premium credits for completing OSHA 30-hour construction safety courses, and those credits can offset the cost of the training itself within a single policy year.

Frequently Asked Questions

Do I need insurance to pull an electrical permit in Albuquerque? Yes. The City of Albuquerque requires proof of general liability insurance, and most permit types also require workers' comp documentation if you have employees.

How much does general liability cost for an Albuquerque electrician? Premiums vary based on revenue, work type, and claims history, but a typical small residential electrical contractor can expect to pay between $2,500 and $5,500 annually for a $1M/$2M policy.

Can I use a personal auto policy for my work truck? No. Personal auto policies exclude commercial use. If you're driving to job sites or hauling tools, you need a commercial auto policy.

What happens if my workers' comp lapses in New Mexico? The state can fine you, and you become personally liable for any employee injuries that occur during the lapse. It's not worth the risk.

Does Joule Pro write policies for Albuquerque electricians? Yes. Joule Pro specializes exclusively in insurance for licensed electrical contractors and has carrier relationships that serve the New Mexico market.

Your Next Steps as an Albuquerque Electrician

Getting your insurance right in Albuquerque isn't just about checking a box for permit applications. It's about building a foundation that lets you bid confidently, survive claims, and grow your business in a market with real environmental and crime-related risks. Start by auditing your current coverage against the requirements outlined here, verify your CID bond and city documentation are current, and talk to a producer who actually understands electrical contractor risk. Joule Pro's team, backed by Fusco Orsini & Associates Insurance Services (CA Lic. 0H16057), works with Albuquerque electricians daily and can help you identify gaps before they become expensive lessons. Reach out for a coverage review: it's the single smartest thing you can do for your business this year.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.