Business Insurance

Roswell, NM Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

Underwriting Preferences for Residential vs. Industrial Projects

Running an electrical contracting business in Roswell, New Mexico, means dealing with a set of risks you won't find in Albuquerque or Santa Fe. Between the Pecos Valley's flash flood potential, extreme summer heat that warps conduit and stresses outdoor panels, and a growing oil and gas sector that demands specialized maintenance, Roswell electricians face coverage questions that generic insurance guides simply don't answer. This guide breaks down the insurance requirements, permitting realities, and carrier preferences specific to Roswell and Chaves County, so you can build a policy stack that actually protects your business. Whether you're a one-truck residential shop or a crew running industrial jobs near the oilfields south of town, getting the right coverage for Roswell's unique conditions is the difference between surviving a bad claim and closing your doors.

Core Insurance Requirements for Roswell Electrical Contractors

General Liability and Property Damage Standards

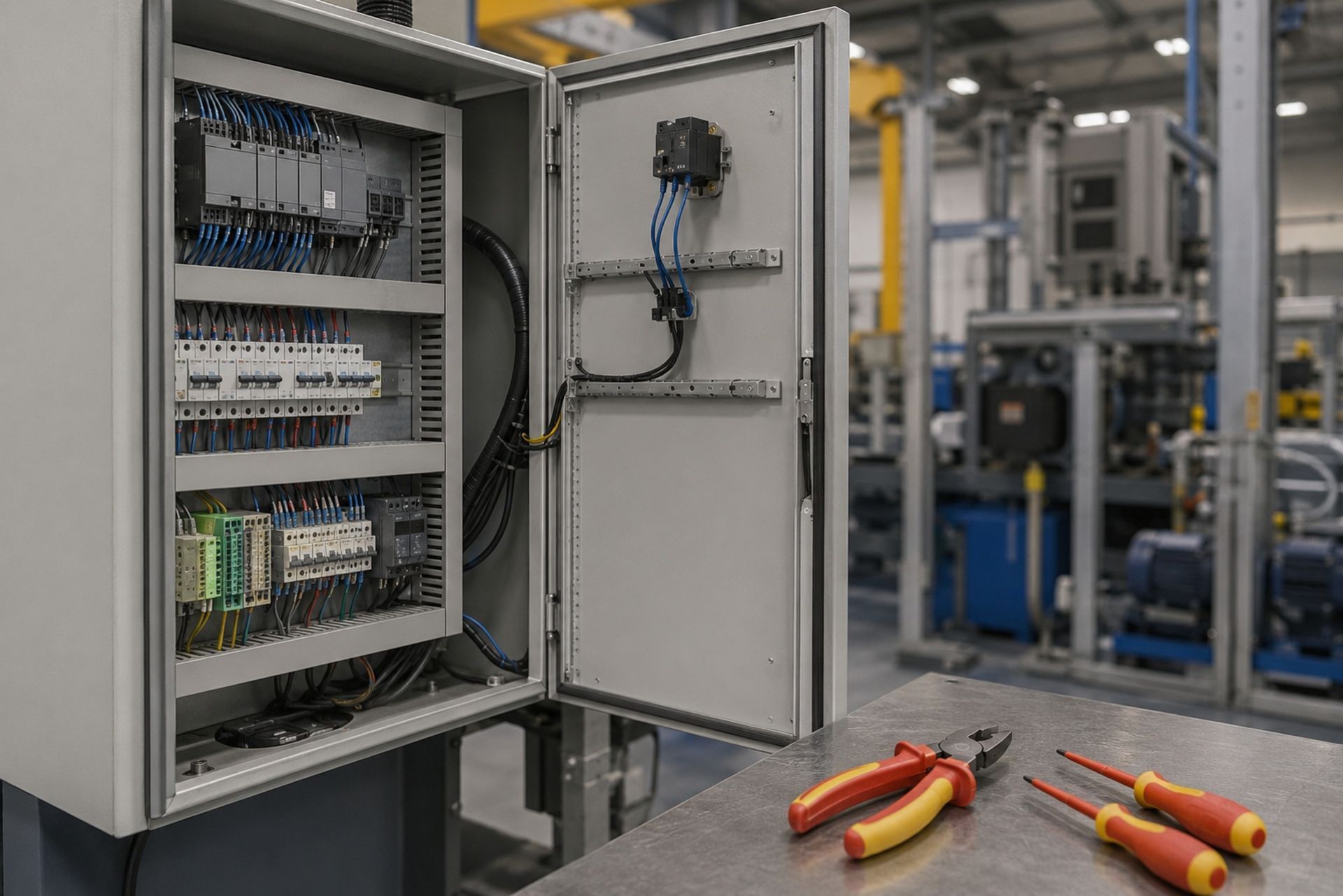

Every electrical contractor working in Roswell needs a commercial general liability (CGL) policy, and most general contractors or property owners will require proof of at least $1 million per occurrence and $2 million aggregate before you set foot on a jobsite. This covers third-party bodily injury and property damage: think a homeowner tripping over your cord, or an accidental fire sparked during a panel upgrade in one of Roswell's older adobe homes.

What catches some contractors off guard is the completed operations component. If a junction box you installed six months ago fails and causes a fire, your CGL's completed operations coverage is what responds. Skipping this or letting it lapse after project completion is one of the most common mistakes we see electricians make. Roswell's housing stock includes a mix of mid-century builds and newer subdivisions, and older wiring in those 1950s-era homes raises the stakes on every retrofit job.

Workers' Compensation Compliance in New Mexico

New Mexico requires workers' compensation insurance for any business with three or more employees, including part-time workers. Sole proprietors and partners can elect to exempt themselves, but subcontractors you hire who lack their own coverage may be counted as your employees under state law. The penalties for non-compliance are steep: fines up to $10 per day per uninsured employee, plus personal liability for any workplace injury.

Electricians face higher workers' comp classification rates than many other trades because of the inherent shock and fall hazards. In New Mexico, electrical contractors typically fall under NCCI class code 5190, and rates in 2026 hover around $4.50 to $6.00 per $100 of payroll depending on your experience modification factor. A clean claims history can shave 20% or more off that number, which is why safety programs aren't just nice to have: they directly affect your bottom line.

Commercial Auto and Inland Marine for Mobile Tool Protection

Your work van or truck is both a vehicle and a mobile warehouse. A standard personal auto policy won't cover commercial use, and it definitely won't cover the $15,000 to $40,000 worth of tools, meters, and wire stock most Roswell electricians carry. Commercial auto insurance covers liability and physical damage for vehicles used in business, while inland marine (often called a tools and equipment floater) covers your gear whether it's in the van, on a jobsite, or locked in a trailer.

One thing to keep in mind: theft from vehicles is a real problem in Roswell, particularly on jobsites near the outskirts of town. An inland marine policy from a program like Joule Pro, which is built specifically for electrical contractors, can cover tools and equipment with agreed-value terms rather than depreciated replacement, so you're not stuck replacing a $3,000 Fluke meter out of pocket.

By: Michael Fusco

President of Joule Pro

INDEX

Core Insurance Requirements for Roswell Electrical Contractors

Navigating Roswell Permitting and Licensing Bonds

Regional Risk Factors: Climate and Infrastructure in Chaves County

Carrier Appetite and Market Trends for NM Electricians

Customizing Policies for Specialized Roswell Projects

Strategies for Reducing Insurance Costs and Mitigating Liability

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Navigating Roswell Permitting and Licensing Bonds

City of Roswell Code Enforcement and Inspection Requirements

A major change took effect recently: as of January 1, 2026, the City of Roswell transitioned all electrical permitting and plan reviews to the State of New Mexico Construction Industries Division (CID). This means you no longer pull electrical permits at Roswell City Hall. Instead, permits go through the state CID office, and inspections are handled by state inspectors rather than city code enforcement.

This shift matters for insurance because CID inspectors tend to enforce the 2020 National Electrical Code more strictly than some municipal inspectors did. Callbacks and failed inspections can delay projects and increase your exposure window, the period during which your general liability policy is on the hook for jobsite incidents. Make sure your policy doesn't have restrictive project-duration limitations that could leave you uncovered during extended inspection cycles.

Surety Bonds vs. Insurance: Meeting Chaves County Mandates

New Mexico requires electrical contractors to carry a contractor's license bond through the CID, typically $10,000 for journeyman electricians and $15,000 for electrical contractors. This bond is not insurance. It protects the public if you fail to complete work or violate code, and the bonding company will come after you for reimbursement if a claim is paid.

Your CGL policy and your surety bond serve completely different purposes. The bond satisfies your state licensing requirement; the insurance protects your business assets. Some contractors confuse the two and assume their bond covers property damage or injury claims. It doesn't. You need both, and they come from different sources: your surety bond from a bonding company, your insurance from a carrier with appetite for electrical trade risks.

Regional Risk Factors: Climate and Infrastructure in Chaves County

Extreme Heat and High-Wind Considerations for External Wiring

Roswell regularly hits 100°F or higher from June through August, and those temperatures punish outdoor electrical installations. UV degradation on exposed conduit, thermal expansion in panel boxes, and heat-related insulation breakdown all increase the likelihood of warranty callbacks and damage claims. High winds, particularly during spring dust storms, can down power lines and damage exterior-mounted equipment you've installed.

If you're doing outdoor work, whether it's parking lot lighting, signage, or rooftop solar, your policy should explicitly cover completed operations claims related to weather-induced failures. Some carriers exclude wind damage above certain thresholds, so read the fine print.

Flash Flood Risks and Subsurface Electrical Installation

The Pecos Valley is prone to flash flooding, and Roswell sits in a FEMA-designated flood zone along several arroyos. Subsurface electrical work, including underground conduit runs, landscape lighting, and well pump wiring, is particularly vulnerable. A single monsoon event can shift soil, expose buried conduit, and create ground fault conditions that lead to property damage claims months after installation.

Contractors doing subsurface work should confirm their CGL policy doesn't exclude flood-related completed operations claims. This is a coverage gap that's easy to miss and expensive to discover after the fact. Documenting installation depth, backfill materials, and drainage conditions gives you a defense if a claim arises.

Carrier Appetite and Market Trends for NM Electricians

Preferred Insurers for Residential vs. Industrial Electrical Work

Not every insurance carrier wants to write electricians, and the ones that do often have strong preferences. Residential electrical contractors with clean loss histories are the easiest to place: multiple carriers compete for this business, and premiums reflect that competition. Industrial and commercial electricians, especially those working in oil and gas or high-voltage environments, face a much smaller pool of willing underwriters.

Specialty programs like Joule Pro exist specifically because generalist agencies often can't access the markets that will write higher-risk electrical work at competitive rates. A program focused exclusively on licensed electrical contractors has underwriter relationships built around the trade's specific risk profile, which translates to better terms and fewer coverage gaps than a one-size-fits-all business owner's policy.

Impact of Claims History on Local Premium Rates

Your experience modification rate (EMR) and loss history are the two biggest factors driving your premium. A single workers' comp claim over $25,000 can increase your EMR above 1.0, which means you'll pay more than the base rate for three years. Two or more large claims in a five-year window can make you nearly uninsurable in the standard market.

Roswell electricians should request a loss run report from their current carrier annually and review it for accuracy. Incorrect or inflated claim reserves are more common than you'd think, and they directly inflate your premiums. Disputing inaccurate loss runs is one of the fastest ways to reduce your insurance costs.

Customizing Policies for Specialized Roswell Projects

Oil and Gas Industry Electrical Maintenance Coverage

Chaves County's proximity to the Permian Basin means steady demand for electricians who can handle oilfield maintenance, pump jack wiring, and SCADA system installations. This work carries higher liability limits, often $5 million or more, and requires pollution liability endorsements that standard CGL policies don't include.

If you're picking up oilfield contracts, make sure your policy includes sudden and accidental pollution coverage at minimum. Some operators require dedicated pollution liability policies with per-occurrence limits of $1 million or higher. Getting this wrong doesn't just cost you the contract: it leaves you personally exposed if a spill or contamination event traces back to your electrical work.

Solar Installation and Green Energy Endorsements

Roswell's abundant sunshine and state-level solar incentives have driven steady growth in residential and small commercial solar installations. Electricians adding solar to their service mix need to verify that their CGL policy covers solar panel installation, which some carriers classify differently than standard electrical work.

Roof-mounted solar work introduces fall exposure and potential roof damage claims that your existing policy may not adequately cover. A contractor-specific endorsement for solar installation typically adds 5% to 15% to your GL premium but closes a gap that could otherwise result in a denied claim worth tens of thousands.

Strategies for Reducing Insurance Costs and Mitigating Liability

The most effective way to lower your insurance costs in Roswell isn't shopping for the cheapest quote: it's managing the factors that drive your premium. Implement a written safety program and document it. Conduct toolbox talks weekly. Drug-test new hires. These steps directly influence your EMR and signal to underwriters that you're a lower risk.

| Strategy | Estimated Impact | Effort Level |

|---|---|---|

| Written safety program | 5-15% premium reduction | Medium |

| Annual loss run review | Varies (corrects overcharges) | Low |

| Higher deductibles | 10-20% premium reduction | Low |

| Bundling GL, auto, and inland marine | 5-10% package discount | Low |

| Clean EMR maintenance | Up to 25% below base rate | Ongoing |

Working with a specialty program like Joule Pro, backed by Fusco Orsini & Associates Insurance Services (CA Lic. 0H16057), gives you direct access to a licensed producer who understands electrical trade risks and can match you with carriers that have real appetite for your specific work type. That targeted approach beats calling three random agencies and hoping one of them knows the difference between NCCI code 5190 and 5183.

Frequently Asked Questions

Do I need insurance if I'm a sole proprietor electrician in Roswell? Yes. While New Mexico exempts sole proprietors from mandatory workers' comp, you still need general liability insurance to pull permits and work on most jobsites. Many GCs won't hire you without proof of coverage.

How much does general liability insurance cost for Roswell electricians? Expect $1,200 to $3,500 annually for a small residential operation with $1M/$2M limits. Industrial or oilfield work runs significantly higher due to increased risk.

Can I use my personal auto insurance for my work truck? No. Personal auto policies exclude commercial use. If you're hauling tools or driving to jobsites, you need a commercial auto policy or your claim will be denied.

What's the difference between a contractor's bond and liability insurance? A bond protects the public and satisfies your state licensing requirement. Insurance protects your business. You need both, and they cover completely different things.

Does my policy cover solar panel installation automatically? Not always. Some carriers classify solar work separately from standard electrical. Confirm with your agent and add a solar endorsement if needed.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.