Business Insurance

Knoxville, TN Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

Underwriting Preferences for Residential vs. Industrial Projects

Running an electrical contracting business in Knoxville means dealing with a unique mix of challenges: aging homes in historic neighborhoods like Fourth and Gill, tornado-season anxiety every spring, and a local permitting process that ties your insurance directly to your ability to pull permits. If your coverage isn't structured correctly, you're not just risking a claim denial - you're risking your license. This guide covers everything Knoxville electricians need to know about insurance, from the specific policies Tennessee requires to which carriers actually want to write your business. Whether you're a one-person residential shop or running commercial crews across Knox County, getting this right matters more than most contractors realize. The difference between a $3,000 annual premium and a $9,000 one often comes down to how well your coverage profile matches what underwriters are looking for in this market. Knoxville sits in a sweet spot for electrical work: enough new construction to keep commercial contractors busy, enough older housing stock to fuel residential rewiring demand, and enough weather events to generate steady storm-damage repair calls. That combination creates specific insurance needs that a generic business policy simply won't cover.

Essential Insurance Policies for Knoxville Electrical Contractors

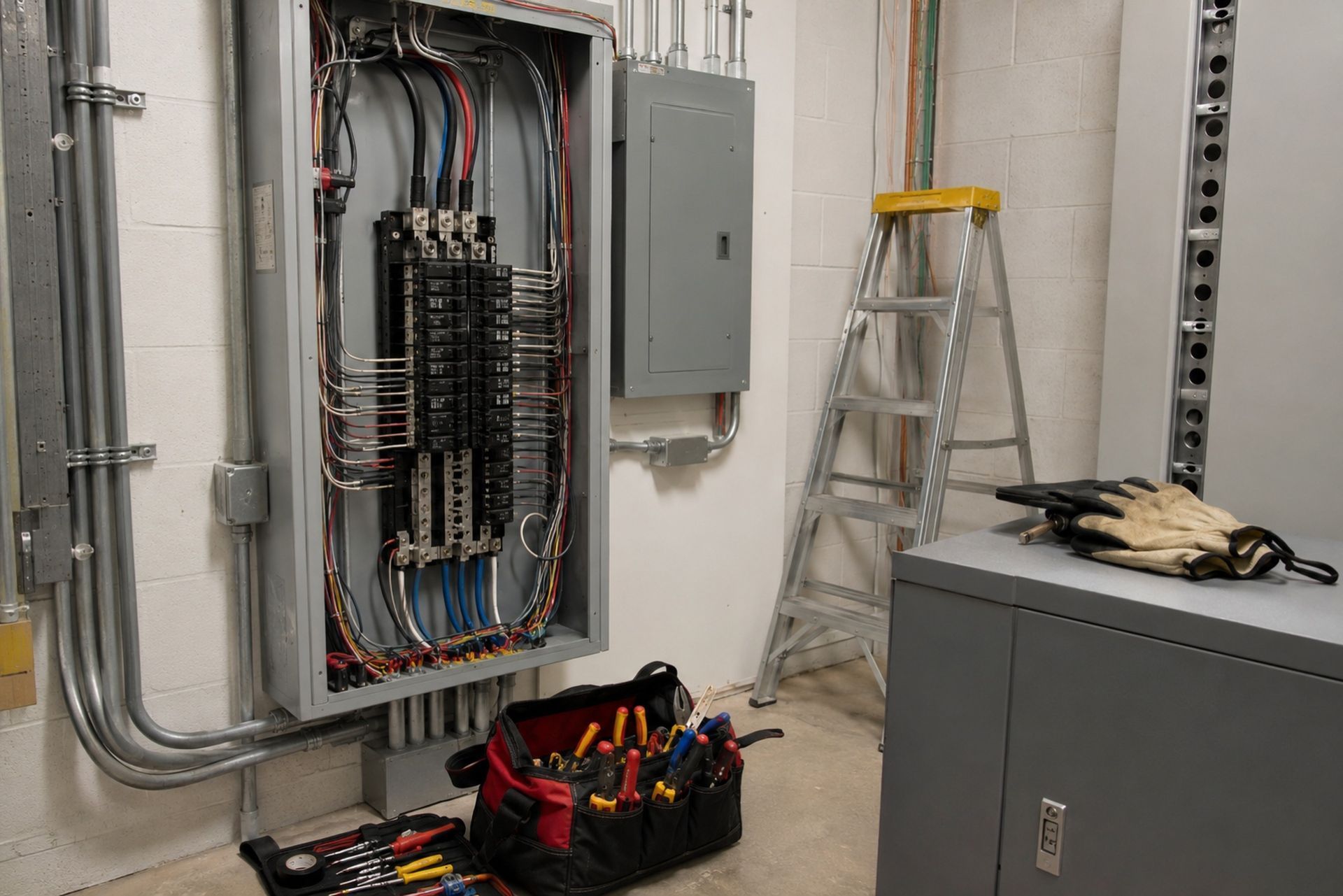

Knoxville electricians need a layered coverage approach. A single general liability policy isn't enough when you're pulling wire in a 1920s Craftsman bungalow one day and roughing in a new build off Pellissippi Parkway the next. Each type of work carries different risk profiles, and your insurance stack should reflect that.

General Liability and Property Damage Coverage

General liability is your foundation. It covers third-party bodily injury and property damage claims, which for electricians typically means things like a client tripping over your equipment, or a fire caused by faulty installation. In Knoxville, most general contractors require their electrical subs to carry at least $1 million per occurrence and $2 million aggregate before stepping onto a jobsite.

Here's where many Knoxville electricians get tripped up: completed operations coverage. Your GL policy needs to cover claims that arise after you've finished a job and left the property. A wiring defect that causes a house fire six months later is a completed operations claim, and if your policy excludes or limits that coverage, you're personally exposed. Joule Pro structures policies specifically for electrical contractors, ensuring completed operations coverage is built into the GL from the start rather than bolted on as an afterthought.

Property damage coverage also matters more than you'd think in a city where so many homes share walls, floors, and ceilings with neighbors. Condo and apartment work in downtown Knoxville means your mistake can damage multiple units simultaneously.

Workers' Compensation Requirements in Tennessee

Tennessee requires workers' compensation for any construction employer with one or more employees. That threshold is lower than many states, and it catches a lot of small Knoxville shops off guard. Even if you hire a single helper for a busy week, you technically need coverage.

The classification code for electricians (NCCI code 5190) carries a base rate in Tennessee that typically runs between $3.50 and $5.50 per $100 of payroll, depending on your experience modification factor. A clean claims history can push that mod below 1.0 and save you thousands annually. One serious injury claim can spike it above 1.5 for three years.

Independent contractor relationships get scrutinized heavily by the Tennessee Bureau of Workers' Compensation. If you're using 1099 subs who don't carry their own workers' comp, you may be liable for their injuries. This is one of the most common and expensive mistakes electrical contractors make in Knox County.

Commercial Auto and Inland Marine Protection

Your work vans and trucks need commercial auto coverage, not personal auto policies. Tennessee requires minimum liability limits of $25,000/$50,000/$15,000, but those minimums are dangerously low for a contractor hauling equipment through Knoxville traffic. Most experienced electricians carry at least $500,000 in combined single-limit coverage.

Inland marine insurance covers your tools and equipment while they're in transit or stored on a jobsite. A standard commercial property policy only covers items at your listed business location. That $15,000 wire puller sitting in your van overnight? Your commercial auto policy won't cover its theft, and your property policy won't either because it's not at your shop. Inland marine fills that gap, and for most Knoxville electricians, annual premiums run between $500 and $1,500 depending on total equipment value.

By: Michael Fusco

President of Joule Pro

INDEX

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Navigating Knoxville Permitting and Licensing Requirements

Knoxville's permitting system is tightly connected to your insurance status. The city won't issue electrical permits to contractors who can't demonstrate proper coverage, and the requirements go beyond just having a policy in hand.

City of Knoxville Electrical Permit Bonds

The City of Knoxville requires electrical contractors to maintain a surety bond before pulling permits. This bond, typically $5,000, guarantees that your work will comply with local codes. It's separate from your insurance policies but often confused with them.

Your bond must be filed with the city's Permit Center on Summit Hill Drive. If it lapses, your ability to pull permits stops immediately, and there's no grace period. Many contractors bundle their bond procurement with their insurance program. Programs like Joule Pro, which focus exclusively on electrical contractors, can coordinate bond and insurance renewals on the same timeline so nothing falls through the cracks.

You'll also need to show proof of a valid Tennessee electrical contractor license issued by the state Board for Licensing Contractors, which itself requires proof of insurance.

Aligning Coverage with Knox County Codes Administration

Knox County operates its own codes administration office separate from the City of Knoxville. If you work in unincorporated areas of the county, you'll deal with different inspectors and slightly different documentation requirements.

Both jurisdictions follow the 2023 National Electrical Code (with Tennessee amendments), but the inspection process and timeline differ. County inspections tend to have longer wait times, which means your general liability policy needs to account for extended project durations. A policy written with tight project completion windows can create coverage gaps if a county inspection delay pushes your work past the policy's expected completion date.

Keep certificates of insurance current with both jurisdictions. Expired COIs are the number one reason Knoxville-area electricians get flagged during permit reviews.

Regional Risks and Environmental Factors in East Tennessee

East Tennessee's geography and climate create insurance exposures that contractors in other parts of the state don't face to the same degree.

Mitigating Risks from Severe Weather and Seasonal Storms

Knoxville averages about 55 thunderstorm days per year, and the city sits within the secondary tornado corridor that runs through the Tennessee Valley. The March 2023 storms that damaged parts of West Knoxville are a recent reminder that severe weather isn't hypothetical here.

For electricians, storm damage creates two distinct risk scenarios. First, emergency repair work done under time pressure increases the likelihood of installation errors and resulting claims. Second, power surges from lightning strikes can damage equipment you've recently installed, leading to callbacks and potential liability disputes about whether the surge or your installation caused the failure.

Carry adequate coverage limits and consider a commercial umbrella policy that sits above your GL and auto policies. A $1 million umbrella typically costs Knoxville electricians between $400 and $800 per year, which is remarkably cheap relative to the protection it provides.

Historic District Challenges and Old Wiring Liabilities

Knoxville's historic districts, including Old North Knoxville, Fourth and Gill, and parts of South Knoxville, contain homes with knob-and-tube wiring, cloth-insulated conductors, and original fuse panels. Working on these systems carries significantly higher liability than new construction.

The risk isn't just that something goes wrong during your work. It's that existing conditions you didn't create can be attributed to you once you've touched the system. A thorough pre-work documentation process, including photos and written assessments of existing conditions, is your best defense. Your insurance carrier will want to see these records if a claim arises.

Some carriers flat-out refuse to cover electricians who do more than 30% of their work on pre-1960 structures. This is where carrier appetite becomes critical to your business model.

Understanding Carrier Appetite for Knoxville Electricians

Not every insurance company wants to write electrical contractors, and among those that do, preferences vary dramatically based on the type of electrical work you perform.

Preferred Carriers for Residential vs. Commercial Specialists

Here's a comparison of how carrier preferences typically break down for Knoxville electricians:

| FactorFactor | Residential Specialists | Commercial Specialists |

|---|---|---|

| Typical GL Premium Range | $1,800 - $4,500/year | $4,000 - $12,000/year |

| Carrier Pool Size | Larger (more carriers willing) | Smaller (fewer admitted options) |

| Key Underwriting Concern | Fire from faulty wiring | Jobsite injuries, contract disputes |

| Preferred Experience | 3+ years licensed | 5+ years with project references |

| Common Exclusion Watch | EIFS/exterior work | High-voltage/utility tie-ins |

Residential electricians generally have more carrier options because the average claim severity is lower. Commercial contractors, especially those doing industrial or high-voltage work, often need specialty markets. Joule Pro maintains underwriter relationships specifically built around electrical trade risks, which means access to carriers that understand the difference between a panel upgrade and a 480V industrial installation.

Factors Affecting Local Premiums and Risk Ratings

Your Knoxville premium is influenced by several local factors: your claims history, annual revenue, payroll size, subcontractor usage, and the specific types of electrical work you perform. Contractors who do solar installations or EV charger work may see different rates than traditional service electricians.

Knox County's relatively low cost of living compared to Nashville or Chattanooga means lower average claim payouts, which can work in your favor. But the area's growth, particularly in Hardin Valley and the Northshore corridor, means more new contractors competing for work, and carriers pay attention to how established your business is before offering preferred rates.

Strategies for Reducing Insurance Costs and Managing Claims

The most effective way to lower your insurance costs in Knoxville isn't shopping for the cheapest quote. It's building a risk profile that makes underwriters want your business.

Start with safety documentation. Maintain written safety programs, conduct regular toolbox talks, and keep records of everything. Carriers reward this behavior with lower premiums, and it protects you during claims investigations.

Bundle your policies. Packaging GL, commercial auto, inland marine, and workers' comp through a single program typically saves 10-15% compared to buying each policy separately. A specialty program designed for electricians can also identify coverage gaps that a generalist agent might miss.

Pay attention to your experience modification rate. Every workers' comp claim affects your mod for three years. Implement return-to-work programs for injured employees, because getting someone back on light duty quickly reduces claim costs and protects your mod.

Finally, review your certificates of insurance quarterly. Expired or incorrect COIs cause more permit delays and contract disputes than actual coverage problems. Set calendar reminders 60 days before each renewal.

Frequently Asked Questions

How much does general liability insurance cost for a Knoxville electrician? Most Knoxville electrical contractors pay between $1,800 and $6,000 annually for GL coverage, depending on revenue, employee count, and the type of electrical work performed.

Do I need workers' comp if I'm a sole proprietor in Tennessee? Sole proprietors with no employees can exempt themselves, but many general contractors and commercial clients require proof of workers' comp before allowing you on their jobsite.

What's the difference between a surety bond and insurance? A surety bond guarantees your work meets code requirements and protects the public. Insurance protects you and third parties from financial loss due to accidents, injuries, or property damage. You need both to pull permits in Knoxville.

Can I use my personal auto policy for my work van? No. Personal auto policies exclude vehicles used for business purposes. If you're hauling tools or driving to jobsites, you need a commercial auto policy.

How do I get a certificate of insurance for a Knoxville permit application?

Your insurance provider issues COIs on request. Programs like Joule Pro can typically generate same-day certificates, which is helpful when you need to file permits quickly.

Your Next Steps

Getting electrician insurance right in Knoxville comes down to matching your coverage to the specific work you do, the jurisdictions you work in, and the carriers that actually want your type of risk. A policy built for a general contractor won't account for completed operations exposure on old wiring, storm surge callbacks, or the bonding requirements at the Knoxville Permit Center.

If you're starting a new electrical business in Knox County or if your current coverage hasn't been reviewed in more than a year, reach out to a specialty program that understands electrical trade risks. The right coverage structure protects your license, your livelihood, and your ability to keep pulling permits in one of East Tennessee's most active markets.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.