Business Insurance

Arlington, TX Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

Underwriting Preferences for Residential vs. Industrial Projects

Running an electrical contracting business in Arlington means working in one of the fastest-growing cities in the DFW metroplex, with a construction pipeline that shows no signs of slowing down. Between the entertainment district expansions, residential subdivisions pushing into western Tarrant County, and aging commercial infrastructure needing rewiring, there's plenty of work to go around. But that growth comes with risk, and the wrong insurance setup can turn a single claim into a business-ending event. This guide covers the insurance coverage Arlington electricians actually need, how local permitting ties into your policy requirements, the city-specific hazards that affect your premiums, and which carriers have an appetite for writing electrical contractor policies in this part of North Texas. If you've been quoted sky-high premiums or had trouble finding coverage that fits your scope of work, the problem might not be your loss history. It might be that you're working with a generalist who doesn't understand how electrical trade insurance works in Tarrant County. Getting this right matters more than most contractors realize until they're staring at a claim denial letter.

Essential Insurance Policies for Arlington Electrical Contractors

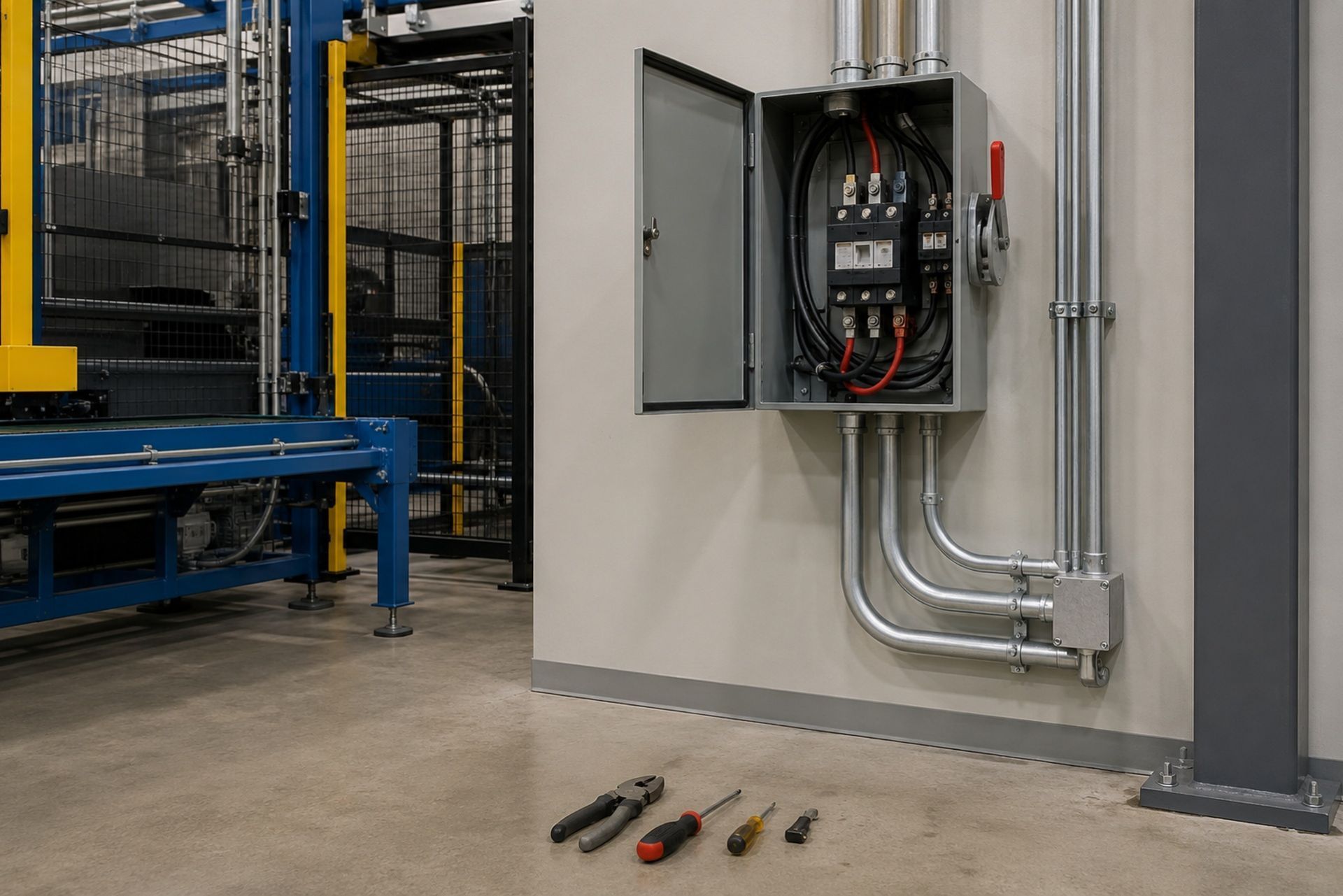

General Liability and Property Damage Coverage

General liability is the foundation of any electrician's insurance program, and in Arlington, the minimum limits most general contractors and property managers require before you set foot on a jobsite are $1 million per occurrence and $2 million aggregate. This covers third-party bodily injury and property damage claims, which for electricians often means scenarios like a faulty panel installation that causes a fire in a client's home or a tripped breaker that damages expensive equipment in a commercial facility.

What catches many Arlington electricians off guard is the completed operations exposure. Your GL policy doesn't just cover you while you're on the job; it also protects you after you leave. A wiring defect that triggers a fire six months later still falls under your policy's completed operations coverage, assuming the policy is active. This is exactly why maintaining continuous coverage without gaps matters so much. One common mistake I see is contractors dropping their GL during slow winter months to save money, only to face a claim from a summer project with no active policy in place.

Workers' Compensation Requirements in Texas

Texas is one of the few states where workers' compensation insurance isn't technically mandatory for private employers. That said, going without it in Arlington is a gamble most electricians can't afford. If you skip workers' comp and an employee gets hurt on the job, you lose the legal protections that come with being a subscriber, meaning injured workers can sue you directly for damages without the usual defenses available to employers who carry coverage.

Most GCs working on Arlington projects, especially anything near the entertainment district or in the growing residential corridors, won't let you on site without a workers' comp certificate. The Texas Department of Insurance tracks employer election status, and savvy project managers check it. For small crews of two to five electricians, expect annual premiums in the range of $4,000 to $12,000 depending on your payroll, classification codes, and experience modification rate.

Commercial Auto and Inland Marine for Tools

Your personal auto policy won't cover a work van loaded with $30,000 in tools and diagnostic equipment. Commercial auto insurance is essential for any electrician running service calls across Arlington, and your policy should include hired and non-owned auto coverage if employees ever use personal vehicles for work purposes.

Inland marine coverage, sometimes called a tools and equipment floater, protects your gear while it's in transit or stored on a jobsite. Think wire pullers, metering equipment, conduit benders, and power tools. A single van break-in at a jobsite near AT&T Stadium can wipe out thousands in equipment overnight. Joule Pro structures these policies specifically for electrical contractors, bundling inland marine with your GL and auto to avoid coverage gaps that generalist agencies often miss.

By: Michael Fusco

President of Joule Pro

INDEX

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Navigating City of Arlington Permitting and Bond Requirements

Meeting the Planning and Development Department Standards

Arlington's Planning and Development Services department handles all electrical permits, and the process runs through the Accela Citizen Access portal for online submissions. Electrical permit fees typically range from $75 to $400 depending on the scope of work, whether it's a simple residential panel upgrade or a full commercial buildout.

Here's what ties permitting to insurance: the city requires proof of valid insurance before issuing permits to contractors. If your GL policy lapses or your certificate of insurance doesn't match the entity name on your contractor registration, you'll hit delays. I've seen Arlington electricians lose weeks on projects because their insurance agent issued a certificate with the wrong named insured or forgot to list the city as an additional insured when required.

Contractor Registration and License Bonds

Arlington requires electrical contractors to register with the city and maintain a valid Texas Electrical License issued through the Texas Department of Licensing and Regulation. Part of that registration process involves posting a contractor license bond, which functions differently from insurance but is often confused with it.

A license bond protects the public if you fail to follow code or complete contracted work. It doesn't protect you. Your insurance policies handle that. Bond amounts for electrical contractors in Arlington typically run between $5,000 and $15,000, and the annual premium you pay is a fraction of the bond face value, usually 1% to 3% for contractors with decent credit. Keep your bond and insurance documents organized together because you'll need both every time you renew your city registration.

Local Risk Factors Unique to the Arlington Market

Severe Weather and Storm-Related Electrical Hazards

North Texas averages around 50 to 60 thunderstorm days per year, and Arlington sits squarely in the heart of tornado alley. For electricians, this means two things: a surge in demand for storm damage repair work and an elevated risk profile that insurers pay close attention to. Lightning strikes, hail damage to exterior electrical components, and wind-driven debris that compromises service entrances are all common claims in the Arlington market.

Carriers pricing electrician insurance in this region factor in the severe weather patterns across North Texas, and that shows up in your premiums. If you do a lot of storm restoration work, your underwriter will want to know about it during the application process. Being upfront about your mix of new construction versus repair work helps avoid mid-term audits that result in surprise additional premiums.

High-Density Commercial Projects Near Entertainment Districts

Arlington's entertainment district, anchored by AT&T Stadium, Globe Life Field, and the expanding Texas Live! complex, generates a constant flow of commercial electrical work. These projects carry higher liability limits, often $5 million or more in umbrella coverage, and involve working in occupied spaces with significant foot traffic.

The risk profile for electricians working on these high-density commercial projects is substantially different from residential service work. You're dealing with tighter timelines, more subcontractor coordination, and a higher probability of third-party injury claims. Your insurance program needs to reflect that reality. A policy designed for residential service electricians won't hold up when a GC on a stadium renovation project reviews your coverage.

Carrier Appetite and Finding the Right Insurer in Tarrant County

Preferred Carriers for Residential vs. Industrial Electricians

Not every insurance carrier wants to write electrician policies, and the ones that do often have very specific preferences. Some carriers focus exclusively on residential electricians with clean loss histories and small crews. Others have appetite for larger industrial and commercial operations but require higher minimum premiums.

| Factor | Residential-Focused Carriers | Commercial/Industrial Carriers |

|---|---|---|

| Typical Crew Size | 1-5 employees | 5-50+ employees |

| Minimum Premium | $2,500-$5,000 | $10,000-$25,000+ |

| Preferred Revenue Range | Under $500K | $500K-$5M+ |

| Common Exclusions | High-voltage, solar | Handyman, side work |

| Umbrella Availability | $1M-$2M typical | $5M-$10M available |

Joule Pro maintains relationships with specialty carriers that specifically underwrite electrical contractor risks, which means faster quoting and fewer declinations compared to working with a generalist agent who submits your application to carriers that don't have appetite for your class code.

Factors Influencing Premium Costs in North Texas

Your premium isn't just about your loss history. In the Arlington and greater Tarrant County market, several factors push costs up or down:

- Years in business and continuous insurance history (gaps kill your pricing)

- Employee count and total payroll for workers' comp rating

- Revenue mix between residential, commercial, and industrial work

- Whether you perform high-voltage or solar installation work

- Your experience modification rate for workers' comp

- Claims history over the past five years, even small ones

Electricians who maintain clean loss runs and carry continuous coverage typically see renewal increases of 3% to 7% annually in this market. Those with claims or coverage gaps can face 20% or higher jumps, or outright non-renewal.

Steps to Secure and Maintain Compliant Coverage

Getting properly insured as an Arlington electrician isn't a one-time event. It's an annual cycle that requires attention. Start by gathering your current loss runs, payroll records, and a clear description of your scope of work. If you're a new contractor, have your TDLR license number and business formation documents ready.

- Request quotes from a specialty program like Joule Pro that understands electrical trade classifications

- Review policy forms carefully, paying attention to exclusions for solar, high-voltage, or EIFS work

- Ensure your certificates of insurance match your Arlington contractor registration exactly

- Set calendar reminders 60 days before renewal to avoid lapses

- Report claims immediately and maintain open communication with your adjuster

One thing to keep in mind: your insurance needs will change as your business grows. Adding a crew member, taking on a commercial project, or purchasing a new service van all require policy updates. Don't wait until renewal to make these changes because a gap in coverage during a claim is the most expensive mistake you can make.

Frequently Asked Questions

Do I need insurance to pull an electrical permit in Arlington? Yes. The City of Arlington requires proof of valid insurance and contractor registration before issuing electrical permits through their online portal.

Is workers' comp required for electricians in Texas? Not legally required for private employers, but most general contractors and project owners in Arlington mandate it before allowing you on site.

How much does general liability insurance cost for an Arlington electrician? Expect $2,500 to $8,000 annually for a small residential operation. Commercial electricians with larger crews can pay $10,000 to $25,000 or more depending on revenue and risk profile.

What's the difference between a license bond and insurance? A license bond protects the public if you violate codes or fail to complete work. Insurance protects your business from liability claims and property damage.

Can I bundle my electrician insurance policies?

Yes, and you should. Bundling GL, workers' comp, commercial auto, and inland marine through a single specialty program avoids coverage gaps and often reduces total cost.

Anyone who drives in Chattanooga knows that the I-24/I-75 interchange and the Ridge Cut are among the most accident-prone stretches of highway in Tennessee. Commercial auto insurance is essential for any electrician running service vehicles through this corridor daily. The I-24 corridor through Chattanooga has historically high accident rates, and your premiums will reflect that.

Commercial auto covers your vehicles, but also liability for accidents your drivers cause. If a technician rear-ends someone on the I-24 split during morning traffic, your commercial auto policy responds. Make sure your policy includes hired and non-owned auto coverage if employees ever use personal vehicles for work errands.

Telematics and dash cameras can help reduce premiums over time by demonstrating safe driving habits. Some carriers offer discounts of 5-15% for fleets that use GPS tracking and driver monitoring systems.

Underwriters look at three things above all else: how long you've been in business, your safety record, and your claims history over the past five years. A clean loss run is the single most powerful tool you have for getting competitive quotes. If you've had claims, be prepared to explain what corrective actions you took.

Your EMR matters enormously for workers' comp pricing. An EMR below 1.0 signals that you're safer than average and earns you premium credits. An EMR above 1.2 can make it difficult to find standard market coverage at all, pushing you into surplus lines where premiums are higher.

Tennessee-specific factors also play a role. Carriers look at whether you're doing residential rewiring in older homes versus new construction, whether you handle any high-voltage utility work, and whether you subcontract portions of your jobs.

Making the Right Choice for Your Arlington Business

The right insurance setup protects more than your balance sheet. It keeps you eligible for permits, qualifies you for better projects, and gives general contractors confidence in hiring your crew. Arlington's growth trajectory means more opportunity for electricians, but only for those who can meet the insurance and bonding requirements that come with it. If your current agent doesn't specialize in electrical contractor insurance, you're likely overpaying or underinsured, possibly both. Reach out to a specialty program that knows the electrical trade inside and out, and get a coverage review before your next renewal.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.