Business Insurance

El Paso, TX Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

El Paso sits at a unique crossroads: a booming border economy, extreme desert conditions, and a construction market that keeps electrical contractors busy year-round. But running an electrical business here means dealing with risks that contractors in Dallas or Houston simply don't face. Between flash floods ripping through arroyos, 110-degree heat frying outdoor panels, and the specific permitting requirements the city enforces, getting the right insurance coverage isn't optional - it's survival. This guide covers everything El Paso electricians need to know about protecting their business, from local licensing and bonding rules to which insurance carriers actually want to write policies in West Texas. If you've been quoted sky-high premiums or turned down by generalist agents who don't understand your trade, you're not alone. The electrical contracting insurance market in this region has its own quirks, and understanding them gives you a real advantage.

Navigating the El Paso Electrical Contracting Landscape

El Paso's electrical contracting market has grown steadily alongside the city's population, which now exceeds 700,000. Military installations like Fort Bliss, cross-border manufacturing support facilities, and a residential housing market that shows no signs of slowing all contribute to demand. But before you can bid on a single job, you need to clear two distinct regulatory hurdles: state licensing through TDLR and local permitting through the City of El Paso.

Texas Department of Licensing and Regulation (TDLR) Requirements

Every electrician working in Texas must hold a valid license issued by TDLR. This applies whether you're a master electrician running your own shop, a journeyman working under someone else's license, or an apprentice logging hours toward certification. Texas requires master electricians to carry at least $25,000 in general liability insurance as a condition of licensure.

One major change hitting the industry this year: Texas will

officially adopt the 2026 National Electrical Code (NEC) effective September 1, 2026, which introduces stricter requirements for arc-fault protection, surge protection, and energy storage system installations. If you're doing any work with battery backup systems or solar tie-ins - increasingly common in El Paso's sun-drenched market - these code updates directly affect your scope of work and your risk profile. Insurers pay attention to code compliance, and violations discovered after a claim can lead to coverage disputes.

El Paso Planning and Inspections: Permitting and Bond Requirements

The City of El Paso requires electrical contractors to register with the Planning and Inspections Department before pulling permits. You'll need to show proof of your TDLR license, a surety bond (typically $10,000 for electrical contractors), and current certificates of insurance. The city's permitting portal has been fully digital since 2024, which speeds things up but also means your documentation needs to be current at all times.

Permit fees in El Paso vary by project scope. A simple residential service upgrade might cost $75-$150 in permit fees, while a commercial tenant improvement can run $500 or more. The key thing contractors miss: your insurance certificates must name the City of El Paso as an additional insured on certain commercial and municipal projects. If your agent can't turn around certificate requests quickly, you lose jobs. Programs like Joule Pro, which focus exclusively on electrical contractors, handle these certificate requests routinely because they understand the urgency.

By: Michael Fusco

President of Joule Pro

INDEX

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Essential Insurance Coverages for El Paso Electricians

General Liability: Protecting Against Property Damage and Bodily Injury

General liability is the foundation of your coverage stack. It protects you when a customer trips over your tool bag, when a wire you installed causes a fire six months later, or when your work damages someone else's property. For El Paso electricians, the most common GL claims involve completed operations - meaning something goes wrong after you've finished the job and left the site.

A typical GL policy for a small residential electrical contractor in El Paso runs between $1,200 and $3,500 annually for $1M/$2M limits. Commercial contractors doing panel upgrades, industrial wiring, or fire alarm installations will pay more, often $4,000 to $8,000 depending on revenue and payroll. The completed operations coverage within your GL policy is arguably the most important piece, since electrical failures often manifest weeks or months after installation.

Workers' Compensation in the Borderplex Region

Texas is one of the few states where workers' compensation isn't technically mandatory for private employers. That said, going without it in El Paso is a terrible idea. General contractors on nearly every commercial project require subs to carry workers' comp before stepping on site. The Borderplex region's construction boom means GCs are strict about compliance - no cert, no work.

Workers' comp rates for electricians in Texas are classified under NCCI code 5190, and the base rate typically falls between $3.50 and $5.50 per $100 of payroll. Your experience modification rate (EMR) can push that number up or down significantly. One serious injury claim can spike your EMR for three years, so investing in safety training and proper PPE pays dividends beyond just keeping your crew safe.

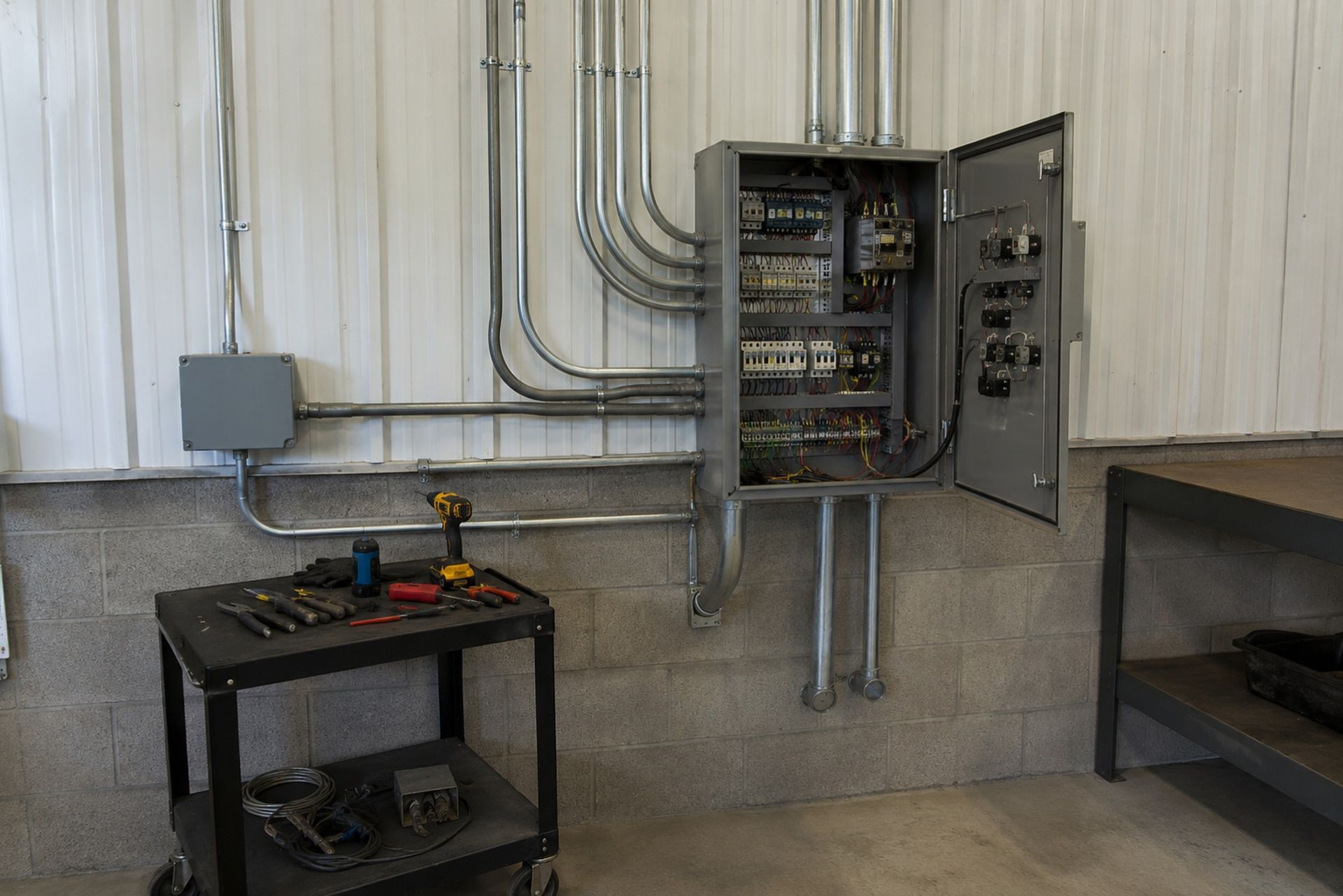

Commercial Auto and Inland Marine for Tool Protection

Your work vans and the tools inside them represent a significant investment. A fully loaded service van can easily carry $15,000-$30,000 worth of wire, meters, benders, and specialty equipment. Standard commercial auto policies cover the vehicle itself but not the tools and equipment inside. That's where inland marine coverage fills the gap.

| Coverage Type | What It Covers | Typical Annual Cost (El Paso) |

|---|---|---|

| Commercial Auto | Vehicle damage, liability while driving | $1,800 - $4,500 per vehicle |

| Inland Marine / Tools | Tools, equipment, materials in transit or on-site | $300 - $1,200 |

| General Liability | Third-party injury, property damage, completed ops | $1,200 - $8,000 |

| Workers' Comp | Employee injuries on the job | Varies by payroll and EMR |

Theft from work vehicles is a real problem in El Paso, particularly in areas near the border and on job sites without overnight security. An inland marine policy covers your tools whether they're in the van, at a job site, or in your shop. Joule Pro bundles these coverages into a single contractor-focused program, which simplifies the process and often results in better pricing than buying each policy separately from different carriers.

City-Specific Risks and Environmental Hazards

Extreme Heat and Arid Climate Electrical Failures

El Paso regularly sees 30 or more days above 100°F each summer. That kind of sustained heat accelerates the degradation of wire insulation, causes thermal expansion in conduit, and puts enormous stress on HVAC electrical systems. Electricians working outdoors face heat illness risks that directly affect workers' comp claims frequency.

From an insurance perspective, the heat creates a higher incidence of completed operations claims. Connections that test fine during installation can fail when ambient temperatures push components past their rated thresholds. Using materials rated for high-temperature environments and documenting your material choices protects you both legally and from an insurance standpoint if a claim arises.

Monsoon Season and Flash Flood Mitigation

The North American Monsoon brings intense, short-duration storms to El Paso from June through September. Flash flooding is a serious hazard in the region's arroyo system, and water intrusion into electrical panels, underground conduit, and outdoor junction boxes causes significant damage annually. Contractors who install outdoor electrical systems need to account for these conditions.

Water damage claims spike during monsoon season. If you're installing exterior panels, EV charging stations, or landscape lighting, proper weatherproofing and elevation above flood-prone grades aren't just best practices - they're your defense against negligence claims. Documenting your installation methods with photos and keeping records of material specifications gives your insurer something to work with if a claim comes in.

Carrier Appetite and Market Trends in West Texas

Preferred Carriers for Residential vs. Commercial Contractors

Not every insurance company wants to write policies for electricians, and even fewer are comfortable with West Texas risks. Carrier appetite - meaning which insurers actively seek electrical contractor business - varies significantly based on your specialty.

Residential electricians doing service calls, panel upgrades, and new construction wiring generally have the easiest time finding coverage. Several admitted carriers write these risks competitively. Commercial and industrial electricians, especially those working on high-voltage systems, fire alarm installations, or solar/battery storage projects, often need surplus lines carriers willing to underwrite more complex risk profiles.

Specialty programs like Joule Pro maintain relationships with underwriters who specifically focus on electrical trade risks. This matters because a generalist agent shopping your policy to carriers unfamiliar with electrical work often gets declinations or inflated quotes. A program built for electricians knows which carriers have appetite for your specific type of work.

Factors Influencing Premiums in the 915 Area Code

Several factors make El Paso premiums different from the Texas average. The city's proximity to the border creates unique auto liability considerations, since cross-border travel and higher uninsured motorist rates affect commercial auto pricing. The extreme climate conditions discussed earlier also factor into underwriting decisions.

Your premium is primarily driven by annual revenue, payroll, number of employees, type of work performed, and claims history. Contractors with clean loss runs for three or more years can often negotiate premium credits. Those with recent claims - especially fire-related or water damage claims - will see surcharges. Keeping detailed safety records and investing in continuing education for your crew signals to underwriters that you're a lower risk.

Best Practices for Risk Management and Policy Maintenance

Strong risk management does more than prevent accidents - it directly lowers your insurance costs over time. Here are practices that make a measurable difference:

- Review your policy annually, not just at renewal. Revenue changes, new employees, and additional vehicles all need to be reported mid-term to avoid coverage gaps.

- Maintain a written safety program. OSHA compliance isn't just about avoiding fines; insurers use it as an underwriting factor.

- Document every job with photos, especially completed work. This is your best defense in a completed operations claim.

- Keep your TDLR license and city registration current. A lapsed license can void coverage.

- Request loss run reports from your current carrier six months before renewal so you have time to address any issues.

Training your crew on the 2026 NEC changes before the September 1 effective date is also smart risk management. Code violations discovered during a claim investigation give insurers grounds to dispute coverage, and that's a situation no contractor wants to face.

Your Next Steps

Getting the right insurance coverage for your El Paso electrical contracting business isn't about finding the cheapest policy - it's about finding coverage that actually responds when you need it. The combination of extreme heat, monsoon flooding, evolving code requirements, and a competitive construction market means you need an insurance partner who understands electrical trade risks specifically.

If your current agent struggles to explain the difference between occurrence and claims-made triggers, or can't get you a certificate of insurance within 24 hours, it might be time to talk to a specialist. Joule Pro, backed by Fusco Orsini & Associates Insurance Services (CA Lic. 0H16057, NPN 15979499), works exclusively with licensed electrical contractors and can put together a coverage program tailored to El Paso's unique conditions. Reach out for a quote and see what a trade-focused program can do for your bottom line.

Not every insurance carrier wants to write electrical contractor risks in South Florida. The combination of hurricane exposure, active litigation, and high claim severity makes many national carriers cautious. Carrier appetite - meaning which insurers are willing to write your specific type of work in your specific geography - varies significantly between residential and commercial electricians.

Residential electricians typically find more carrier options because the per-project exposure is lower. Commercial electricians, especially those working on high-rises, hospitals, or large-scale renovations, face a tighter market. Specialty carriers and surplus lines markets often provide the best options for commercial electrical contractors in Miami. The key is working with a producer who has established relationships with these specialty markets and can match your risk profile to the right carrier.

Frequently Asked Questions

Is workers' compensation required for electricians in Texas? No, Texas doesn't mandate workers' comp for private employers. But nearly every general contractor requires it from subs, and going without it exposes you to personal liability lawsuits with no cap on damages.

How much does general liability insurance cost for El Paso electricians? Expect $1,200 to $3,500 annually for small residential operations and $4,000 to $8,000 for commercial contractors, based on $1M/$2M policy limits.

Do I need a separate policy to cover my tools? Yes. Commercial auto covers the vehicle, not what's inside it. Inland marine coverage protects your tools and equipment whether they're in the van, at a job site, or in storage.

Will the 2026 NEC changes affect my insurance? They can. Stricter code requirements for arc-fault protection and energy storage systems change your risk profile. Insurers may adjust premiums or require documentation of code compliance.

What does "carrier appetite" mean? It refers to which insurance companies actively want to write policies for your type of work. Not all carriers are comfortable insuring electricians, especially those doing commercial or high-voltage work.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.