Business Insurance

Laredo, TX Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

Underwriting Preferences for Residential vs. Industrial Projects

Running an electrical contracting business in Laredo means dealing with a unique set of challenges that electricians in Dallas or Houston simply don't face. The extreme South Texas heat, proximity to the Mexican border, and a construction market shaped by international trade logistics all create risk profiles that generic insurance programs weren't designed to handle. If you're a licensed electrician operating in Webb County, your insurance needs to reflect the reality of working in a border city where summer temperatures routinely exceed 110°F, where commercial projects tied to cross-border warehousing are booming, and where the City of Laredo has its own permitting and bonding requirements that differ from state minimums. This guide covers the essential insurance policies Laredo electricians need, the city-specific risks that affect your premiums, local permitting mandates, and which carriers actually want to write policies for electrical contractors in this market. Whether you're a solo operator pulling permits for residential panel upgrades or running crews on industrial projects near the World Trade Bridge, the right coverage structure can mean the difference between surviving a claim and shutting your doors.

Essential Insurance Policies for Laredo Electrical Contractors

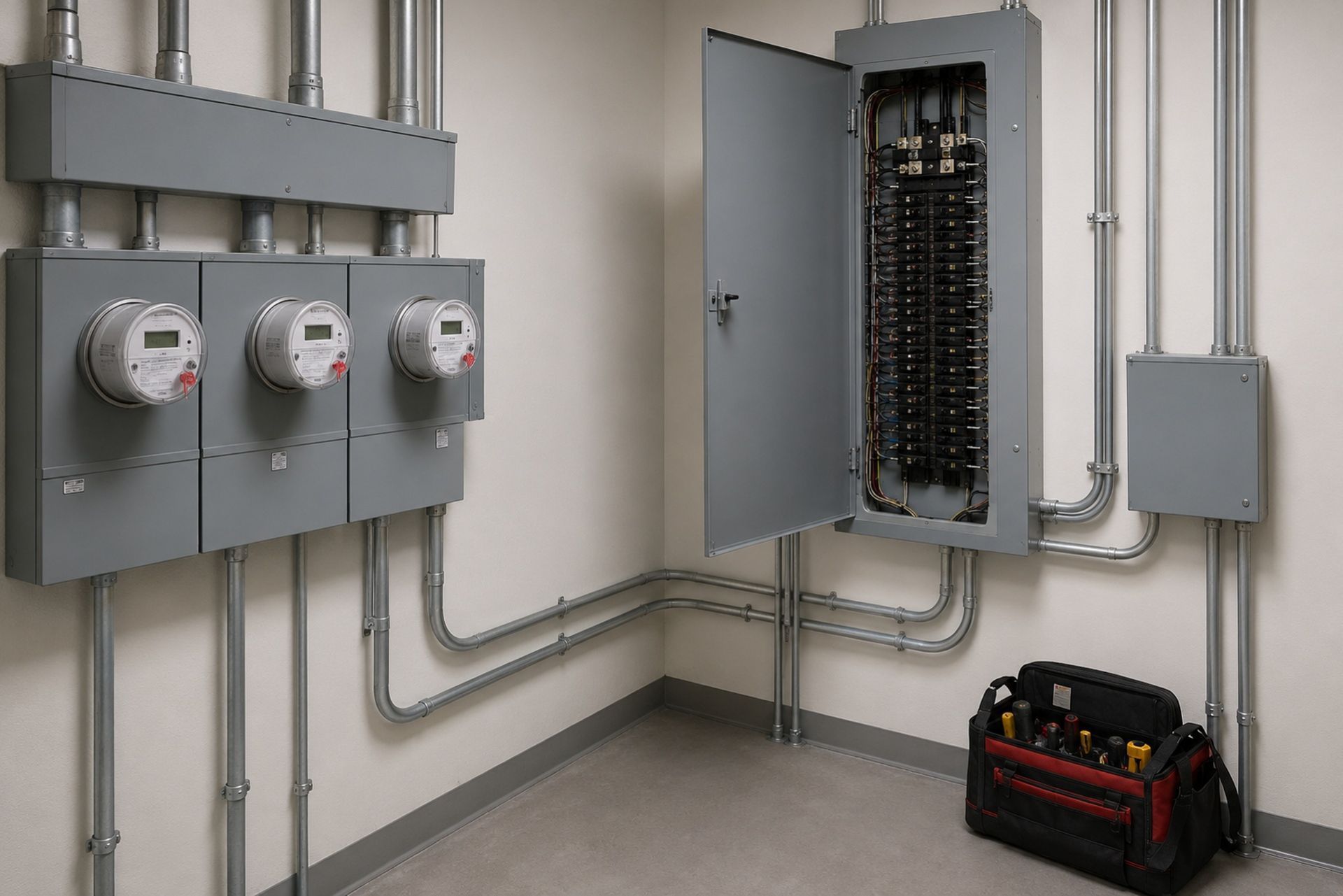

General Liability and Property Damage Coverage

General liability (GL) is the foundation of every electrician's insurance program, and in Laredo, it's non-negotiable for pulling permits. A standard GL policy covers third-party bodily injury, property damage, and completed operations claims. That last piece matters more than most electricians realize: if faulty wiring causes a fire six months after you finish a job, your completed operations coverage is what responds.

For Laredo electricians, GL limits of $1 million per occurrence and $2 million aggregate are standard, though commercial and industrial projects often require higher limits. Umbrella policies can extend your coverage to $5 million or more without dramatically increasing your premium. One thing to keep in mind: lockout/tagout violations have surged by 29% recently, making them a leading cause of catastrophic claims for industrial electricians. If you're working on energized equipment at any of Laredo's warehouse or manufacturing facilities, your GL policy needs to be airtight.

Texas Workers' Compensation Requirements

Texas is one of the few states where workers' compensation insurance isn't legally mandatory for private employers. That said, going without it is a gamble most Laredo electrical contractors can't afford. Without workers' comp, you lose your protection under the Texas Workers' Compensation Act, meaning injured employees can sue you directly for damages with no cap on what a jury might award.

Most general contractors in Laredo require subcontractors to carry workers' comp before stepping on a jobsite. If you're bidding on commercial projects, especially the warehouse and logistics facilities popping up along I-35, you'll be asked for a certificate of insurance showing active workers' comp coverage. Texas rates for electricians typically fall under class code 5190, and your experience modification rate (EMR) plays a huge role in what you actually pay.

Commercial Auto and Inland Marine for Tool Protection

Your work trucks and the tools inside them represent a significant investment. Commercial auto insurance covers your vehicles while they're on the road, but here's the gap most electricians miss: a standard auto policy won't cover the $15,000 worth of meters, benders, and power tools sitting in the bed of your truck.

That's where inland marine coverage comes in. Inland marine protects tools, equipment, and materials in transit or stored at jobsites. In Laredo, where tool theft from vehicles and jobsites remains a persistent problem, this coverage pays for itself fast. A typical inland marine policy for an electrical contractor runs $500 to $1,500 annually depending on the value of your equipment, a small price compared to replacing a full loadout of Fluke meters and Milwaukee power tools.

By: Michael Fusco

President of Joule Pro

INDEX

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Navigating Laredo Permitting and City Bonding Requirements

City of Laredo Electrical Permit Insurance Mandates

The City of Laredo requires electrical contractors to carry valid insurance before issuing permits. You'll need to provide proof of general liability coverage, and the city typically requires a minimum of $300,000 in coverage, though most contractors carry far more. Your insurance certificate must name the City of Laredo as an additional insured on permitted projects.

Laredo's Building Development Services Department handles electrical permit applications, and they've tightened enforcement over the past two years. Expired certificates or policies with lapsed coverage will stall your permit approval, costing you time and potentially losing you jobs. Keeping your certificates current and having your agent issue updated copies promptly is a small administrative task that prevents real headaches.

Surety Bonds vs. Liability Insurance for Local Compliance

Contractors in Laredo often confuse surety bonds with liability insurance, but they serve completely different purposes. A surety bond guarantees you'll comply with local codes and regulations. If you don't, the bond pays the city or the affected party, and then the bonding company comes after you for reimbursement. Liability insurance, on the other hand, protects you from third-party claims.

Laredo requires electrical contractors to maintain a surety bond as part of the licensing process. The bond amount varies, but typical requirements for electrical contractors range from $5,000 to $25,000. You'll need both the bond and active liability insurance to maintain your license and pull permits. Programs like Joule Pro, which specialize in electrical contractor coverage, can help coordinate both requirements through a single point of contact rather than forcing you to deal with separate bond and insurance brokers.

Addressing Laredo-Specific Environmental and Operational Risks

Extreme Heat and Weather-Related Site Hazards

Laredo regularly ranks among the hottest cities in the United States. Summer temperatures frequently exceed 110°F, and electricians working on rooftops, in attics, or inside un-air-conditioned new construction face serious heat-related health risks. Heat exhaustion and heat stroke claims are a real concern for workers' comp carriers evaluating Laredo-based contractors.

Your safety program directly affects your insurability and your premiums. Carriers want to see documented heat illness prevention plans, mandatory water breaks, and buddy systems for crews working in extreme conditions. Beyond the human cost, a single heat stroke claim can spike your EMR and increase your workers' comp premiums for three years. Investing in cooling vests, shade structures, and adjusted work schedules during peak summer months isn't just good practice: it's a financial decision that affects your bottom line.

Severe weather also plays a role. While Laredo doesn't see hurricanes like coastal Texas cities, flash flooding during monsoon season can damage equipment stored at ground-level jobsites and delay projects. Your inland marine and commercial property policies should account for flood exposure.

Border Region Logistics and Cross-Jurisdictional Risks

Laredo's position as the largest inland port in the United States creates unique opportunities and risks for electricians. The city's economy is heavily tied to international trade, and many electrical projects involve warehouse facilities, cold storage buildings, and logistics hubs that serve cross-border commerce.

If your work takes you across the border into Nuevo Laredo or other Mexican municipalities, your standard U.S. insurance policies won't cover you. You'd need separate Mexican liability and auto coverage. Even if you never cross the border yourself, subcontracting arrangements with companies that operate on both sides can create liability exposure you might not anticipate. Clarify these boundaries with your insurance provider before accepting any project with a cross-border component.

Carrier Appetite and Market Trends in Webb County

Preferred Insurance Carriers for South Texas Trades

Not every insurance carrier wants to write policies for electricians in South Texas. Carrier appetite, the willingness of an insurer to take on a specific type of risk, varies significantly by geography and trade classification. Some national carriers have pulled back from the Texas border region entirely due to higher-than-average claim frequency in the construction sector.

The carriers that do write electrician insurance in Webb County tend to be specialty or surplus lines markets with experience pricing trade-specific risks. Programs like Joule Pro maintain relationships with these underwriters specifically because they understand electrical contractor operations. Working with a specialty program means your application lands on the desk of an underwriter who knows the difference between a residential service electrician and a high-voltage industrial contractor, and prices accordingly.

Factors Influencing Premium Rates in the Laredo Market

Several factors push Laredo premiums higher than the state average for electrical contractors:

| Factor | Impact on Premiums | What You Can Control |

|---|---|---|

| Extreme heat exposure | Increases workers' comp rates | Safety programs, adjusted schedules |

| Border region classification | Higher GL base rates | Clean claims history |

| Vehicle theft rates | Higher commercial auto premiums | GPS tracking, secured parking |

| Project type mix | Industrial work costs more to insure | Accurate class code reporting |

| EMR score | Multiplier on workers' comp base rate | Injury prevention, return-to-work programs |

Your claims history is the single biggest lever you have. A three-year clean record can reduce your premiums by 15-25% compared to a contractor with even one significant claim.

Strategic Risk Management and Policy Procurement

Bundling Coverages for Commercial and Residential Electricians

Purchasing your GL, commercial auto, inland marine, and workers' comp through a single program typically saves 10-20% compared to buying each policy separately. A Business Owner's Policy (BOP) bundles GL with commercial property coverage and often includes business interruption insurance.

For Laredo electricians doing both residential and commercial work, make sure your policy classifications reflect your actual revenue split. Misclassifying your work mix is one of the most common audit surprises contractors face. If you reported 80% residential but actually performed 60% commercial work, your year-end audit will result in additional premium charges that can strain cash flow. Joule Pro's direct producer access means a licensed insurance professional reviews your classifications annually, catching these discrepancies before they become expensive surprises.

Annual Policy Audits and Growth-Based Adjustments

Your insurance needs change as your business grows. Adding employees, purchasing new vehicles, expanding into industrial work, or taking on larger projects all affect your coverage requirements. An annual policy review should examine your payroll projections (which drive workers' comp premiums), your vehicle schedule, your equipment values, and your contract requirements.

Don't wait for renewal to update your policies. If you hire three new journeymen mid-year and don't report the payroll increase, your audit will catch it, and you'll owe back premium plus potential penalties. Proactive reporting keeps your coverage accurate and avoids cash flow surprises at audit time.

Frequently Asked Questions

How much does general liability insurance cost for electricians in Laredo? Most Laredo electricians pay between $2,500 and $6,000 annually for a $1M/$2M GL policy. Your exact rate depends on revenue, project types, and claims history.

Do I need workers' comp insurance in Texas? Texas doesn't require it for private employers, but most general contractors and project owners mandate it before you can work on their sites. Going without it exposes you to unlimited personal liability.

Can my U.S. insurance cover work in Mexico? No. Standard U.S. policies exclude coverage outside the country. You'd need separate Mexican insurance for any work performed across the border.

What's the difference between a surety bond and liability insurance? A surety bond guarantees your compliance with local codes and protects the city or client. Liability insurance protects you from third-party injury and property damage claims. You need both in Laredo.

How does my EMR affect my premiums?

Your Experience Modification Rate is a multiplier applied to your workers' comp base rate. An EMR below 1.0 means you're safer than average and pay less. Above 1.0, and you're paying a penalty.

Your Next Steps

Getting the right insurance coverage for your Laredo electrical contracting business isn't about finding the cheapest policy: it's about building a coverage structure that matches how and where you actually work. The combination of extreme heat, border-region risk factors, and local permitting requirements means your insurance program needs to be specific to your operations. Work with a specialty program that understands electrical contractor risks, review your policies annually, and keep your safety documentation current. If you're looking for a coverage review tailored specifically to licensed electricians, reach out to Joule Pro for a consultation with a licensed insurance professional who handles electrical contractor policies every day.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.