Business Insurance

Rochester, NY Electrician Insurance

★★★★★ 150+ Five-Star Reviews · Google & Facebook

Underwriting Preferences for Residential vs. Industrial Projects

Rochester's electrical contractors face a unique mix of challenges: brutal winters, aging housing stock dating back a century or more, and a city permitting process that demands specific insurance documentation before you can pull a single wire. If you're running an electrical business in Monroe County, getting your insurance coverage right isn't just about checking a box. It's the difference between surviving a bad claim and shutting your doors. This guide to electrician insurance in Rochester, NY covers the coverage types you need, the local permitting requirements that trip people up, the risks specific to Western New York, and which carriers actually want to write policies for electrical contractors in this market. Whether you're a one-truck residential shop or a commercial outfit with twenty employees, the details here should save you time, money, and headaches.

Essential Insurance Policies for Rochester Electrical Contractors

General Liability and Property Damage for Job Sites

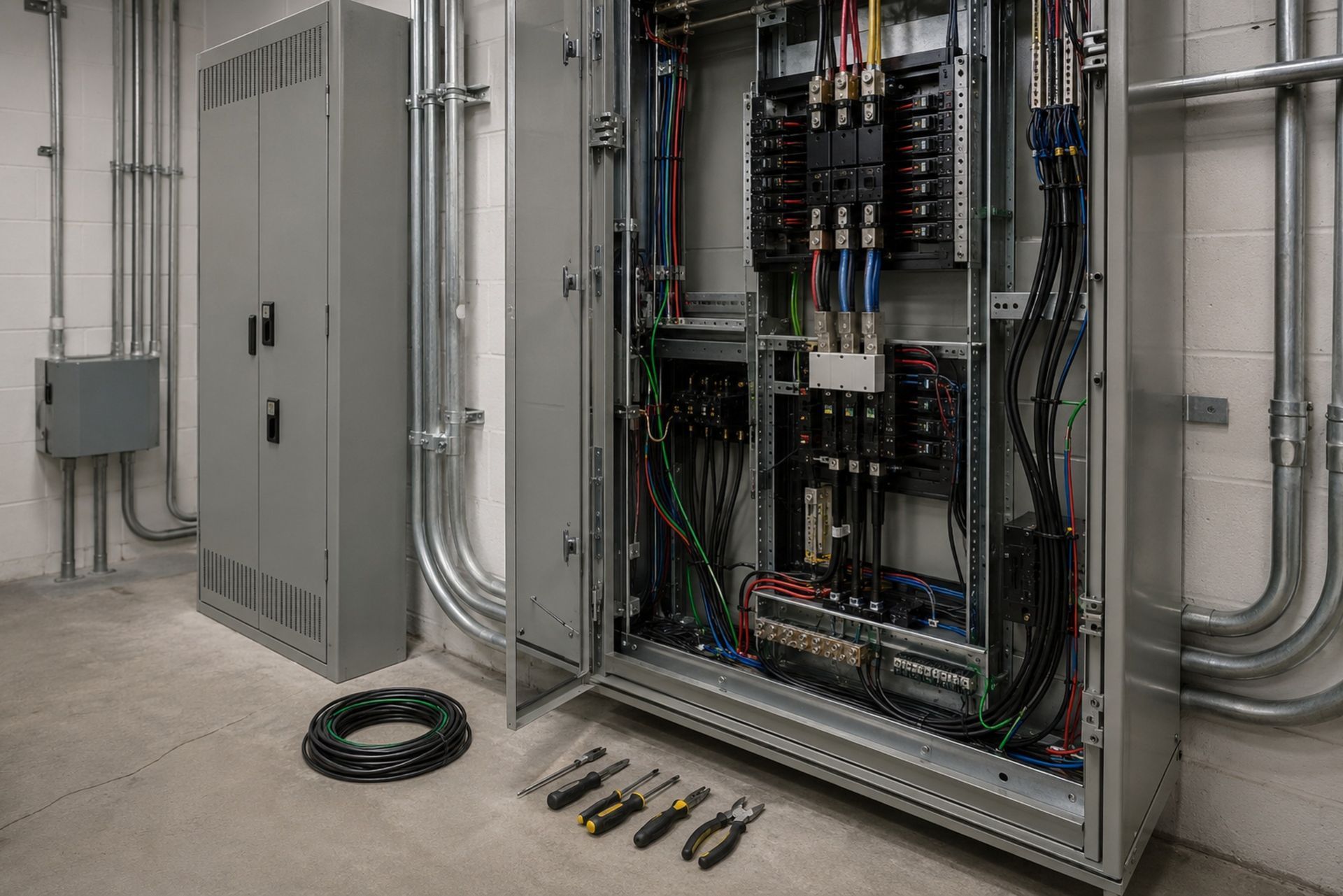

General liability is the foundation of every electrical contractor's insurance program, and in Rochester, it carries extra weight. The city's mix of older residential neighborhoods like Park Avenue and South Wedge, combined with commercial renovation projects downtown, means you're frequently working in buildings where one mistake can cause significant property damage.

A standard GL policy covers third-party bodily injury and property damage claims. Think: a homeowner trips over your cord and breaks a wrist, or you accidentally damage a client's finished hardwood floor while running conduit. Most Rochester general contractors and property managers require $1 million per occurrence and $2 million aggregate before they'll let you on site.

One thing many Rochester electricians overlook is completed operations coverage within their GL policy. If a panel you installed causes a fire six months after the job is done, this is the coverage that responds. Given the age of Rochester's building stock, where you're often tying new work into decades-old wiring, completed operations claims are more common than you'd expect.

NYS Workers' Compensation and Disability Requirements

New York State does not mess around with workers' comp. If you have even one employee, you need a workers' comp policy, and you need to carry New York State Disability Benefits (DBL) and Paid Family Leave (PFL) coverage as well. The penalties for non-compliance are severe: the state can issue stop-work orders and fine you up to $2,000 for every ten-day period without coverage.

Electrical work carries classification codes (typically NCCI code 5190 for wiring) that reflect the inherent danger of the trade. Your experience modification rate, or e-mod, directly affects your premium. A Rochester electrician with a clean three-year claims history might carry a 0.85 e-mod, saving 15% on premiums, while a contractor with multiple lost-time injuries could see rates 30-40% above the baseline.

Commercial Auto and Inland Marine for Tools and Equipment

Your vans and trucks are both transportation and mobile workshops. Commercial auto insurance is mandatory, and New York commercial auto rates are projected to rise by 6.02% in 2026, so budgeting for this increase matters.

Inland marine coverage protects your tools and equipment while they're in transit or on a job site. A standard commercial auto policy won't cover your $15,000 worth of meters, benders, and diagnostic equipment if your van gets broken into at a Rochester job site overnight. Inland marine fills that gap, typically covering tools whether they're in your vehicle, at a customer's location, or in temporary storage.

By: Michael Fusco

President of Joule Pro

INDEX

Joule Pro is a specialty insurance and risk program of Fusco Orsini & Associates Insurance Services, built exclusively for electrical contractors and licensed in all 50 states.

We work with electrical firms across the country — from California, Texas, Florida, New York, and coast to coast — placing General Liability, Workers' Compensation, Commercial Auto, Inland Marine, Surety Bonds, Excess Liability, and full specialty coverage stacks for commercial, industrial, service, residential, and low-voltage electrical contractors. Joule Pro is not a separate licensed entity. It is a dedicated program structure inside Fusco Orsini, giving electrical contractors access to specialty carriers, in-house claims advocacy, and trade-specific risk engineering under one program.

Navigating Rochester's Local Permitting and Licensing Mandates

City of Rochester Insurance Certificate Requirements

Pulling electrical permits in the City of Rochester requires more than just your license and a completed application. The city's Bureau of Inspection and Compliance Services requires proof of insurance, and they want to see specific documentation.

You'll need to provide a Certificate of Insurance (COI) naming the City of Rochester as a certificate holder. Most Rochester inspectors expect to see:

- General liability with minimum $1M/$2M limits

- Workers' compensation (or a CE-200 exemption if you're a sole proprietor with no employees)

- Proof of NYS disability benefits coverage

The COI needs to be current. Expired certificates are one of the most common reasons permit applications get kicked back, which delays your project timeline and frustrates your clients.

Electrical Code Compliance and Professional Liability

Rochester follows the New York State Uniform Fire Prevention and Building Code, which incorporates the National Electrical Code with state-specific amendments. Errors in code compliance can trigger professional liability claims, especially on commercial projects where an inspector flags deficient work that requires costly rework.

Professional liability (sometimes called errors and omissions) isn't required by the city, but it's increasingly requested by commercial GCs and property developers in Rochester. If your design or installation recommendation leads to a financial loss for a client, this policy responds where GL won't. For electricians doing design-build work or specifying equipment, this coverage is worth serious consideration.

Addressing Region-Specific Risks in Western New York

Winter Weather Hazards and Slip-and-Fall Liability

Rochester averages around 100 inches of snow per year, and that creates real liability exposure for electrical contractors. If you're working at a client's property and someone slips on ice near your work area or equipment, you could face a claim. Your GL policy covers this, but the frequency of winter slip-and-fall claims in Western New York means underwriters pay close attention to your safety protocols.

Practical steps that can reduce both claims and premiums include keeping salt and sand in your trucks during winter months, documenting site conditions with timestamped photos before starting work, and using caution tape or cones around exterior work areas. These aren't just good practice: they're the kind of risk management details that specialty insurers like Joule Pro look for when evaluating your account.

Cold weather also affects your vehicles. Rochester's freeze-thaw cycles destroy roads, and pothole damage to your fleet is a real cost. Comprehensive and collision coverage on your commercial auto policy should account for this, and maintaining higher deductibles on older vehicles can help manage premium costs.

Working with Rochester's Aging Industrial and Residential Infrastructure

A huge portion of Rochester's housing was built before 1950. Neighborhoods like the 19th Ward, Maplewood, and Swillburg are full of homes with knob-and-tube wiring, outdated panels, and aluminum wiring from the 1960s and 70s. Working on these systems carries higher risk than new construction.

The danger isn't just electrical. Older homes in Rochester may contain asbestos insulation around wiring, lead paint that gets disturbed during panel upgrades, and structural surprises behind walls and ceilings. Your insurance program needs to account for these exposures. A pollution liability endorsement, for instance, can protect you if asbestos disturbance triggers a cleanup claim.

Commercial electricians working in Rochester's former industrial buildings along the Genesee River corridor face similar challenges. These adaptive reuse projects often involve outdated three-phase systems, questionable grounding, and code compliance issues that require careful documentation.

Carrier Appetite and Underwriting for Monroe County Electricians

Preferred Carriers for Residential vs. Commercial Specialists

Not every insurance carrier wants to write electrical contractor policies, and carrier appetite varies significantly based on the type of work you do. Here's a general breakdown of how underwriters view Rochester electricians:

| Factor | Residential Specialists | Commercial/Industrial Specialists |

|---|---|---|

| Carrier appetite | Broad: many carriers compete | Narrower: fewer carriers, higher scrutiny |

| Typical GL premium range | $1,800 - $4,500/year | $4,000 - $15,000+/year |

| Key underwriting concerns | Completed operations, panel upgrades | Hot work, high-voltage systems, subcontractor use |

| Common exclusions to watch | EIFS, fire suppression work | Pollution, professional liability |

A specialty program like Joule Pro, which focuses exclusively on licensed electrical contractors, often has access to markets that generalist agencies can't reach. This matters in Rochester because the combination of older buildings and harsh weather makes some standard carriers hesitant to write policies here.

Impact of Claims History on Local Premium Rates

Your claims history is the single biggest factor in what you'll pay for insurance in Monroe County. One significant claim can increase your premiums by 20-35% at renewal, and the impact lingers for three to five years.

The most common claims among Rochester electricians include property damage from faulty installations, particularly in older homes where existing wiring complications cause issues. Slip-and-fall injuries on job sites rank second, followed by auto accidents involving work vehicles on Rochester's notoriously rough winter roads.

If you've had claims, don't try to hide them. Underwriters pull loss runs going back five years, and discrepancies between what you report and what shows up will get your application declined faster than anything else. Instead, document what you've done to prevent similar incidents. Carriers want to see that you've learned from past losses.

Optimizing Coverage and Reducing Insurance Costs

Smart Rochester electricians treat insurance as a business tool, not just an expense. A few strategies that consistently reduce costs without sacrificing protection:

Bundle your policies. Packaging GL, commercial auto, inland marine, and umbrella coverage under a single program typically saves 10-15% compared to buying each policy separately. Joule Pro structures its programs this way specifically for electrical contractors, which simplifies administration and often delivers better pricing.

Invest in safety training and document it. OSHA 10 or 30-hour certifications for your crew, regular toolbox talks, and written safety programs all signal to underwriters that you're a lower risk. Some carriers offer premium credits of 5-10% for documented safety programs.

Review your coverage annually. Your insurance needs change as your business grows. Adding a truck, hiring employees, or taking on commercial work all affect your exposure. An annual review with a producer who understands electrical contracting ensures you're neither over-insured nor dangerously underinsured.

FAQ

Do I need insurance to pull an electrical permit in Rochester? Yes. The City of Rochester requires proof of general liability and workers' compensation (or an exemption) before issuing electrical permits.

How much does general liability cost for a Rochester electrician? Residential specialists typically pay $1,800 to $4,500 annually. Commercial contractors pay more, often $4,000 to $15,000 or higher depending on revenue and scope of work.

Can I get workers' comp coverage if I'm a sole proprietor with no employees? Sole proprietors can file a CE-200 exemption with the state. But if you hire even one helper, you need a policy immediately.

Does my personal auto insurance cover my work van? No. Vehicles used for business purposes need commercial auto insurance. Personal policies exclude business use, and a claim denial at the wrong time could be devastating.

What's the best way to lower my insurance premiums? Maintain a clean claims history, invest in safety training, and work with a specialty program that understands electrical contractor risks rather than a generalist agency.

Your Next Steps

Getting electrician insurance right in Rochester means understanding the local requirements, accounting for Western New York's specific hazards, and working with carriers that actually want to insure electrical contractors. The permitting process, winter liability exposure, and aging building stock all create risks that generic insurance programs often miss or price poorly.

If you're shopping for coverage or feel like your current program has gaps, reach out to a specialty producer who focuses on the electrical trade. The right coverage protects your business, keeps you compliant with Rochester's permitting requirements, and gives you confidence to take on the projects that grow your company.

Founder & CEO

The Force Behind the Program

About the Author:

Michael Fusco.

Fusco Orsini & Associates

Joule Pro exists because Mike Fusco saw electrical contractors getting boilerplate insurance — and built a program designed for the way the trade actually works.

Mike is the CEO and co-founder of Fusco Orsini & Associates, the San Diego–based independent agency he launched in 2010. Under his leadership FOA has grown into a nationwide partner serving clients across 31 states, with a personal, client-first approach to commercial insurance and risk.

With over 20 years in insurance and risk management, he specializes in tailored programs spanning general liability, workers' compensation, surety bonding, and employee benefits — helping owners confidently manage risk and pursue growth.

Mike holds a B.S. in Business from the University of Maryland — Robert H. Smith School of Business, and the Certified Insurance Counselor (CIC) designation, held by fewer than 3% of insurance professionals nationwide.

What Our Clients Say

Trusted by Electrical Contractors Across the Country.

5.0

★★★★★

Google reviews

Core Commercial Coverage

Business Insurance for Electrical Contractors.

The fundamentals — written, structured, and priced for electrical risk. Each line is reviewed annually by an underwriter who only writes our trade.

01

General Liability

Premises & completed-operations coverage with electrical-specific endorsements and full pollution carve-back options.

02

Workers' Compensation

Class-code optimization, experience-mod review, and return-to-work programs designed for energized-work exposures.

03

Commercial Auto

Fleet, hired & non-owned auto, and tools-in-transit coverage written for service vans and bucket trucks.

04

Tools & Equipment

Scheduled and blanket coverage for tools, test equipment, scissor lifts, and contractor's equipment on-site or in-transit.

05

Surety Bonds

Bid, performance, and payment bonds — single-job and aggregate programs for commercial & public-works contracts.

06

Commercial Property

Layered limits up to $50M with carrier panels covering your shop, warehouse, yard, and on-premises tools, materials, and equipment.

Who We Serve

Electrical Contractors We Specialize In.

From $5M service shops to $250M industrial primes — every Joule Pro program is shaped to the contractor's revenue mix and project profile.

01 / Industrial

Commercial & Industrial Electrical Contractors

High-voltage, substation, and plant electrical work. Pollution, builder's risk, and large-deductible WC programs.

02 / Service

Service & Residential Electrical Contractors

Service-call shops, panel upgrades, and EV charging installers. Auto-fleet, GL, and tool-coverage programs.

03 / Low-Voltage

Specialty & Low-Voltage Contractors

Data, fire-alarm, security, and BMS controls. Cyber, professional liability, and follow-form excess.

Frequently Asked Questions

Common

Questions From

Electrical Contractors.

What size electrical contractors do you write?

Joule Pro is built for licensed electrical firms from roughly $2M in revenue to $250M+. Below $2M we typically refer to our small-business desk; above $250M we underwrite individually with our industrial practice team.

Do I need to be licensed in multiple states?

No. We license you wherever you work. Joule Pro is admitted in all 50 states and our compliance team handles multi-state filings, prevailing-wage endorsements, and certificate-of-insurance requirements.

How is Joule Pro different from a generic contractor program?

Generic programs use a contractor's questionnaire that treats you like a roofer. We use forms written for energized work, arc-flash exposures, and design-build risk — and our carriers price accordingly.

What does the claims process actually look like?

Every Joule Pro client is assigned a named claims advocate at bind. They take the FNOL, set strategy with your assigned attorney, and serve as your single point of contact through close.

Can you bond large public-works contracts?

Yes. Through our surety partners we write single-job bonds up to $75M and aggregate programs to $300M, with expedited turnarounds for school district, federal, and DOT work.

What happens at renewal?

Your producer and claims advocate jointly run a renewal review 90 days out — covering loss trends, exposure changes, and market alternatives — so renewal day is a confirmation, not a surprise.

From the Blog

Insights for Electrical Contractors.

Risk briefings, claim post-mortems, and program updates — written by our underwriters and risk engineers.

Get Started

Get a Quote on a Program Built Around Your Trade.

A 30-minute discovery call is the only commitment. You'll leave with a written gap analysis of your current program — yours to keep, whether you bind with us or not.